Spruce Point is pleased to issue a critical forensic “Strong Sell” report on Amdocs, Ltd. (Nasdaq: DOX or “the Company”) – an opaque company incorporated in the dodgy tax haven of Guernesy, founded in Israel, and headquartered in the United States. Given the Company’s significant exposure to AT&T and the troubled telecom industry, we believe its unusually margin stability and growing Non-GAAP earnings belie the fact that it is now struggling to generate cash flow, as evidenced by its non-transparent factoring of accounts receivables and joint venture loans.

Q4 hedge fund letters, conference, scoops etc

Our report will unravel DOX’s wasteful M&A strategy to bolster sales and earnings with aggressive use of percentage-of-completion and software development cost capitalization, and repeated one-off net tax benefits. With insider ownership at an all-time low, evidence that management is milking DOX’s cash through aggressive option comp schemes, and past allegations of improprieties by various Board members tied to option back-dating and software cost capitalization, we believe shareholders should be increasingly vigilant about the means with which DOX has gone to engineer consistent financial results, and its decision to construct a new Israeli headquarters, while providing inconsistent disclosures about the true cost.

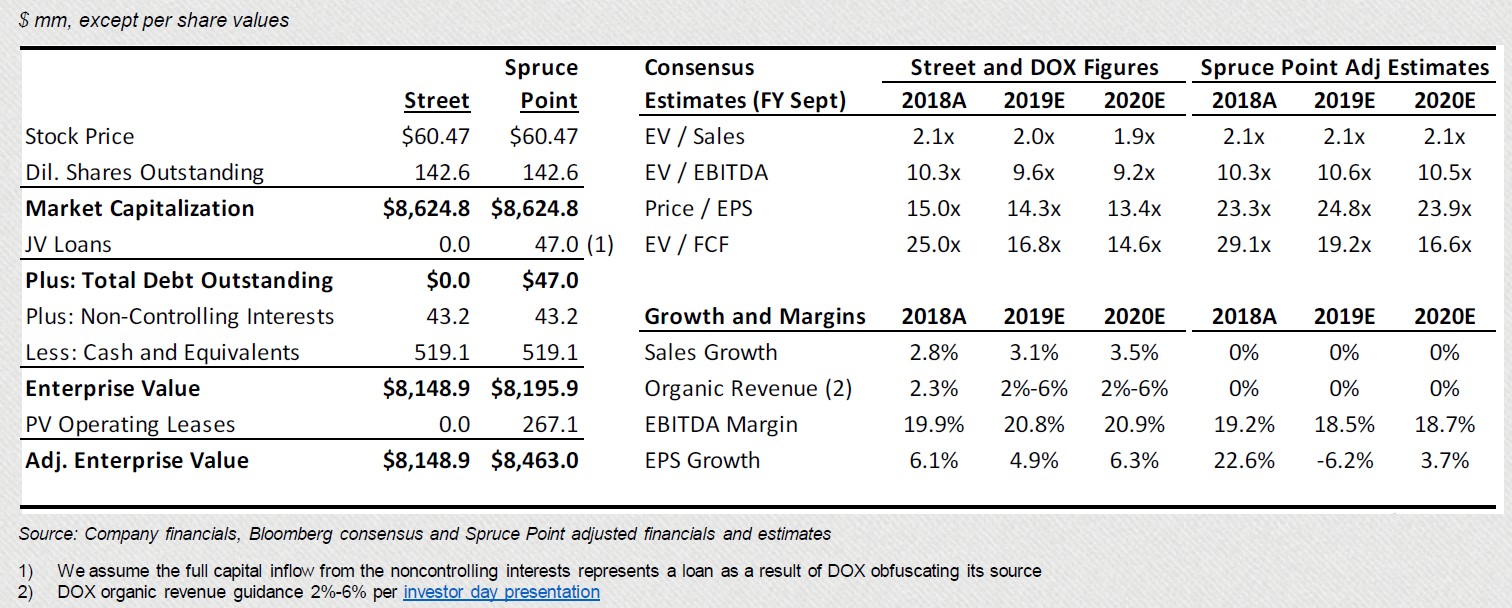

As a result, we see 25%-50% intermediate downside risk to $30.00-$45.00 per share, as investors come to terms with the fact that DOX is at best a no growth company, and at worst in its decline. We believe that DOX should not trade at a material premium to midcap technology and business process outsourcing (BPO) peers as a result of its cryptic and complex structure, below average growth, questionable accounting methods, and heightened governance concerns.

Executive Summary

Spruce Point Sees 25%-50% Downside Risk In Amdocs (NYSE: DOX): $30 – $45 Per Share

Amdocs (DOX or “the Company”) is a cryptic entity based in the tax-dodge haven of Guernsey that provides revenue management, BPO and IT services primarily to telecoms. Industry forces have dragged on sales growth to the point that Amdocs appears to be in organic decline. We believe that DOX has engineered superficial top and bottom-line growth alongside unusually stable margins through opaque M&A, aggressive percentage-of-completion accounting, software cost capitalization, and repeated one-off net tax benefits. Challenged FCF growth, self-imposed minimum cash balances, and likely leverage limits will constrain DOX’s ability to pursue growth via M&A going forward. We are also concerned that DOX is accelerating its earnings- inflating cost capitalization scheme by constructing a new Israeli campus. An obscured JV loan, receivable factoring, and capex statements which hide asset sales all point to slowed underlying FCF growth. With insider ownership at an all-time low, evidence that management is milking DOX’s cash through aggressive option comp schemes, and Board members tied to allegations of option back-dating and software cost capitalization, we believe that shareholders should keep a vigilant eye on management’s accounting practices and compensation decisions.

