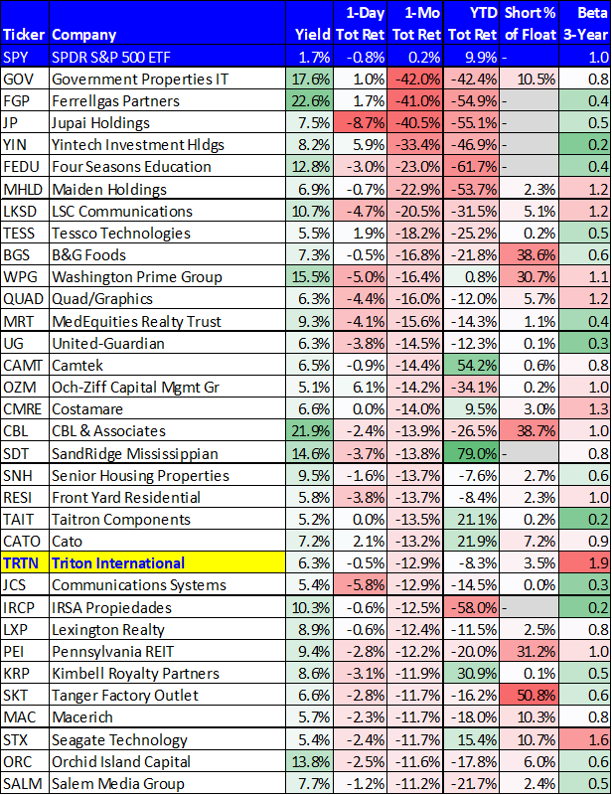

As the 10 year treasury yield hit a 7-year high on Thursday, the market got jittery. Specifically, many investors fear the fed’s increasingly hawkish monetary policies will put the brakes on the 9-year bull market rally. As a result, stocks sold-off. However, not all stocks are created equally, and some very attractive high-yielders extended their unwarranted slides. Here is a list of 100 high-yield stocks that have continued to sell-off, followed by five specific high-yielders that are attractive and worth considering.

Q3 hedge fund letters, conference, scoops etc

1. Triton International (TRTN), Yield: 6.3%

Triton is an intermodal shipping container company (i.e. the ubiquitous steel boxes on ships, trains and trucks), and it offers a tempting 6.3% dividend yield, especially after the recent sell-off, as shown in the above chart. However, before you go diving in head first, you should consider the big risks (i.e. the China “Trade War,” and economic sensitivity), as well as the many attractive qualities. You can view our full Triton write-up here:

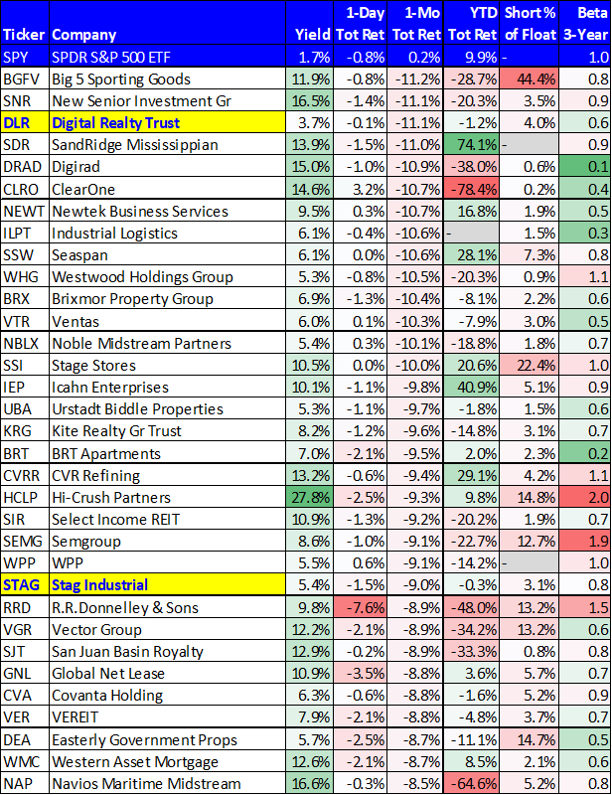

2. Digital Realty Trust (DLR), Yield: 3.7%

Data center REITs, such as Digital Realty in particular, have a lot of room to grow because of the explosive growth of data and particularly data being stored in “the cloud” (which basically means stored offsite on the servers of a data center, like Digital Realty properties). DLR owns the real estate upon which the data centers sit, and this is a lucrative position to be in.

We wrote about the attractiveness of DLR earlier this year, in this article:

Digital Realty: Despite Fear Mongers, Dividend, Price Will Rise

And the company has continued to perform well, and the share price was too, until the recent public offering which has caused the share price to sell-off. Of course the offering is a good thing because it gives the company capital to fund more growth (e.g. the recent Ascenty acquisition), but also because it gives investors another chance to buy at a lower price (i.e. this offering’s dilution has already occurred).

