A few things.

Q2 2021 hedge fund letters, conferences and more

Asia Markets reported today that the CCP is cooking up a plan to restructure Evergrande into three separate entities, effectively ingurgitating them into the state, SEO style. As of now, this is only rumor, though a likely one.

China is a special case. Yes, they’re a mess. Its GDP has been artificially inflated with unproductive malinvestment for years. Its attitude towards debt growth has long been that a rolling loan gathers no loss and that dead pigs aren’t afraid of boiling water. Which, essentially translates to a collective YOLO attitude when it comes to financial gearing.

The ever erudite China commentator, Michael Pettis, lays out the tough choices ahead for Xi and party in his latest post (link here). It essentially boils down to three challenges (1) stopping contagion (2) containing financial distress and (3) solving the debt-fueled GDP growth issue.

According to Pettis, they can easily handle the first. The concern over spreading financial distress is real and a more difficult issue. Property values have fallen quite fast, seemingly catching the regulators by surprise. This one needs to be dealt with quickly and aggressively. And the third problem of debt being joined at the hip to GDP, “is almost impossible to resolve”.

China has relied on a Gerschenkron growth model for decades. I’ve written about this here, in We Will Bury You. Their growth has been dependent on suppressing Household’s share of GDP, which means private and state industries received more of that income (think large SEOs).

Since businesses consume less than households, this raised China’s savings rate. Savings equal investment, so China was able to maintain high levels of investment relative to GDP.

In an undeveloped country, which China was 20-years ago. This is a good thing. It boosts GDP, raises living standards, and modernizes the country’s capital stock (Pettis and Klein wrote an excellent book on this idea, called “Trade Wars are Class Wars”).

But, eventually, as was the case with China, you inevitably run out of large projects that you can productively finance. You cross the chasm of diminishing returns. So if you want to keep the party of high GDP growth. Which, Chinese elites very much did since this model is what gave them their elitist status in the first place. You simply crank up the leverage. Falling returns on investment, just require more leverage. And so it’s been for the last decade-plus.

Xi Jinping has been on a warpath to consolidate power so he can effectively confront these elites and rejigger the system — also because he wants to be President for life, but let’s focus on his positive traits for now.

If China wants to delink growth in debt from growth in the economy, it needs to raise the Household’s share of GDP. Give the consumers more of the income pie so they can go out and consume.

This means accepting a much lower growth rate, especially since Chinese consumers are already highly indebted. But it’s the country’s only viable path to creating a sustainable economy. One not driven by pilling on more IOUs. It’s also their only hope for exiting the middle-income trap (though I think that’s unlikely at this point).

Anywho, it’s going to be interesting to see how this plays out over the next few years. Cracking down on financial speculation is one of Xi’s big aims over the next three years. And it looks like he finally has the power to make headway there.

China’s real estate sector is where most of this speculation has been occurring. Estimates put China’s RE at roughly 27% of GDP. That’s quite a large footprint. To put that in perspective, the US’s real estate sector accounted for 7% of GDP at the height of the housing bubble.

China’s real estate sector is where most of this speculation has been occurring. Estimates put China’s RE at roughly 27% of GDP. That’s quite a large footprint. To put that in perspective, the US’s real estate sector accounted for 7% of GDP at the height of the housing bubble.

Here’s a terrific NBER paper that goes deeper into the size of the problem (link here). I pulled the chart to the right from it.

My base case — and take this with a shaker of salt because it’s China and well, I’m just a guy from Texas who eats at Panda Express only occasionally, so what do I know… my base case is that this will be a long-drawn-out affair, with spillover effects coming in the form of slower growth and lower demand for certain commodities. Not systemic risk or Lehman hysterics as I’ve seen many of the you-know-who’s shouting about on the twitters.

Xi is concerned first and foremost with control. To control you need a somewhat satiated public. That means no mass layoffs or AIG moments. Plus, the majority of the country’s debt is denominated in yuan. And they have over a $1trn in foreign currency deposits. So I’m pretty sure they’ll be able to manage for the time being.

Moving on…

The FOMC today was more hawkish than expected. Here’s the things to note from the statement and Powell’s presser:

- Median projection for 2022 shifted up by half a hike

- The 2023 plot jumped by one and a half hikes

- And the 2024 avg dot plot has the rate at 1.75%

- Taper is almost certainly coming in November and will probably wind up mid-2022

I don’t think this is enough to throw off the market by itself. But it’s a net negative as it brings up in time the market’s inevitable lasering in on rate hikes.

