Senior Investment Strategist Steve Lipper details three sectors at the intersection of quality and value where he is finding opportunities.

Q2 hedge fund letters, conference, scoops etc

Where are you finding attractive opportunities?

The approach that we find most useful to identify opportunities is looking for stocks at what we call the intersection of quality and value. And what we mean by that is companies that have above average profitability and below average valuation. And when you look across all the sectors today, there are three that really stick out.

Those are Materials, Industrials, and Consumer Discretionary. Let me take you to those one by one.

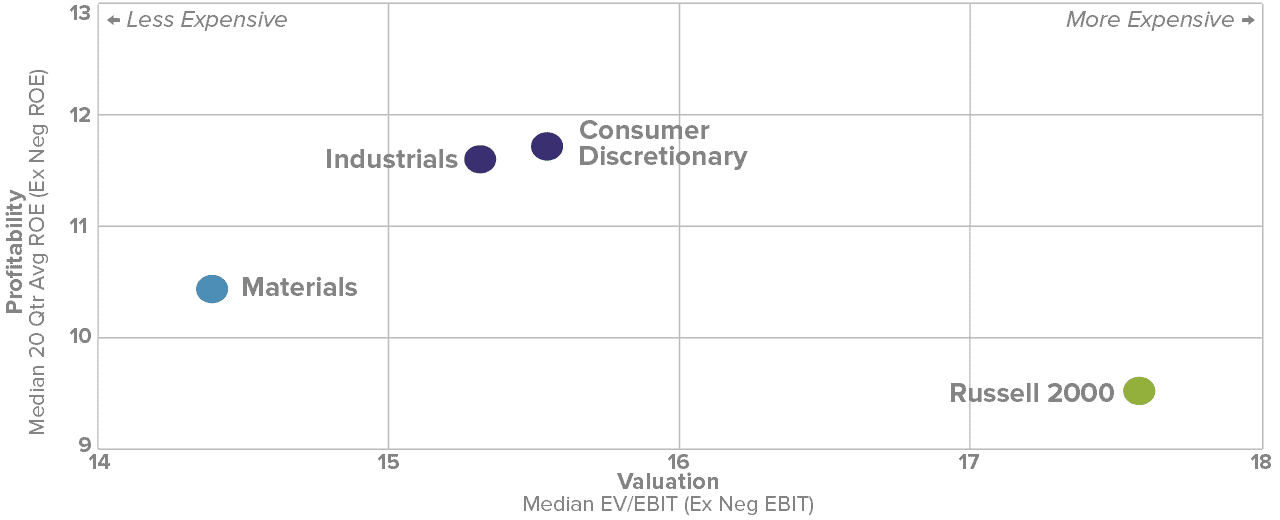

Selected Cyclical Sectors Appear Attractive

Russell 2000 as of 6/30/19

EV/EBIT is Earnings before interest and taxes. Return on Average Total Equity (ROE) is the trailing twelve month net income divided by the two fiscal period average total shareholders’ Equity. The performance data and trends outlined in this presentation are presented for illustrative purposes only. All performance information is presented on a total return basis and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Historical market trends are not necessarily indicative of future market movements. Sector and industry weightings are determined using the Global Industry Classification Standard (“GICS”). GICS was developed by, and is the exclusive property of, Standard & Poor’s Financial Services LLC (“S&P”) and MSCI Inc. (“MSCI”). GICS is the trademark of S&P and MSCI. “Global Industry Classification Standard (GICS)” and “GICS Direct” are service marks of S&P and MSCI.

Materials: Specialty Chemicals

First, let’s look at Materials. The area we find attractive right now is specialty chemicals. And that’s because we think there’s a misperception about exactly how cyclical their business models are. So in contrast with commodity chemical companies, specialty chemical companies often sell solutions that are much higher margin and are less sensitive to changes in unit volume. So there is less cyclicality than is appreciated, and that is causing a discount in the valuation that we think is unwarranted and we’re looking to take advantage of.

Industrials: Professional Services

The second area we find interesting is the so-called industrial area, though the area we’re excited about is not a smokestack industry. It’s the professional services firms of employment agencies, recruiters, or headhunters.

Well, let’s think about what part of the economy right now is really robust. It’s really the labor market. In fact, we’re going through a time right now, where there’s over a million more job openings in the U.S. than there are unemployed people. Up until last year, that had never occurred before.

This is a robust job market. Who benefits from that? Well, workers do, but also employment agencies, headhunters, and recruiters. And we have a number of investments in this area. Those that are specialized look to fill technology positions as well as those that are executive search firms looking to place senior executives. We think all of them have pretty good tailwind in this environment and their valuations we don’t think reflect that.

Consumer Discretionary: Recreational Vehicle

The third area we find opportunities is in Consumer Discretionary, though in more specific areas. But it reveals again what seems to be perhaps some misperceptions. So in an economy as vast and diverse as the U.S. there are always industry cycles that are going through their own pacing that may be distinct from the overall national economic cycle. So we think that you can often find industries that are in early part of their cycle despite the fact that the overall U.S. may be in a late part of its cycle. An example of that today is recreational vehicles.

Now, RVs have gone through a period of supply glut because there was great amount of inventory build which exceeded demand. During that period, the companies did not do so well and their stocks declined. We think that may be about to change and that better days may be ahead. We also think that some of the best opportunities are in the component suppliers to these RV manufacturers, and we think their valuations don’t reflect what we see as better days ahead.

Article by Royce Funds