Key Points

- Most investors seek to earn a 5% annualized return above inflation to securely meet their financial needs in retirement. With today’s low expected returns across financial markets, most mainstream portfolios, including the typical advisor portfolio, are poised to fall well short of this mark.

- An alternative risk premia strategy—one that harvests robust factor premia via long–short exposures to mature and varied asset classes, preferably in a straightforward, systematic, and transparent framework—provides attractive absolute return prospects and materially improved odds of achieving long-term return targets.

- A systematic alternative risk premia strategy can deliver valuable benefits beyond attractive returns, such as improved portfolio diversification and reduced downside risk.

Q3 hedge fund letters, conference, scoops etc

For most investors, earning less than a 5% annualized total return above inflation means they will likely fall short of meeting their financial needs in retirement. A couple of years ago, our colleagues West and Masturzo (2016) invited investors to try the “5% challenge,” posing the question: What are the odds your portfolio will earn an annualized real return of 5% over the next decade? Since launching the challenge two years ago, of the more than 53,000 portfolios created, only 14% have topped this mark. Unfortunately, from today’s starting point of low interest rates and elevated equity valuations, most mainstream portfolios are doomed to fall short. The 5% challenge proves difficult even for the relatively diversified portfolios recommended by the average financial advisor.

We see a wide gap between 1) the long-term return most investors base their planning decisions on, and 2) the annualized return their conventional portfolio is poised to realize over the coming decade. In this article, we explore one path with the potential to close a portion of this gap without materially increasing portfolio-level risk. We propose adding a liquid and transparent systematic alternative risk premia strategy as a core alternative allocation to complement investors’ mainstream-centric portfolios. This strategy appears to offer a compelling option which should raise an investor’s odds of clearing the 5% real return hurdle.