Hallmark Indicators Of A Company With Questionable Financials And Accounting

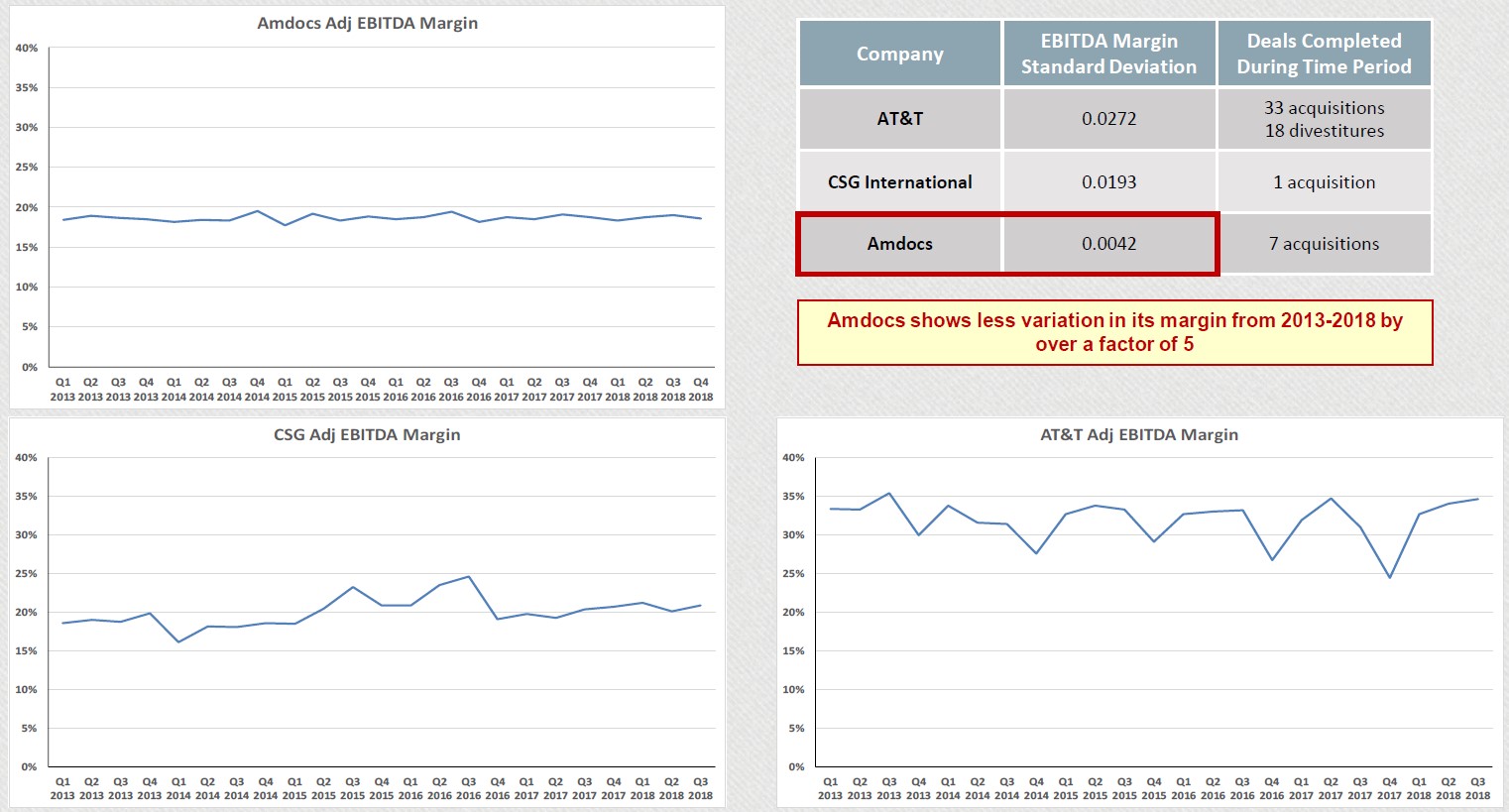

- Suspiciously Steady Margins: Amdocs shows remarkably steady margins for a firm which frequently absorbs acquisitions ($1.6B since 2012), which should have some degree of operating leverage, and whose business has come under pressure from its largest customer (AT&T). Peers and telcos show much more natural margin Unusually steady margins support our suspicion that Amdocs engages in aggressive percentage-of-completion accounting.

