Performance DiscussionThere are two possible explanations of these results: we have become incompetent over the last five years or the equity markets are in a bubble somewhat similar to 1999, when cheap stocks declined and expensive shares rose parabolically. While we think that the latter is true, I am sure that patience is wearing thin and that the former explanation is gaining ground. Thankfully, the Fund has risen over 19% this month through July 16th, thereby erasing a portion of the downdraft. Looking at our past history, every time the Fund has experienced a similar drawdown, it has recovered quickly and created very strong short-term results. We are confident that another material rebound will occur in coming months and should end 2018 with a strong gain.

Basically, most of the stocks we currently own were trading near their 52-week lows as of June 30, 2018. It appears that there is a stealth bear market that is weaving its way through the averages, hitting a few sectors at a time. Importantly, the Fund’s holdings have rarely (or possibly never) been cheaper in aggregate. The average equity in the Fund is now trading at 9.5 times 2018 net income estimates and 8.4 times 2019 estimates while growing their revenues and earnings at respectable rates, a trend that should continue for many years.

Portfolio Outlook

Given the downdraft, expected returns from this point in time have risen. First, the revenue of our holdings should grow organically by roughly 4-5% each, some faster, some slower. With a bit of operating leverage, we would expect earnings to grow 6-7%. Due to material share repurchases at most of our holdings, we expect earnings per share to grow 10-12% annually, on a weighted average basis, and dividends to average around 3-4% per year. We also expect valuations to rise from 9 times next twelve months earnings to 12 times earnings due to rising returns on equity at many of our positions. This could be exceeded but we prefer to be a bit more conservative. If we include the fact that we expect Tesla to become troubled and potentially enter protection from creditors and a bit of leverage, we believe, using a large margin of safety, that the Fund should rise 32% per year the next 5 years, which would roughly turn $1 today into $4 in 5 years, pre-fees.

Market Outlook

Pundits continue to discuss how they believe that the market is overvalued and due for a fall. However, it is sort of like a basketball team with three guys like me along with Michael Jordan and LeBron James. While the average talent level would be quite high, success clearly depends upon who has the ball. The stock market may appear to be expensive by some metrics but since you are averaging in the massive market capitalizations of Amazon at ~200 times earnings, Netflix at ~150 times, etc, it skews the numbers in a material fashion. Thus, it is our assertion that the “average” valuation is as meaningless as the “average” talent level would be on our hypothetical basketball team. There are a number of incredibly inexpensive stocks and some wildly overvalued ones that average to a number that scares market analysts. We prefer to own the cheap ones knowing that, eventually, equity ownership at attractive prices works extremely well.

First Half Discussion

The biggest issue for the Fund has been the drop in financials due to falling long term interest rates, the decline in drug distribution companies, the downdraft in auto shares due to fears of the effects of a global trade war, and the rise in the shares we were short. These were partially offset by the rise in Valeant, which we sold 98% of after more than doubling our capital in a short period of time, and our realized profits in Express Scripts, Medtronic, Genworth, Coca Cola, General Mills, Target, Kroger, Mallinckrodt, Transocean, GM, and Shire Pharmaceuticals, among others. We recently repurchased a significant portion of our large bank positions, including JP Morgan, Goldman Sachs, Morgan Stanley, Bank of America and Citigroup, as they have fallen roughly 20% from the levels we sold them at earlier this year. Due to the large increases in dividends and massive share repurchases, which will be restarted in coming days, these positions should perform very well. As an example, Citigroup is yielding almost 3% and is repurchasing 10% of its shares for an effective yield of 13%. The banks are conservatively managed, are trading at low multiples of earnings and book value, are growing their deposits, loans, investment banking and trading activities, and are poised to recover meaningfully in coming months.

The drug distributors were hit late in the quarter due to the purchase of PillPack by Amazon. PillPack simply places drugs into packages, marked by the day, and ships them to chronic users’ homes. According to reports, CVS has been offering this service for years, with limited uptake, and it would not be difficult for the other incumbent companies to offer a similar service. The obvious worry is that Amazon will use this acquisition as a stepping stone to take over the drug distribution business by offering low prices and free shipping. Regarding prices, Walgreen’s has a net profit margin of roughly 4%. Though some would say they gouge customers to pay for excessive overhead, overall this profit margin is quite low. In addition, most people purchase as part of a co-pay arrangement that is fixed irrespective of the retailer. A $5 co-pay is the same at Walgreens, Costco or Wal-Mart, as an example. Second, most people tend to purchase pharmaceuticals in stores because they want or need immediate fulfillment. Waiting a few hours or day is often unacceptable. Thus, it will be hard to eliminate the stores. Nobody needs a TV or new shirt immediately; an antibiotic for an infection or blood pressure pills can’t wait, however. And finally, if you are one of the 6% of Americans who purchase drugs without insurance, WalMart already offers $4 generic prescriptions.

