Alpine Capital Research commentary for the month of July 2019, titled, “We’ve Seen this Movie Before.”

Q2 hedge fund letters, conference, scoops etc

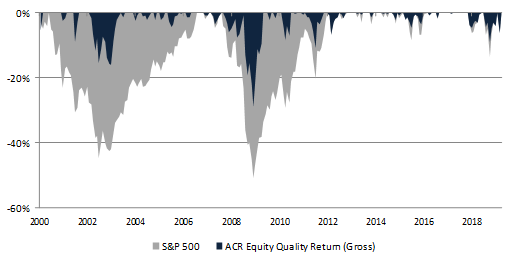

Trillions of dollars evaporated during the bear markets of 2000-2002 and 2007-2009. Disciplined execution of ACR’s first four principles were essential for helping us avoid losses resulting from these declines. Below is a chart of EQR’s record on that score.

EQR vs S&P 500 Drawdowns April 2000 – June 2019

The market declines themselves were exacerbated by investors who either bought or threw in the towel at the wrong time. Excellent communication – our fifth and only non-investment principle – helps investors avoid the wealth-destroying cycle of buying high and selling low. We believe that excellent communication is more important today than ever.

The two types of markets which foster destructive investor decision-making are: (a) the later stages of long, high-priced bull markets and, (b) fear-laden bear market bottoms. The current market is an historic example of the former and is statistically on par with the speculative markets of the late 1920’s and late 1990’s.

ACR expects to “underperform” bull markets like today’s. By underperform, we mean falling behind the market while seeking to protect our investors from high prices, not underperforming relative to our objectives. To the contrary, EQR has performed well and achieved our three objectives which are to: (i) protect capital, (ii) exceed a satisfactory absolute return, and (iii) beat the market over a full cycle. Annualized net-of-fees returns for EQR versus the S&P 500 were 10.4% vs. 5.6% since inception and 8.8% vs. 7.9% during the last full cycle1.

1 Total return including dividends and capital gains net of a 1% fee. EQR composite inception 4/3/00. Last full cycle beginning 11/1/07. EQR returns net of a 1% fee are supplemental information. See EQR’s full composite presentation at https://www.acr-invest.com/strategies/eqr-advised-sma-composite/94. Past performance is not indicative of future results.

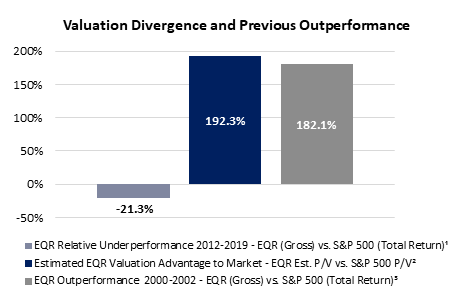

While expecting to fall behind today’s market, we are not worried about “catching up” again. The reason is that we believe our fundamental valuation advantage relative to the market in the long-term more than compensates for our market underperformance. The following chart illustrates this dynamic.

EQR has underperformed the market since 2012 by approximately 21%, but we believe this will be offset by our estimated 192% valuation advantage. The valuation advantage is defined by our estimated quarter-end price/value for EQR of 0.78 versus 2.28 for the S&P 500. While it may seem implausible that there could be such a large valuation differential between EQR and the market, our last four of five commentaries provide the reasoning and data which support our price/value statistics. Perhaps more importantly, we’ve seen this movie before.

During the bear market from April-2000 to December-2002, EQR’s total cumulative return was +71% versus the S&P 500 return of -39%. That is 182% of gross relative outperformance and within chipping distance of our estimated 192% valuation advantage today. However, we want to make clear that ACR believes EQR is unlikely to outperform the market by so much in such a short time again. The timing and undulations of future performance are impossible to predict.

1 The required market decline for the S&P 500 TR to reach performance parity with EQR (Gross of Fees) for 2012-2019 Q2.

² The difference between EQR’s estimated price/value (P/V) of 0.78 and the S&P 500’s estimated P/V of 2.28. These numbers represent the valuation estimates of ACR’s investment team.

³ EQR (‘Pure Gross ’) outperformed S&P 500 TR by 182% from inception in Apr 2000 to Dec 2002. EQR +71% vs. S&P 500 -39%. Figures are total return (“TR”) including dividends and capital gains. EQR ‘Pure Gross’ returns are gross of all fees including brokerage commissions and are supplemental information. See EQR’s full composite presentation at https://www.acr-invest.com/strategies/eqr-advised-sma-composite/94. Past performance is not indicative of future results.

Regardless of how future performance unfolds, it is interesting to note the similarities in valuation statistics today and in 2000. P/E ratios at quarter end were 10.4x for EQR and 32.7x for the S&P 500. During our first year in business, the ratios were ~10x for EQR and ~30x for the S&P 500. Such large valuation discrepancies prompted ACR’s founding.

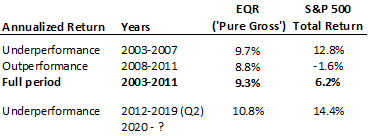

We have also seen the relative underperformance and subsequent outperformance movie before. The following table illustrates our other major period of market underperformance, and what happened next.

All figures are total return including dividends and capital gains. EQR ‘Pure Gross’ returns are gross of all fees including brokerage commissions and are supplemental information. See EQR’s full composite presentation at https://www.acr-invest.com/strategies/eqr-advised-sma-composite/94. Past performance is not indicative of future results.

EQR’s underperformance from 2003-2007 was disproportionately offset by our outperformance from 2008-2011. Just as importantly for investors with regular spending requirements, EQR provided a far smoother ride with satisfactory absolute returns and spendable gains along the way.

There are two differences between this past period and today. The underperformance today is marginally greater at -21% versus -13% during the 2003-2007 period. However, the greater underperformance is dwarfed by the second difference. EQR’s estimated valuation advantage today of 192% is far greater than our estimated valuation advantage of 107% in 2007. Similarly, the EQR earnings yield is 210% higher than the market today (9.6% v 3.1%) versus 63% higher than the market in 2007 (6.5% v 4.0%).

At the risk of sounding promotional, these statistics support our belief that today is a great time to invest in EQR and a risky time to invest in the broader market. More importantly, we want to ensure that our clients do not make a wealth-destroying mistake. Our investment performance through the market extremes of the ‘00s led to significant new capital investment in our EQR strategy since 2012. These newer clients have not yet experienced the true benefits of our strategy. We want to reassure them that we have indeed seen this movie before, and the story ended well.

Nick Tompras

July 2019

Article by Alpine Capital Research