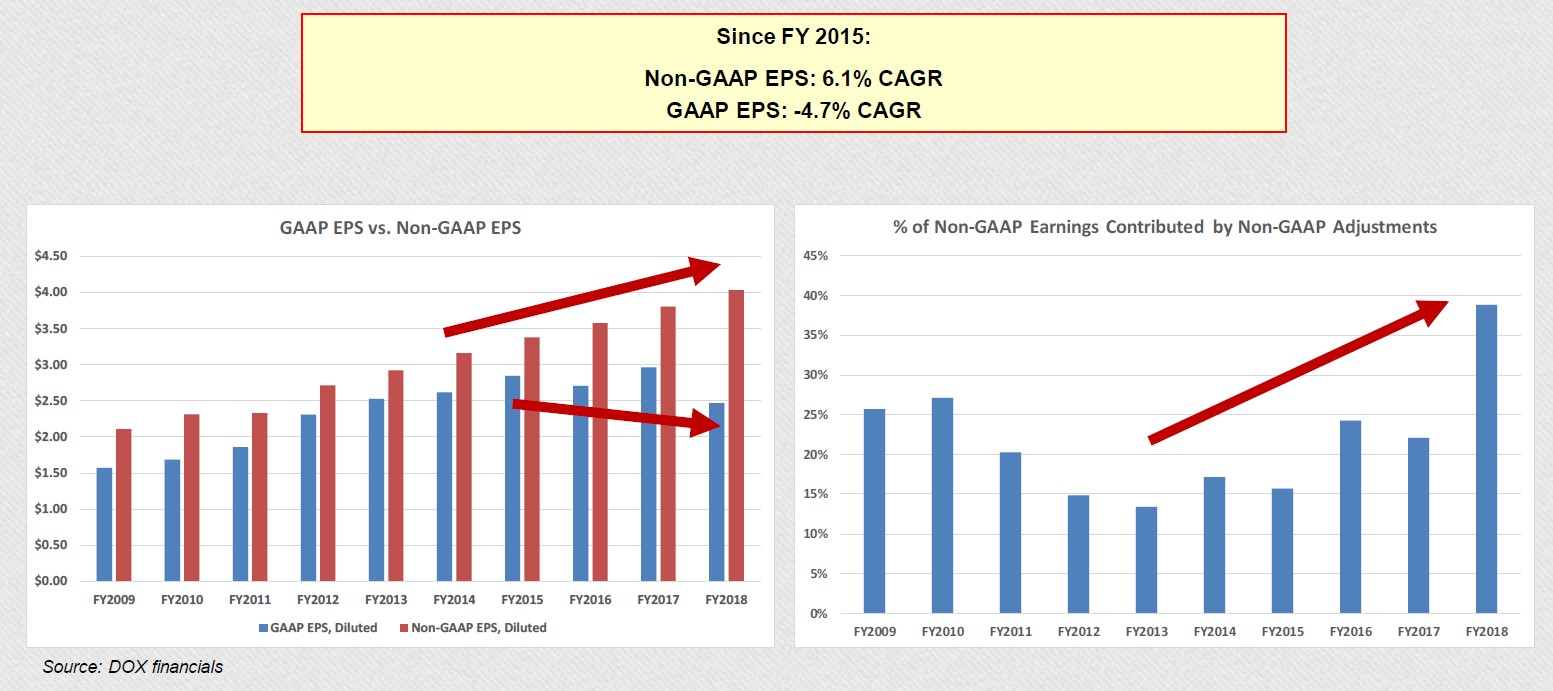

- Growing Divergence Between Adjusted And GAAP Metrics: Amdocs’ proprietary Adjusted EPS measure has grown steadily through the last 5 years, while GAAP EPS and cash flow have been flat to down over the same period despite the Company’s M&A-fueled growth. Spruce Point has observed both of these patterns among numerous companies on which it has published research, and feels that they are strong indicators of impending financial strain.

- Questionable One-Off Tax Items: DOX claims up to $60M of one-off net tax benefits on a yearly basis, with the specific sources of these benefits changing almost every year (it claimed $28M in benefits related to its spending on its new campus in FY 2018). We do not believe that these benefits – worth 10% of EBT in FY 2018 – are a sustainable source of Excluding these items, Amdocs’ tax rate looks much closer to that of most companies.