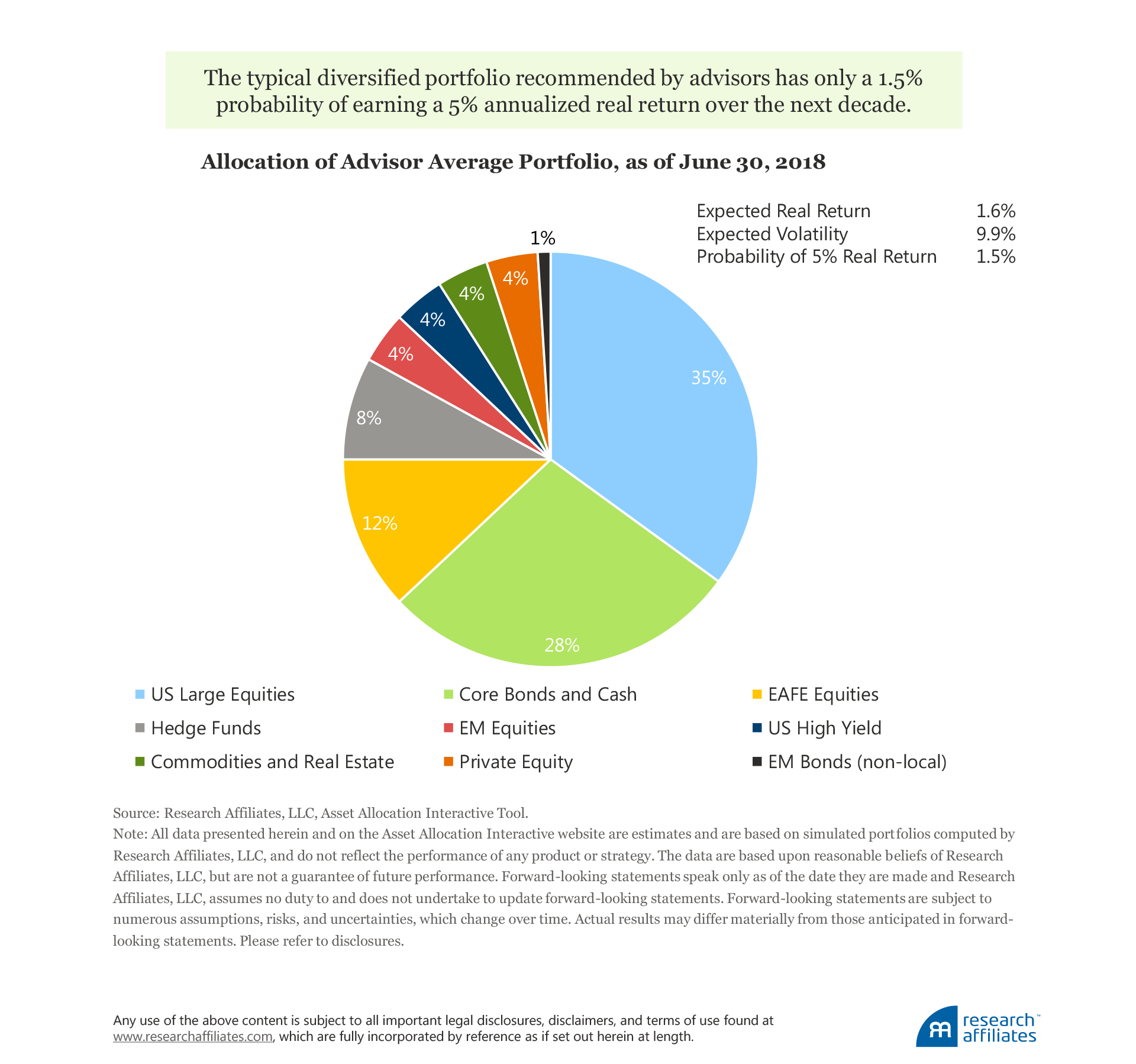

Falling Short: Expected Returns of Traditional Portfolios

Today, we expect a traditional US 60/40 portfolio allocation1 to earn an annualized real return of 0.6% over the next decade. This translates into less than a 1% probability of achieving a 5% annualized real return. As Brightman (2012) explains, starting yields make up the largest and most predictable component of expected returns for most assets and strategies. A more-diversified portfolio, such as one recommended by the average financial advisor,2 also appears to fall far short of most investors’ desired long-term return target. Despite allocating nearly one-quarter to nonmainstream assets such as credit, commodities, real estate, hedge funds, and private equity, the typical portfolio recommended by financial advisors, which we call the Average Advisor portfolio, is priced today to eke out a real return of only 1.6% a year over the next decade. The probability of its earning an annualized real return of 5% over that period is a mere 1.5%. A 5% annualized real long-term return is an increasingly difficult hurdle to clear!

Improving the Odds

Backed by our investment research and supported by our investing philosophy, we believe including a systematic alternative risk premia strategy can improve the odds of a portfolio’s meeting its long-term return hurdle. Such a strategy harvests robust factor premia, such as carry, value, and momentum, via long–short exposures to liquid futures contracts in a straightforward, systematic, and transparent portfolio design. For instance, we estimate a 20% allocation to such an approach3 more than triples the Average Advisor portfolio’s probability of clearing the 5% return target, improving the odds from 1.5% to over 5%, and an aggressive allocation of 40% moves this probability to over 21%. Importantly, the alternative risk premia strategy includes exposures absent from most advisor portfolios, so the increased return comes along with improved portfolio diversification, lower portfolio-level volatility, lower higher-order moments, and reduced downside risk.

Robust Risk Premia

According to the 2018 JPMorgan Institutional Investor survey,4 approximately 36% of the 214 respondents (pensions, insurance companies, endowments, funds of funds, consultants, and banks) plan to invest in alternative risk premia strategies in 2018. Increasingly, these strategies are available to retail investors. These strategies can take a variety of approaches, but generally seek to capture a collection of risk factors, or risk premia, largely uncorrelated with major markets and to each other, and are implemented across multiple asset classes and styles. By gaining exposure through cheap and liquid implementation in a systematic and robust manner, these strategies tend to harness risk premia at a lower cost and with greater transparency than traditional alternative structures, such as hedge funds.

A risk premium is likely to persist when based on a robust factor. Beck et al. (2016) find that a factor’s robustness is characterized by being 1) grounded in a long and deep academic literature; 2) robust across minor perturbations in the factor’s various definitions; 3) robust across geographies; and 4) implementable, with trading costs that do not threaten to erode returns. In the alternatives space, Brightman and Shepherd (2016) describe carry, value, and momentum as the most well-known, theoretically sound, and empirically robust factors. Our research findings consistently remind us why emphasizing robustness, liquidity, and implementation quality, while removing unnecessary complexity, is vital to helping investors reap and keep the rewards offered by these alternative sources of risk premia.