The drug distribution business is difficult to disrupt and change will come slowly, if at all. We believe that the incumbents will respond by offering home delivery options, if wanted, as Target and Kroger did. Those stocks rebounded 50% from the day Amazon purchased Whole Foods (we purchased both Target and Kroger and made 40-50% on those positions). A similar, or greater, recovery is in store for Walgreens and CVS.

Investors in the auto business seems to be fearing a spiraling of the trade war started by the current administration and another recession to top it all off. We did sell our position in GM after they announced the investment by Softbank into their self-driving technology, which caused the shares to rise 10% or so. The Fund made a profit of roughly 30% on the shares of GM in a relatively short period of time. Our current positions in Honda, Daimler and Ford, which have all fallen 20-30% recently, are still very attractive as they pay dividends ranging from 3.2%-6.4%, are growing unit volume 3-6%, are selling at roughly six times net income and 2-3 times EBITDA. For perspective, the average private equity transaction in larger companies appears to be occuring in the 10-12 times EBITDA range. We think that these shares will perform very well as they are largely selling at valuations below the levels they fell to in the financial crisis. Thus, a terrible recession is priced into these shares while continued economic plodding along will be huge upside.

And our short position in Tesla rose this year despite record losses, a terrible balance sheet, and making numbers by producing cars outdoors in a tent while skipping brake and alignment testing. Does this mean that the story of “productizing the factory”, “the machine that make the machine”, “alien dreadnaught”, and “air friction as a limiting factor” is similar to the Theranos revolutionary blood testing machine? We think so. To be clear, we aren’t anti-innovation; we are just against a hype machine that burns up precious savings with little chance of long term survival. The fact that the enterprise value (which takes into account net debt or net cash on a company’s balance sheet) of Tesla was recently above Daimler is beyond absurd. Daimler is today what Tesla wants to become: the leading maker of luxury automobiles and trucks worldwide. The main differences are that Daimler should earn $10 billion this year while Tesla is expected to lose at least $2 billion, Daimler produces more than twenty times more vehicles than Tesla, and Daimler has over $20 billion in cash, held for a rainy day, while Tesla has $12 billion in debt, negative $3 billion in working capital, and a Caa credit rating (defined as: An obligor is CURRENTLY VULNERABLE, and is dependent upon favorable business, financial, and economic conditions to meet its financial commitments). 1999 all over again.

Why are there so many cheap stocks?

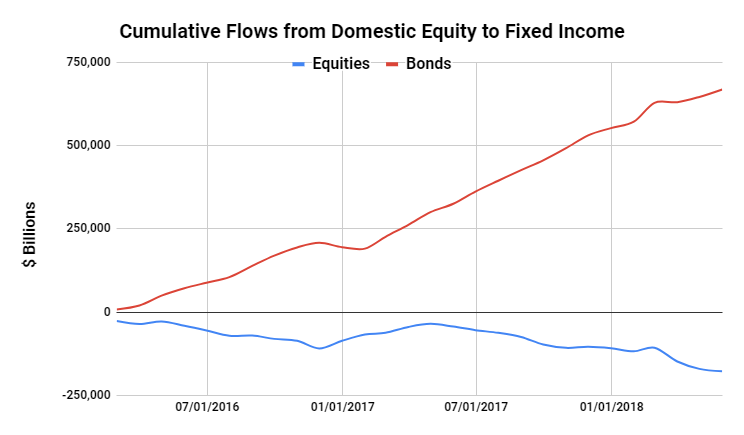

Because investors seem to dislike stocks, especially (or, better said, only) value names, more than any other asset. Money flows have been decidedly out of stocks and into bank deposits, cash, bonds, real estate and private equity at an extremely rapid and unrelenting pace.

</

Why? Because these assets do well, on a relative and mark to market basis, when stocks crash. And everyone seems to think, or know, that the next big crash is coming. Thus, the thinking seems to be “let’s get out of the market and preserve our principal so that we can reinvest at half of today’s prices”. But, if almost everyone thinks this and is acting upon it, does this not cause some stocks to become underpriced and drastically reduce the probability of an imminent crash? We think so. Almost nobody says to us “I think that there are areas within the stock market that are a great place to put fresh capital” and, therefore, there are.

Strategy Review

The Vilas Fund, LP uses a value-based strategy and focuses on those companies that are both growing their revenue and earnings, on an expected basis, at rates near or above GDP while trading at levels that are low when compared to shareholders equity and earnings. Also, we look to invest in companies that are currently, or are expected, to have returns on shareholders equity that are well over 10%. Companies that grow their revenues and earnings over long periods of time are more valuable than those companies that cannot grow or are in decline. Smaller companies that grow into large companies are the backbone of the American dream and provide jobs and economic growth. We look to invest in companies that fulfill these criteria, irrespective of their size or location.

