Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Q3 2019 hedge fund letters, conferences and more

The growth of personal savings and investment in China of the last few years has a parallel in the boom in the “old Northwest” of the U.S. following the War of 1812. The parallel carries a fateful lesson for the future of China.

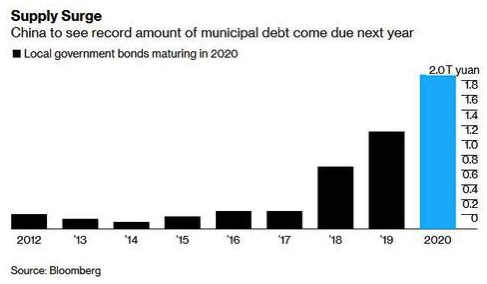

Both periods saw near exponential growth in property financing, development and speculation – all of which was paid for by local finance. As recently as three years ago, local government debt in China was maturing and being refinanced at the rate of 200 million yuan per year. This year municipal debt financings will be five times what they were in 2017. Next year it will double: two trillion yuan worth of bonds are expected to mature and will require either payment or refinancing.

There was an equally explosive real estate financing boom for Americans streaming across the Appalachians after the news of the Treaty of Ghent, which ended the War of 1812, reached the U.S. While the quantities for the two periods were very different – China’s numbers are in the trillions while for the U.S. they were in the tens of thousands – the rates of change are directly comparable. So are the social situations that produced the dramatic expansions of credit. In the “old Northwest”, land and property were bought and sold using the notes of local banks. In the same way special financing vehicles of local governments are the means by which Chinese have invested in apartments and other developed property.

The social pressures in favor of ever expanding lending are also comparable. In Ohio, Kentucky, Indiana and Tennessee, sales by existing property owners were seen as politically acceptable only if the proceeds were being used as the down payments for even larger speculations in local property. What was not acceptable was for someone to want to cash out. Just as the wealthy in Chinese provinces have their own money tied up in the merry-go-round of local development, the newly rich founders of the state banks in the old Northwest had their fortunes tied to local development financed by bank credit.

The numbers are quite extraordinary. In two years (1816-1818) the number of banks in the United States grew from 246 to 392. In Kentucky alone 40 new banks were chartered in the 1817-1818 legislative year. Public land sales rose from less than $4 million in 1816 to $13.6 million in 1818. In neither country did this property development occur in a vacuum. The national governments were busy with their own investments in infrastructure. In the U.S. federal construction expenditures rose 20-fold during the period – from less than $1 million in 1816 to more than $14 million in 1818.

We know what came next for the United States – the panic of 1819. What is not so well known is that this first Great Depression in American history was regional, not national. The panic and its consequences did not affect the external finances of the U.S. at all. The national bank – the second Bank of the United States – experienced no distress; its very success would later bring on the complaint that it had survived at the expense of the western state banks. The state and local banks in New York and New England had carried on without interruption; the panic occurred only with the banks that had financed the development of the lands opened up for development after the war. The northeastern banks had continued to redeem their notes for gold even as the Bank of England deferred its formal return to the gold standard.

Read the full article here by Stefan Jovanovich, Advisor Perspectives