Let’s look more closely at the three factors of carry, value, and momentum.

- Carry refers to a long position in a relatively higher-yielding asset financed by a short position in a lower-yielding asset. As Brightman and Shepherd (2016) discuss, often this yield premium—especially absent an underlying directional market exposure—serves as compensation for the risk of shifting spot prices. The well-documented currency carry trade serves as a good example. The trade persists because investors who hold high-interest-rate currencies seek a yield premium to offset the crash risk that comes with negative spot price movements concentrated in economic downturns (Lustig and Verdelhan, 2007). And as Keynes’ (1930) theory of normal backwardation describes, the commodity carry trade delivers a yield premium in order to encourage speculative capital to provide price volatility insurance to producers with large upfront costs (say, when corn seed is planted) and with uncertain future revenues (when the crop is harvested and brought to market). Augmenting carry strategies with other robust factors designed to determine changes in spot prices, such as value and momentum, leads to greatly mitigated volatility, lowered skewness, and insulation against large drawdowns.

- Value is another well-established, robust factor with a long history of academic exploration. One of the first factors identified, value’s origins can be traced to the work of Graham and Dodd in the 1930s. Value refers to the tendency of relatively cheap investments to outperform relatively expensive ones over a longer holding period, so that value investors tend to be compensated for patiently holding uncomfortable, contrarian positions. Value often requires taking on maverick risk (Arnott, 2003), which makes it particularly well suited for a systematic investment strategy inherently immune to the behavioral tendency of investors to buy high and sell low.

- Momentum can be viewed as the mirror image of value. While momentum and value both aim to predict spot price movements, they do so over different time horizons, and therefore serve as excellent complements to one another. Also known as trend following,5 momentum involves buying assets whose prices have been recently rising and selling those whose prices have been recently falling. Short-term momentum suggests that prices initially underreact to a news event, allowing for the continuation in the directional price movement and creating a self-reinforcing trend. In some markets, momentum can be perpetuated by institutional frictions or actions, such as central banks intervening in the currency markets to stabilize exchange rates and mitigate volatility.

In the spirit of “no free lunches” we encourage investors to come to a deep understanding of the sources of risk that drive their expected returns prior to committing their investment dollars; some type of risk is almost always present in an investment whether obvious or not! Having an awareness of the investment risks associated with alternative risk premia strategies, which commonly involve the use of leverage, derivatives, and both long and short exposures, and which require a high degree of skill in implementation, is of particular importance.

Construction Considerations

Once satisfied that carry, value, and momentum strategies are robust and should continue to deliver a desirable return stream to complement traditional portfolios, the next step is knowing how to best access these premia and combine them in a portfolio. We favor using the combination of carry, value, and momentum because these factors have complementary exposures with clear empirical and theoretical support and which address the different building blocks that make up the total return of any investment (Brightman and Shepherd, 2016). As previously stated, carry is the yield differential earned on a long higher-yielding position and paid on a short lower-yielding position; value can exploit potential price adjustments over longer horizons; and momentum targets short-run impacts on spot prices.