We’re still in wait-and-see mode… There’s certainly no shortage of developing narratives to tip this market over into a bit of a fit. The D.C. circus and debt ceiling talks I think have the most potential to stir things up.

Regardless, our base case is that we chop around for a bit. Maybe retest the lows again. But ultimately embark on another bull leg before we turn over into a larger extended correction later this winter.

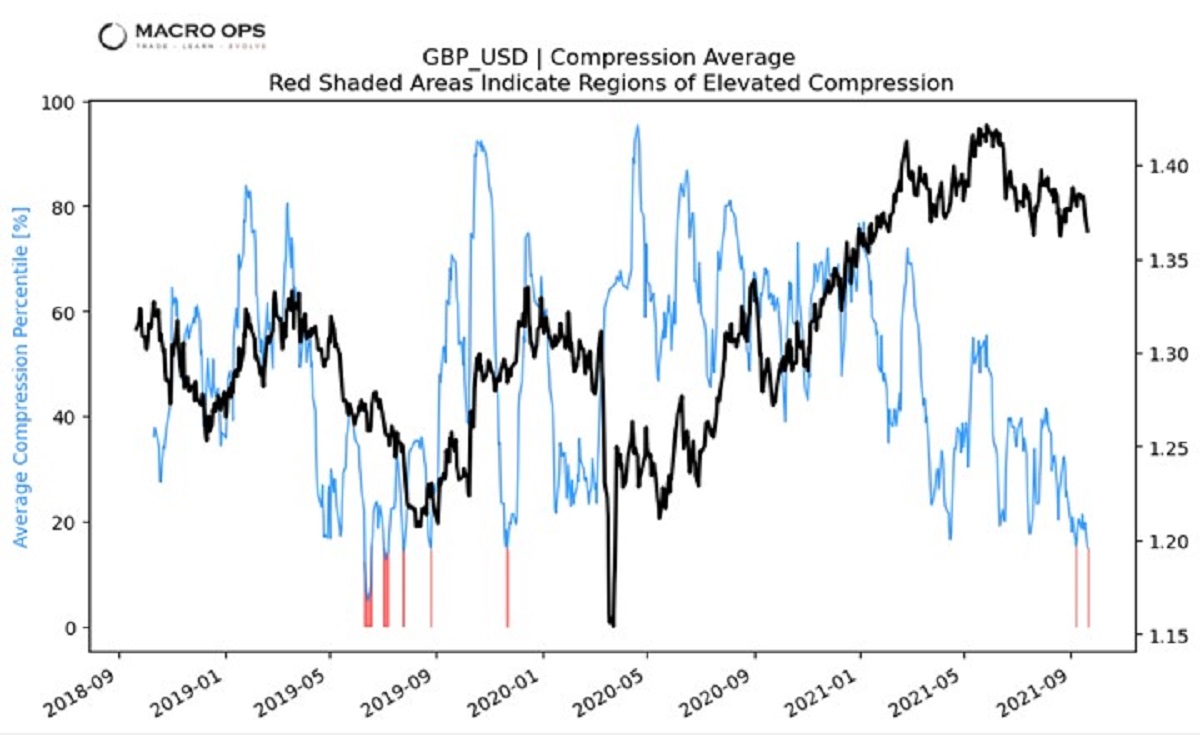

One trade we’re eyeing right now is GDPUSD. It’s at a multi-month inflection point.

It’s in a big compression regime indicating a big move is likely. Our yield curve oscillator says odds favor an eventual move higher. But, short-term I’m directionally agnostic and willing to play a break below or a bounce up. We’ll send out an alert if we pull the trigger.

***We’re opening enrollment into our Collective this week. The Collective is our full kit service that includes all of our research, a full library of reports and videos on theory and strategy, our proprietary market dashboard called the HUD, plus our internal slack where the team and I, plus fund managers and die-hards from around the world talk shop, exchange ideas and shoot the shit. If you’re interested in joining our crew, just click the link below. Looking forward to seeing you in the group.

Join The Collective

A percentage of all Collective sales go to the Special Operations Warrior Foundation, helping the children and family members of our fallen heroes.***

Thanks for reading.

Stay nimble and keep your head on a swivel.

Article by Alex Barrow, Macro Ops