PM Lauren Romeo discusses finding opportunities in the recent downturn and what she likes about four current holdings.

What is your take on the recent market downturn?

Downturns are never pleasant in the short run. However, at Royce we always try to put cash to work when share prices are falling to create potentially rewarding long-term opportunities.

Q3 hedge fund letters, conference, scoops etc

If you’re looking for more timely hedge fund insight, ValueWalk’s exclusive newsletter Hidden Value Stocks offers exclusive access to under-the-radar value hedge funds and their ideas. Click here to find out more and signup for a free no-obligation trial today.

The kind of high-quality characteristics that we seek in Premier—companies with high returns on invested capital and sustainable competitive advantages—are usually trading more closely to their full valuation. It can take a long time for what we think are high-quality small-caps to enter a favorable valuation range.

So far in the fourth quarter, we’ve added four new names to Premier’s portfolio, each as a result of the pullback that brought each company’s respective valuation to a level that we found attractive. These purchases came after relatively quiet second and third quarters, when most valuations appeared pretty stretched.

For the most part, we’ve had these companies on our “watch list” and/or owned them in more diversified portfolios we work on at Royce, so we’d already done our intensive fundamental research and analysis and gained high conviction in the business models. The market pullback created the final piece of the puzzle—a reasonable valuation entry point.

In what sectors have you been finding high-quality small-cap opportunities?

Many companies in the industrial and tech areas were pretty hard hit in the downturn, so in addition to the new names we added, we increased some existing positions in Premier as well. The four new names each came from a different sector—Industrials, Information Technology, Materials, and Consumer Discretionary.

Certain high-earning cyclical companies that we really like have been performing better as companies than they have as stocks in 2018. Investors’ concerns about peak profitability seem to be overshadowing the attractive valuations of these companies—even on a normalized earnings basis.

This short-term focus seems to be assigning little credit to what we think are the true drivers of these companies’ long-run market worth, that is, their ability to grow and compound value at above-average returns well into the future. We’re confident, however, that sustainable profit growth and prudent capital allocation are qualities that will draw increasing numbers of investors. We tend to find most of them in the Industrials and Information Technology sectors.

What have you been hearing recently from the management teams you talk to?

It depends a lot on the industry, of course, but for the most part managements’ views remain cautiously optimistic, which has been the case throughout the last year or so.

A lot of management teams are still concerned about tariffs and trade. Current demand overall continues to be generally strong, but we’ve heard from some companies that are pushing purchase orders out, hoping for clarity in the form of a more definitive resolution of trade questions with China.

Inflationary headwinds surrounding both labor and materials are also a concern, though we’ve seen more evidence that these increases can be passed on to customers without stifling demand. And many companies have been acting to deal effectively with these increases for some time.

I’d say, then, that the overall perspective is still positive and that much of the confidence stems from ongoing order strength or favorable secular demand trends across a number of industries.

Can you talk about two holdings in Premier that have done well in 2018? What factors have contributed to their success?

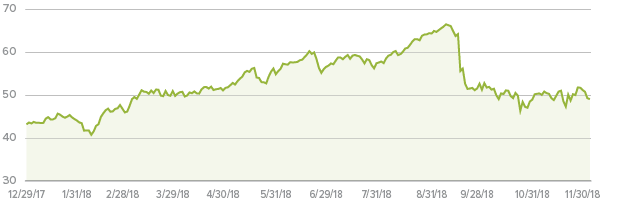

Two names that come to mind are Copart and Idexx Laboratories. Copart is the largest online salvage auction provider in the U.S. The company has seen increases in volume and revenue per car in 2018 in part due to its commitment to continuous improvements to its virtual bidding platform, which has been expanding the pool of potential buyers, auction participants, and bids per car.

Copart Stock Price

From 12/29/17 through 12/6/18

Copart also supplemented its growing European footprint through the acquisition of a salvage operation in Finland earlier this year, which increased its buyer base in Russia and the Baltic States. Finally, management recently detailed an accelerated infrastructure rollout in Germany, which has given it the necessary foothold to source inventory and validate the advantages of its consignment auction model to potential insurance company customers in that country.

What about Idexx Laboratories?