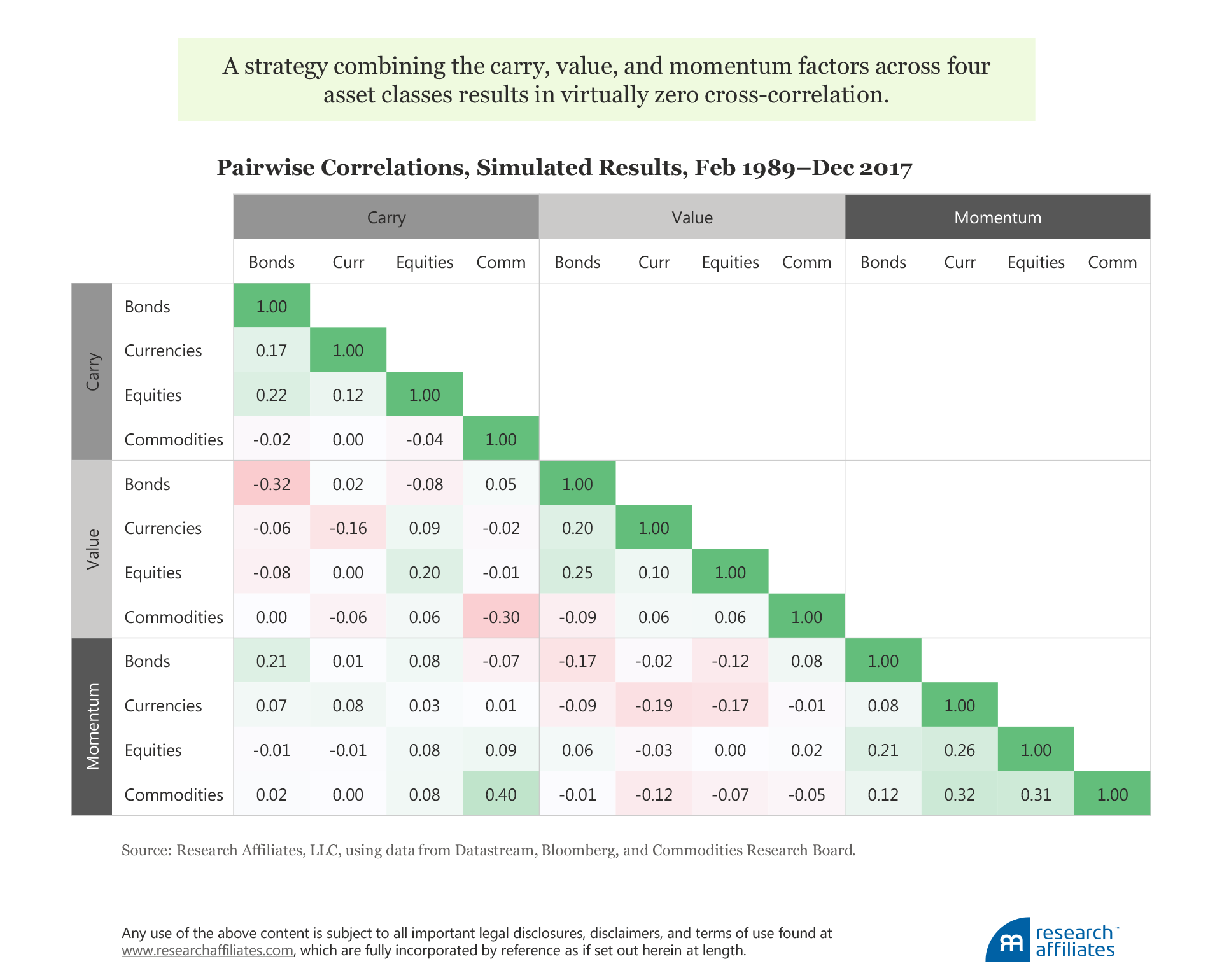

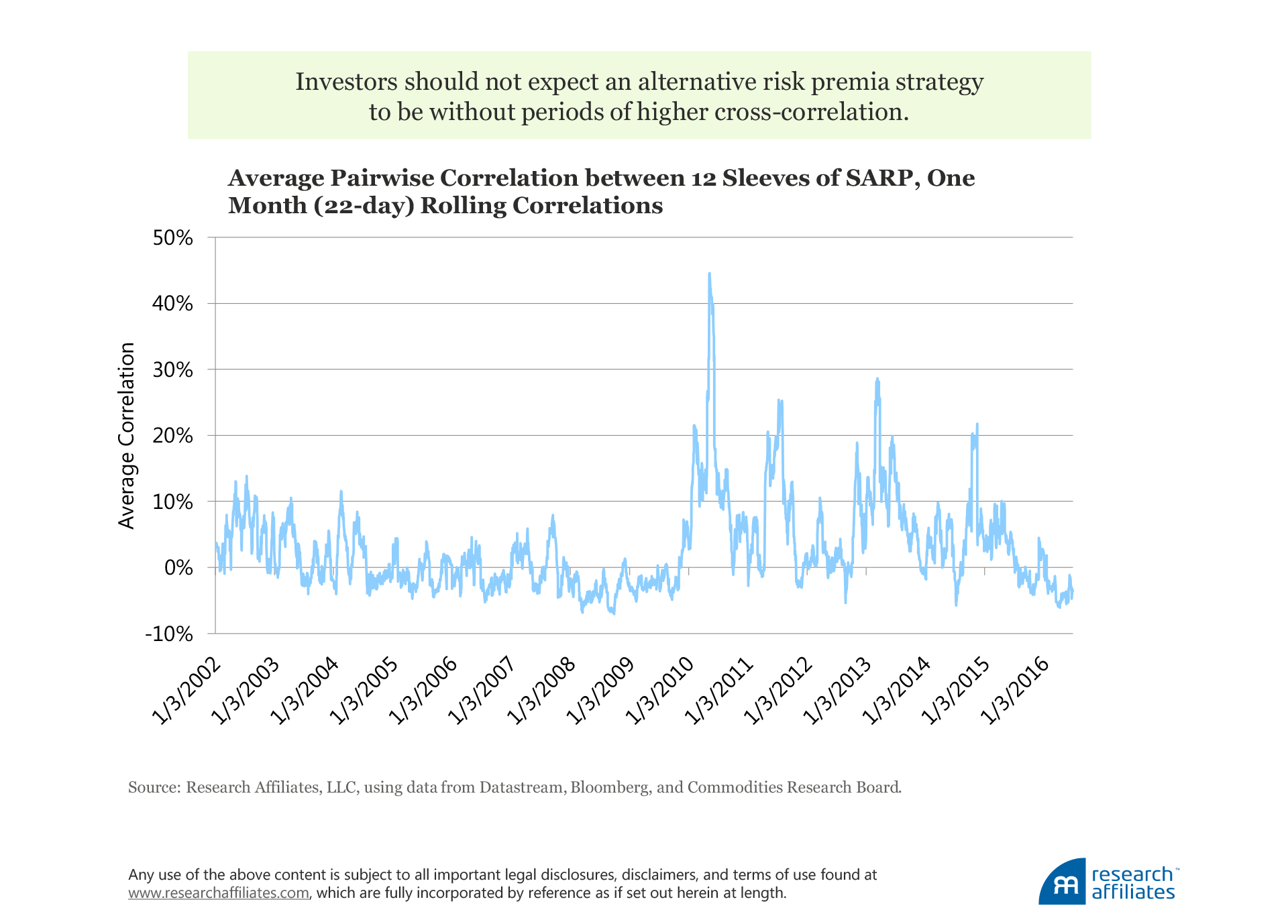

Generally, the initial benefit of combining factors in an alternative risk premia strategy shows up as volatility reduction.6 Thus, the correlations of the component factors must maintain their diversifying properties in order for the strategy to deliver on its promise. We analyze the correlation levels of all combinations across three factors—carry, value, and momentum—across four markets—bonds, currencies, equities, and commodities—from February 1989 through December 2017. The average pairwise correlation of these 12 sleeves is 0.03, which means they are essentially uncorrelated. Furthermore, the time variation of these average pairwise correlations has typically been quite low, even over short horizons, with rolling one month (22-day) correlations wavering between −10% and +10%, although we have observed several meaningful rises in these correlations over the last 10 years. These short-lived periods of spikes in correlation are a warning sign of the danger of the risk and leverage in these strategies and a reminder that they need to be assumed with a degree of humility, not with blind adherence to the historical data and the output of overly calibrated models.

When combining individual factors, product design and implementation considerations can significantly impact a strategy’s ability to harvest these premia, as Li and Shepherd (2018) discuss. We support a systematic approach incorporating a long–short construction and relatively straightforward design, which has the following benefits:

- Systematic vs. Discretionary Approach. A systematic approach, far more immune to psychological and organizational biases than a discretionary approach, ensures the strategy remains invested. Many alternative risk premia exist precisely because of psychological tendencies that overwhelm discretionary traders in the heat of the moment. Abandoning a systematic process increases the odds of falling right into these behavioral traps.

- Long–Short vs. Long-Only Approach. One of the key features of an alternative risk premia strategy is limited directional exposure to traditional asset classes, increasing their value as a useful source of diversification for the total portfolio. By going long investments with attractive factor scores and shorting those that rate poorly, investors can harvest premia across various markets absent significant risk associated with the direction of the underlying markets. These premia often provide attractive Sharpe ratios, but with low unlevered returns. The careful application of leverage in a long–short portfolio design can amplify returns enough, however, to make them impactful for the entire portfolio. Of course, the use of leverage and derivatives magnifies volatility (intentionally so), but often unintentionally magnifies many other investment risks, such as model error risk, parameter misestimation, and collateral risk, which brings us to the natural trade-off between complexity and simplicity in design.