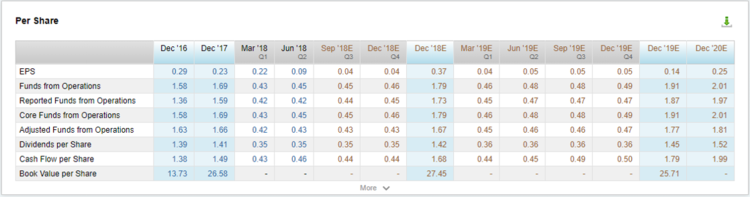

3. Stag International (STAG), Yield: 5.4%

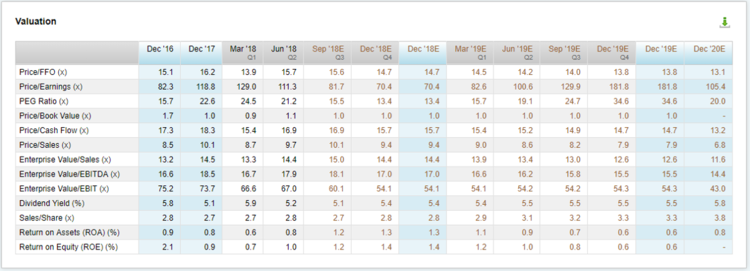

Stag is a big monthly dividend paying industrial REIT that continues to move away from its tertiary property history as it grows its secondary and primary property locations. However, the market still is not giving the company credit for this (the valuation metrics are too low), and the shares have recently pulled back (see chart above) making Stag even more attractive, in our view. Here is a look at some per share and valuation metrics for Stag, which are expected to keep moving in the right direction, per analyst forecasts (and as long as the economy remains relatively healthy, we agree).

We’ve written about Stag in the past, explaining we like the company, but advising to consider it on pullbacks as its higher beta (because it’s an industrial REIT, closely tied to economic strength) creates attractive buying opportunities. Here is one such report:

Since that report, the business has continued to improve, but the shares have pulled back. Also, the valuation is attractive, the monthly dividend is nice, and we believe Stag is worth considering if you are a long-term income-focused investor.

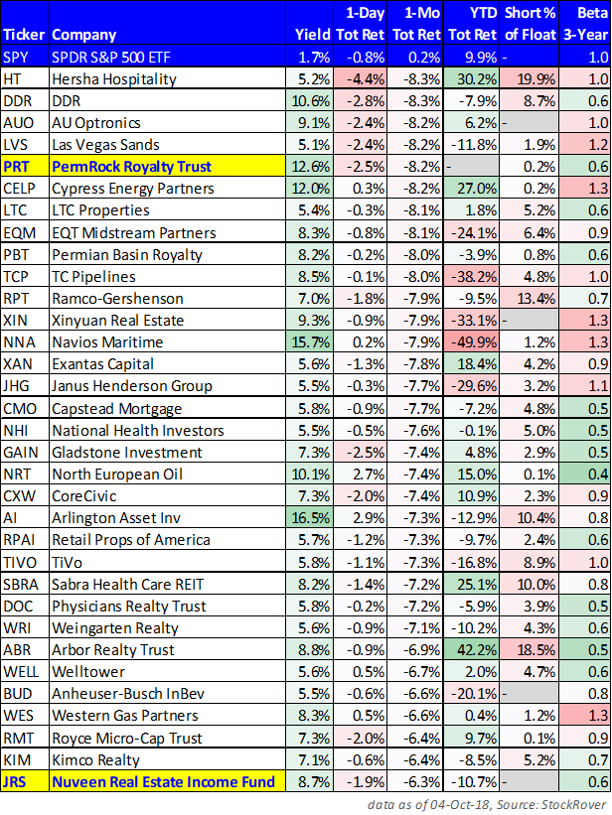

4. PermRock Royalty Trust (PRT), Yield: 12.6%

PermRock is an increasingly attractive high-yield, oil & gas, small cap that began trading earlier this year. The share price has recently pulled back sharply (as shown in the chart above) which makes it quite tempting, in our view—especially considering energy-related assets can be a hedge against inflation and a strong performer when other assets and industries struggle.

The main asset of PermRock is an 80% Net Profit Interest (“NPI”) in oil and natural gas producing properties in the Permian Basin of West Texas. Your can read our full write-up (including attractive characteristics and risks) on PRT here:

5. Nuveen Real Estate Income Fund (JRS), Yield: 8.7%

If you are an income-focused contrarian, JRS is worth considering. Not only have the shares of this closed-end fund sold-off as interest rate fears rise (real estate investment trusts rely heavily on borrowing to fund growth), but the widely discounted price to net asset value allows investors to buy this attractive basket of dividend paying securities at below market cost (the discount to NAV is currently an attractive -8.9%). You can read our previous write-up on JRS in this report:

Nuveen Real Estate Income Report

Conclusion:

A successful investor we work with likes to say “when the market pukes, we want to be there with a bucket.” Timing the absolute bottom in any market or security is likely a fool’s errand, but if you are an income-focused value investor, attractive opportunities do go “on sale,” and can trade at compelling prices. We’re not trying to time the bottom, but margin of safety can be important. If you like contrarian opportunities that pay high income, we believe the ideas included in this article are worth considering, particularly after their recent price pull-backs. In addition to the 5, perhaps you can find a few more based on the data in the table.

Article by Blue Harbinger