Abstract

Factor investing has failed to live up to its many promises. Its success is compromised by three problems that are often underappreciated by investors. First, many investors develop exaggerated expectations about factor performance as a result of data mining, crowding, unrealistic trading cost expectations, and other concerns. Second, for investors using naive risk management tools, factor returns can experience downside shocks far larger than would be expected. Finally, investors are often led to believe their factor portfolio is diversified. Diversification can vanish, however, in certain economic conditions, when factor returns become much more correlated. Factor investing is a powerful tool, but understanding the risks involved is essential before adopting this investment framework.

Q4 hedge fund letters, conference, scoops etc

Factor investing involves allocating portfolio weights to certain known “factors.” Investors are typically led to develop their factor return expectations with little more than an extrapolation of the factor’s past paper-portfolio returns. But, past is not prologue. We argue that both the expected returns and the risks are rarely fully understood by investors, whether retail or institutional.

Factor investing is no longer a niche investment product. This investment style has been embraced by some of the world’s largest institutional investors, as well as by retail investors who now have access to hundreds of factor products. Given the widespread adoption of factor investing, it is worthwhile to take a step back and reexamine the process of factor development and investment.

Our article details three important misperceptions in factor investing: returns falling far short of expectations due to overfitting and/or crowding, drawdowns that far exceed expectations, and failed diversification, as correlations unexpectedly soar.

First, a factor can produce disappointing returns for multiple reasons. Recent research by Harvey, Liu, and Zhu (2016) documents 314 factors published in top academic journals (with many more “newly discovered factors” not making it into those top journals). How many of these added value in historical testing, on paper? Almost all of them, of course. How many were statistically significant? Almost all of them. How many investors asked these simple questions: Does this factor make sense or is it likely data mined? How crowded is the factor now? What are the likely trading costs to implement this factor? Is the historical performance of the candidate factor explained by its exposure to another factor (e.g., rising from low valuation to high valuation during the sample period)? Very few of the papers ask any of these questions, yet all of these issues lead to investors developing exaggerated expectations of factor performance.

Second, investors often have a naive view of the tail behavior of factor strategies.Most of these factor returns stray very far from a normal distribution. As such, it is a mistake to use simple risk management tools that ignore the tail behavior. Too many investors believe that creating a portfolio of factors will eliminate the extreme tail behavior. This is a dangerous misperception.

Third, investors need to understand correlations. Many investors mistakenly believe they can diversify away most of the risks in factor investing by creating a portfolio of several factors. In periods of market stress, however, most diversification benefits can vanish as the factors begin moving in unison. An understanding of how factors behave in different environments (e.g., high or low market volatility, high or low inflation, high or low real bond-market yields, economic expansion or recession), and of how correlations change through time, is essential.

In the second section, we detail the impact of data mining on both factor selection and disappointing out-of-sample factor performance. The third section demonstrates the extent of the non-normalities in factor returns. The fourth section explores how the degree of diversification is time varying. The fifth section of the paper quantifies the underperformance risks of factors exacerbated by non-normality and serial- and auto-correlation of factor return realizations. The sixth section of the paper examines the performance of factors over the last 15 years using a bootstrapping technique, which takes non-normalities into account, and tries to answer the question: Is factor investing broken? Some concluding remarks are offered in the final section.

Why Factor Premia Vanish

Of the thousands of factors tested, some will look good in the backtest purely by luck, i.e. as a consequence of data mining and backtest overfitting (point made by Harvey and Liu (2015) among others). Importantly, many of these lucky factors have little or no economic foundation which is emphasized in Harvey (2017). Some of these factors possibly look good as a result of coding mistakes by researchers or due to problems with the data. For example, McLean and Pontiff (2016) failed to replicate the in-sample performance of 12 out of 97 factors in their examination of the many published anomalies.1

Even if a factor has a true structural risk premium, real-world returns can disappoint once the factor becomes crowded.2 The backtest results do not reflect the market impact of investors pouring capital into the strategy. As the factor becomes crowded, too many investors seek to make approximately the same trades and the mispricing disappears. The anticipated arbitrage leads to disappointing returns. McLean and Pontiff (2016) and Arnott, Beck, and Kalesnik (2016) show that factor performance degrades after publication. We will quantify some of the return degradation later in this section.