- Simplicity vs. Complexity. Guided by our investment beliefs, we caution against unnecessary complexity and overstated claims of infallible investment processes, which often are merely examples of overfitting and overconfidence. We see less danger in erring toward reducing complexity and increasing transparency: “Complexity can dampen investor understanding, which can lead to poor investment decision making so that an investor’s long-term financial goals are not achieved…. If a simple design works, ample evidence suggests that the investor benefits by choosing simplicity” (Hsu and West, 2016). Avoiding unnecessary complexity helps avoid unintentional data mining of factor definitions or contract-weighting schemes, results in lower turnover and more cost-effective implementation, and increases the likelihood that out-of-sample results will reflect simulated backtests.

Expected Outcomes

Given the low expected return prospects across most asset classes, the majority of investor portfolios are poised to deliver returns far below their desired long-term real return targets. We review the outcomes investors stand to realize by complementing their mainstream portfolios with an alternative risk premia strategy.

The right level of allocation to an alternative risk premia strategy depends on an investor’s tolerance for tracking error and their comfort level with nonmainstream investment strategies. For simplicity, we show a spectrum of results for portfolios that shift away from the Advisor Average portfolio and into an alternative risk premia strategy at allocations ranging from 10% to 40% of the portfolio. To estimate the forward-looking return expectations for the asset classes in the Advisor Average portfolio, we follow the methodology described on our Asset Allocation Interactive web tool. To represent the systematic alternative risk premia option, we use the long-term return target for our Systematic Alternative Risk Premia (SARP) strategy between a 7% and 9% excess return,7 apply an average volatility expectation of 11%, and assume that historical cross-correlations with other asset classes are indicative of future averages.