Stocks since 1942

If you didn’t get a chance to attend live or watch on Yahoo Finance, the first ten minutes of the Berkshire Hathaway meeting was well worth the time. Mr. Buffett used this segment to show the headlines in the newspapers that existed in the four days prior to the purchase of his first stock. These headlines discussed the extensive battles in Japan and Europe, and the rising inflation, up to 6-7%, that the war spending was creating. Mr. Buffett explained how his purchase immediately declined 30% and how, when it eventually was up 10%, he sold it, only to watch it grow fivefold from the price he sold at (sounds really familiar). The point of this segment was to illustrate how a $10,000 investment in the Dow Jones Industrial Average on the date of his first stock purchase in 1942 would have performed until now. That $10,000 would have grown into $51 million currently. Gold, as a reference, would have grown from $10,000 to $400,000. Thus, stocks outperformed gold by 125-fold over this extended time period. No research was needed, no special strategies, no private, illiquid investments, no special knowledge. Just faith that equity ownership was better than the other options available and an ability to ignore current headlines and potentially bad economic news without reacting.

We, at Vilas, believe in long term equity ownership and believe that owning cheap stocks both lowers the risk of permanent loss of capital and raises expected returns. Over long periods of time, owning equities creates more wealth than any other securities. Trying to predict the next downturn or wiggle in the market is a strategy that is likely to lower those expected returns so we generally do not engage in those activities.

Professional Societies

So prior to the finance and economics masters degree from the University of Chicago, I earned a degree in Mechanical Engineering from the University of Wisconsin – Madison. In addition to a tremendous amount of math involved, which I greatly preferred over humanities (and my professors mutually agreed), Mechanical Engineering had a wide range of coursework, from Thermodynamics, Electrical Current and Motors, Fluid Dynamics, Civil and Structural Design, Material Science, and Internal Combustion Engines. In many of those courses, the concept of “over design” was discussed often. This concept was intended to make sure that if a bridge needed to carry 1,000,000 pounds under any stress scenario, it was designed to carry 3,000,000 pounds to account for unforeseen issues. Also, we studied some of the great failures of the past to help determine what went wrong and how to prevent it, as best as humanly possible, going forward. Remember the Tacoma Narrow Bridge failure? A wind at just the right speed and direction created harmonics that caused the bridge to swing wildly and collapse. This failure was studied greatly and future designs took into account the effects of wind and harmonics.

The NTSB studies nearly all failures in any mode of transportation, especially airplanes, to help learn and prevent future loss of life. Most practicing design engineers also become Professional Engineers, which is a comprehensive exam to make sure their education is thorough and that the student was diligent. This is also similar in medicine where prospective doctors take the Medical Board exams, which has a similar scientific based structure.

Benjamin Graham, a graduate of Columbia University, worked on Wall Street in the period leading up to the Great Depression. He was quite successful and earned roughly $500,000 per year in the 1920’s. The Great Crash nearly wiped out all of his investments, causing him to study the period and determine, with hindsight, what could have been done differently to help protect capital. He wrote Security Analysis in 1934 and lectured extensively at Columbia University. One of his students was Warren Buffett. In addition to other accomplishments, Benjamin Graham is considered, by many, to be the founding member of the CFA, a society with the goal of training students to hopefully avoid catastrophic investment results for clients. In essence, Ben Graham and the CFA focus on investments that have a tangible net worth that is substantial in relation to the price of the security, to help provide downside protection, and also have earnings and revenue growth to provide for capital appreciation. The CFA teaches financial statement analysis, to be able to determine the cash flows, and finance, to understand the time value of money and to determine the expected returns of an investment. In this sense, Ben Graham and the CFA created a structure that is quite similar to the engineering and medical disciplines: focus on learning from what went wrong in the past and strive, via education, to not repeat those mistakes.Ironically, over the last dozen years, it has paid large dividends to ignore the teachings of Ben Graham and focus on the most expensive companies that are growing their revenue the fastest, irrespective of balance sheet strength, valuation, current earnings or reasonable estimates of future earnings. In fact, large earning streams seem to be thought of as potential sources of disruption by “new economy” competition. The chart below describes how the average of the most expensive half (growth) and cheapest half (value) of companies performed the last 12 years. What is most interesting is that the tails of the distribution had differentials in performance that were much wider than the following graph. In essence, the most expensive stocks performed far better than the cheapest stocks, drastically exceeding the differential shown below. Sort of a “winner takes all” sort of a market. The issue is that many of these companies are trading at valuation levels 5, 10 or 20 times higher than the levels that Ben Graham would have taught was appropriate. Those who have followed his advice over the last dozen years appear foolish and shortsighted.