When paper portfolios move to live trading, transactions costs start to play a very important role. Novy-Marx and Velikov (2016) show that almost no factor, constructed as a long–short portfolio, with turnover exceeding 50% has any return left after accounting for transactions costs.3 Hou, Xue, and Zhang (2017) review 447 factors and show that 64% of them fail to deliver statistically significant alpha when the backtest excludes the illiquid micro-cap names (defined as the bottom 2% of the market by market cap). This finding differs from overfitting, but has a similar consequence: if the strategy cannot be implemented in the manner the backtest assumes, the live experience will likely fall far short of the backtest results, even if an uninvestable paper portfolio concurrently matches the backtest results.

Factors are not independent, a finding that is well documented. Yet investors often mistakenly attribute the backtest result to a particular factor when the observed performance is due to exposure (its loading or factor beta) to another factor. Further, the backtest of the candidate factor might look impressive if it begins when it has low valuation levels and ends when it has high valuation levels, a point made by both Fama and French (2002) and Arnott and Bernstein (2002). This surely impacts the forward-looking premium, as Arnott et al. (2016) argue.

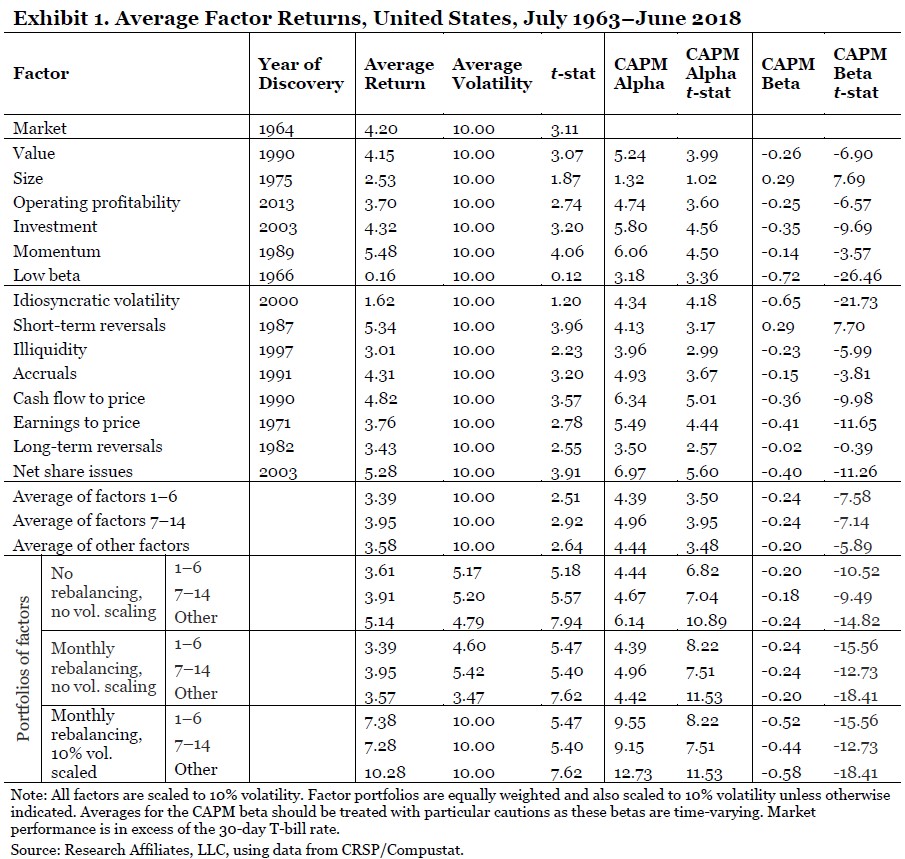

In Exhibit 1, we report the return characteristics of the 15 factors most closely followed by investors over the period July 1963 through June 2018. Beyond the market excess return factor, we divide the factors into two groups. The first group comprises the 6 factors used in the most popular academic multi-factor models (value, size, operating profitability, investment, momentum, and low beta) and the second group includes another 8 popular factors (idiosyncratic volatility, short-term reversals, illiquidity, accruals, cash flow to price, earnings to price, long-term reversals, and net share issues). We also provide summary information for an additional 33 factors frequently examined in the literature.

Read the full article here By Campbell Harvey, Rob Arnott, Vitali Kalesnik, Juhani Linnainmaa – Research Affiliates