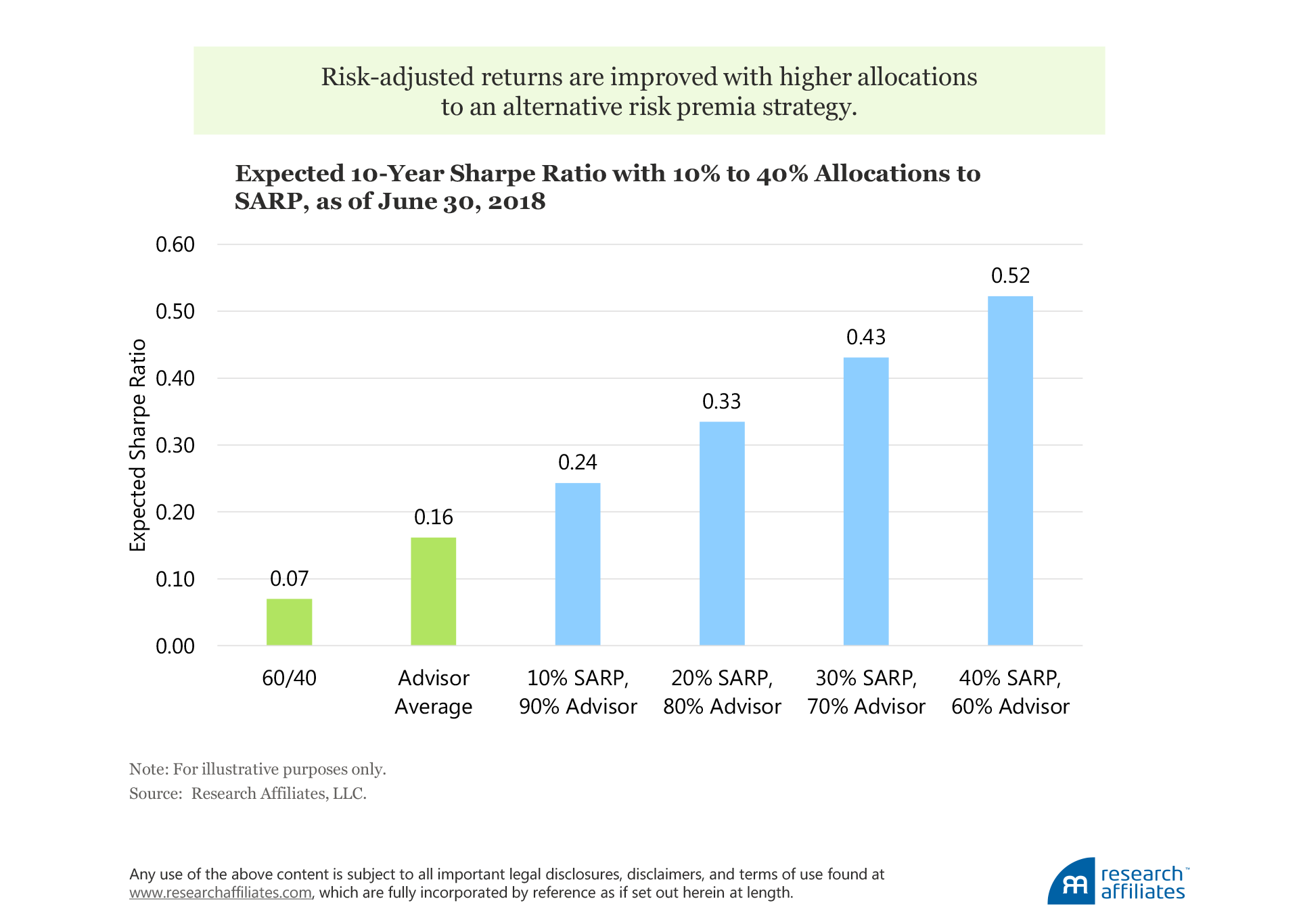

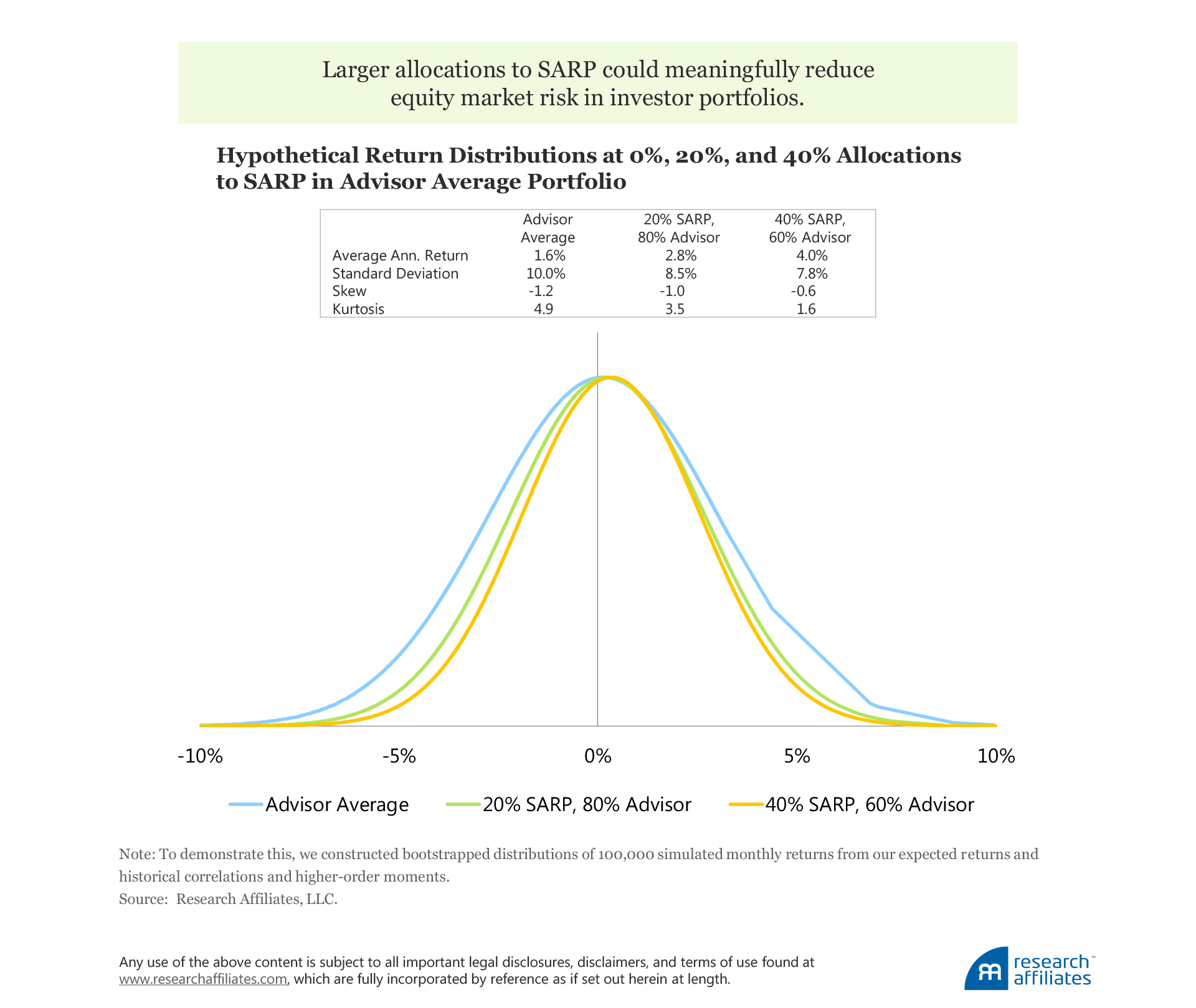

Steadily increasing exposure to the SARP approach within the Advisor Average portfolio leads to rising expected returns and falling portfolio-level volatility. An Advisor Average portfolio with a 20% allocation to the SARP strategy improves its 10-year real return prospect to 2.8% from the currently estimated 1.6%, while creating a volatility profile approximately 15% lower than that of the Average Advisor portfolio (8.4% vs. 9.9%). This benefit translates into a dramatic improvement in the potential risk-adjusted return, represented by an expected Sharpe ratio of 0.33, exceeding the Sharpe ratio of the Advisor Average portfolio by 1.1x and of a US 60/40 portfolio by 3.8x.

The probability of meeting the real return hurdle of the 5% challenge rises with increasing exposure to the SARP strategy, from less than 0.1% for a traditional US 60/40 portfolio to over 5% for an Advisor Average portfolio with 20% allocated to the alternative risk premia approach. As we mentioned earlier, doubling the allocation of SARP to 40% leads to dramatically improved odds (21.6%) of meeting the challenge. For many investors, a 40% allocation may be well outside their comfort zone, but discomfort often goes hand in hand with higher expected returns—one of Research Affiliates’ core investment beliefs.

Importantly, investors who choose to add an alternative risk premia strategy to their portfolio in order to capture these potential benefits do not necessarily need to sacrifice liquidity or transparency. Nor does such an allocation require a huge dent in investors’ wallets, particularly relative to other alternative strategies such as hedge funds.