Fallacy of extended growth sharesAs an example, we have Amazon, one of the main drivers of the market and business strategy these days. Forgo profits today to grow revenue, put competitors out of business, and hopefully be able to raise prices in the future to offset the delay of returns on investor capital. Pretty much sums up a lot of the public, and private, darlings of today.

The issue with Amazon is now the law of large numbers. If shareholders buy the stock today, they are surely hoping for at least a 10% annual return on those shares over the next ten years. I would surmise that this would actually be a shockingly low expected return for the average shareholder today but if we use a faster rate in this analysis, it makes the following problem much worse. So we will use 10%.

If Amazon stock rises 10% annually, the company will have a $2.6 trillion market capitalization in 10 years. This is irrefutable and is just math. Next, we have to make two assumptions: the P/E ratio in 10 years and the profit margin in 10 years. Given that Apple, Microsoft and Google trade at roughly 20 times earnings on average today and are somewhat more mature than Amazon is currently, but similar to the 10-year older Amazon of 2028, we will use 20 times earnings as our base case. Further, the story of Amazon is that the investments of today will lead to larger profit margins in the future. We will assume that Amazon experiences a 200% increase in its net profit margin, from roughly 1.7% average the last few years to 5%. Could be higher, which we doubt, but also could be similar to today’s level. Using 5% is a decent estimate that gives Amazon a much higher return on their historical investments. The issue is that at a $2.6 trillion market cap trading at 20 times earnings, the company will need $130 billion per year in net income (which compares to the $11 billion it has earned, cumulatively, since inception 24 years ago). At a 5% profit margin, this means Amazon will need $2.6 trillion in revenue. US Gross Domestic Profit is roughly $20 trillion today, growing at 4% nominally. In ten years, it should be $30 trillion. Government is currently 18% of GDP, a ratio unlikely to go down. Thus, in ten years, the private sector should be $24.6 trillion. So, for Amazon shareholders to earn 10% per year, the company must become 11% of the private sector. For perspective, WalMart, the largest employer and revenue producer in the US, is roughly 3% of the private sector today.

The Fund has a very, very small short position in Amazon today (roughly 0.15% of equity). Needless to say, we don’t believe that the company can become 11% of the private sector and don’t believe that they can experience a tripling of their profit margin. Delivery expenses will continue to rise, with the shortage of delivery drivers, and the government will eventually become concerned with anti-trust type of issues. Trees don’t grow to the sky.

On the other hand, the Fund’s largest position is Walgreens. It is trading at roughly 10 times the next twelve months net income estimates. It has a solid balance sheet, lots of free cash flow, covers their interest expense easily, and will most likely continue to grow earnings per share at the same 12% rate that it has averaged over the last 20 years. More stores, new compounds, a growing population, an aging population, and share repurchases will drive earnings per share over the next decade or more. It normally traded at 16 times forward earnings estimates over the last decade but averaged roughly 20 times earnings going back further. In three years, Walgreens will likely be looking at earning $9.25 per share over the next twelve months. This corresponds to a $148 stock price at 16 times forward estimates. Further, the company will pay investors nearly $6 in dividends the next three years. Those buying the stock today should be able to see their investment rise to $154 in three years, a 134% return from today’s price, or a 32.8% annualized rate of return. Thus, there is lots of downside protection, due to their large free cash flow, strong balance sheet, and share repurchases, and a great deal of upside inherent in the stock of Walgreens.

Thus, the shareholders of Amazon will struggle to earn 10% per year, on an expected basis, and the shareholders of Walgreens could easily earn 30% annually for the next few years. It is just math. For perspective, the Fund has well over 100 times more dollars invested in Walgreen’s than in the Amazon short position; far more money is made investing in companies than betting against them.

Conclusion

Ben Graham taught students to use conservative assumptions and to have a large margin of safety to prevent permanent losses of capital. It seems that those who have followed his advice over the last decade are becoming entirely discredited while those engaging in wishful thinking are winning in nearly every respect. There is a reason we build bridges today that prevent harmonics. We use double blinded placebo trails in medicine. We change all the turbine blades more frequently on aircraft engines after one explodes and kills someone. In the investment world of today, however, using strategies with little to no margin of safety is what people seem to want, whether they know it or not.

Some stocks are too cheap, due to the above money flows, while some very large ones are far too expensive. This makes the market look somewhat expensive, overall. All stocks are not the same. Those who buy cheap stocks will perform much, much better than those buying very expensive shares, especially from this point forward.