Idexx is a global leader in some very specific and interesting niches, all related. The firm provides diagnostics equipment, consumables, veterinary practice software, and outsourced lab testing services for companion animals, a market that’s projected to grow by mid-to-high single digits over the long term. Idexx continues to look past and outpace this benchmark with its own 10%-plus annual organic growth goals.

Idexx Laboratories Stock Price

From 12/29/17 through 12/6/18

The company currently boasts a 40% share in global diagnostics and software, which is twice the size of its next two largest competitors combined. Idexx also has 97%-plus retention rate on recurring consumables and lab revenue. This has allowed the company to generate significant cash flow, part of which it’s using to outspend the competition on R&D thereby solidifying its market dominance by introducing innovative new software, instruments, and tests.

So far in 2018, the company’s posted double-digit organic growth in both veterinary diagnostic instruments and the associated recurring revenue from test consumables, while also seeing increased adoption and utilization rates for the tests it’s brought to market.

Our conviction in the business model sustainability and unique niche for both Copart and Idexx is very high—but so is each firm’s valuation. So we’ve been selling into share price strength and reducing our position in both stocks as each company’s valuation has risen to levels that we thought more than fully reflected the expected returns and future value both looked likely to generate.

Can you discuss two of your high-confidence stocks in Premier that have not yet taken off?

One would be MKS Instruments, which was a top contributor for Premier in 2017. Spending on semiconductor capital equipment has decelerated in the second half of 2018, and the slowdown is projected to continue at least through the first half of 2019.

MKS Instruments Stock Price

From 12/29/17 through 12/6/18

We think this near-term uncertainty is overshadowing MKS’s evolution and its very attractive long-term prospects. First, in its legacy semiconductor equipment components and subsystems business, the company is retaining its significant market share and remaining a leader in technology. The capital intensity of semiconductor manufacturing is increasing while the major capital spenders—such as Samsung, Intel, and TSMC—increasingly rely on MKS not only as a supplier but also as an integral partner in developing and realizing their future technology roadmaps.

Second, MKS has worked diligently over the years to improve its operational efficiency and smooth out its cost structure so that its semiconductor business could continue to generate healthy profits even were it to face a sustained environment of lower demand.

Finally, we believe that investors don’t fully appreciate how successfully MKS has evolved from a semiconductor equipment company into a critical process technology provider. Its efforts on this score would include organic growth initiatives to cross-sell its core semiconductor offerings to non-semiconductor markets, the 2016 acquisition of Newport, which makes lasers and photonics, and the recently announced agreement to buy Electro Scientific Industries—a laser-based industrial machining and advanced printed circuit board equipment maker.

The result is that roughly 50% of MKS’s revenue is being generated outside the semiconductor industry and includes large, fast-growing end markets such as industrials, life & health sciences, telecommunications, and research and defense. We really like its prospects going forward.

Can you talk about one more company that hasn’t taken off yet in 2018?

Yes—another name would be Kennedy Wilson Holdings, a position that we reinitiated in Premier earlier this year. It’s a global real estate management firm that owns, operates, and invests primarily in multifamily and office properties in the Western U.S., the U.K., and Ireland.

Kennedy Wilson Holdings Stock Price

From 12/29/17 through 12/6/18

We see its primary advantage in the valuable knowledge the firm gains from local operating platforms in its target markets, along with the close ties that it’s established over the years, and through many real estate cycles, with major financial institutions in these same geographies.

These advantages help Kennedy Wilson to be early in identifying opportunities to develop underutilized assets or reposition existing ones to enhance cash flows. Local knowledge also drives astute portfolio management, particularly with respect to the timeliness of selectively harvesting assets to maximize value. And with close to $1 billion in liquidity—46% of which is in cash—the company possesses ample capital to deploy for future opportunities.

The firm also has a fee-based revenue stream from its growing real estate investment management platform through which it currently runs about $2 billion of commingled funds and separate accounts, primarily for institutional investors. The firm’s strong prospect pipeline underlies its annual $1 billion fundraising target and hints at strong growth potential for this recurring revenue source.

Finally, its adept capital allocation goes beyond real estate, with management opting to buy back $150 million of its stock this year at around $18 share, well below what we think it’s worth. With the stock still close to that price in early December, while also offering a 4.3% dividend yield, we believe it offers a compelling long-term risk/reward. We’re very happy to be holding shares in Premier.

Article by The Royce Funds