A portfolio with a 10% allocation to SARP is poised to produce a Sharpe ratio marginally higher than that of the Advisor Average portfolio (0.24 vs. 0.16, respectively). Does this suggest that advisors need to introduce an allocation greater than 10% to make the switch worthwhile or that advisors are already capturing a large portion of the benefits associated with these strategies? A careful look produces a definitive “No.”

Because the SARP strategy has a low correlation with the Advisor Average portfolio (0.10), substantial risk reduction can be achieved even at small allocations. Although the chance of achieving the 5% challenge remains slim, the volatility reduction arising from an allocation to the strategy is meaningful and the distribution of returns begins to look more normal;8 that is, the negative skewness and fat tails associated with equity market risk become mitigated, with stronger impacts noted as allocations to the SARP strategy increase. Therefore, we conclude that a 20% or 40% allocation to an alternative risk premia strategy could greatly reduce the negative tail events and drawdown risk to which the Advisor Average portfolio is vulnerable, cutting these instances in half at a 40% allocation.

Conclusion

The prospect of meeting many investors’ desired real return target of an annualized 5% over the coming decade is not an easy feat. No wonder it’s been dubbed the 5% challenge. The good news is that investors do not need to drastically reposition their portfolios beyond tolerable risk levels, often coming with increased downside risk, return dispersion, or a large sacrifice in liquidity or transparency, in order to achieve better outcomes. Nor do investors need to consider a rare, costly, uncomfortably complex, black-box solution to get closer to their return goals. A straightforward alternative risk premia strategy that relies on robust factors combined in a liquid, transparent, and disciplined design can be an attractive option for traditional investor portfolios.

Article By Shane Shepherd, Amie Ko, Brandon Kunz – Research Affiliates