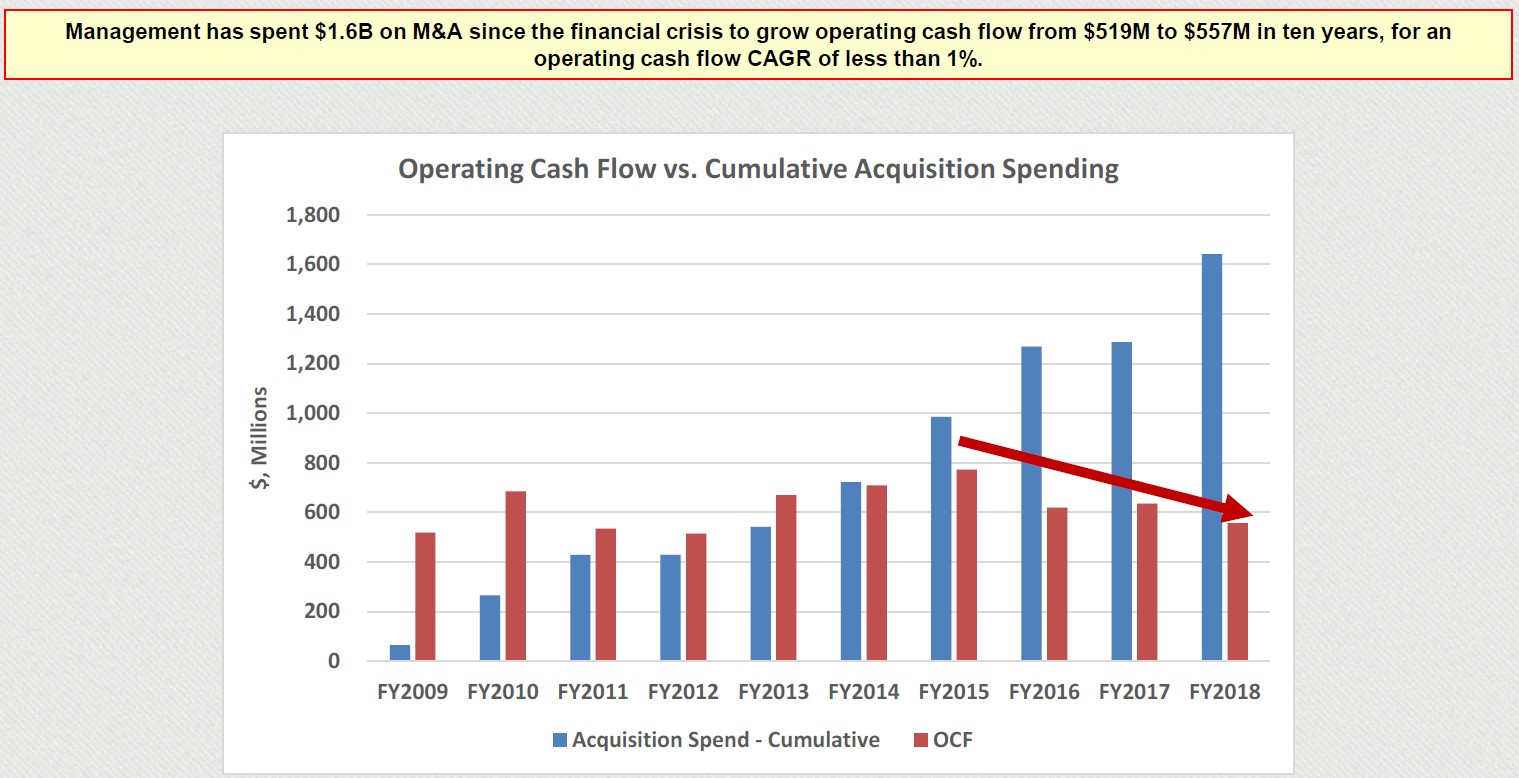

- Struggles Generating Cash: In Dec ‘18, DOX began to disclose that it factors accounts receivable (on non-transparent terms). It also obscured a loan issued via a recently-formed JV to finance its new HQ, despite saying previously that it could finance the project internally without material impact to

- Who Signs DOX’s 20-F And Credit Agreement: We observe that DOX’s Head of IR/Secretary signs its 20-F and Credit Our research shows that this is a highly unusual practice: the CEO generally signs the 20-F, while the CFO and/or Treasurer normally signs Credit Agreements.

Amdocs Engaging In M&A To Manufacture Growth

- Closely Tied To A Low-Growth Industry: As IT support for major telcos, Amdocs’ organic growth is ultimately tied to a stagnant industry – AT&T in particular (~30% of sales). Management attempts to describe industry trends such as consolidation as a tailwind for the Company, but, in reality, slow growth among telcos translates into slow organic growth for Amdocs – particularly as elements of revenue management software become less complex.

- Management Engages In Frequent M&A To Grow Sales: Amdocs has purchased a jumble of IT and media businesses through the past decade to support growth where it can’t generate its Many of these businesses appear to be only tangentially relevant to Amdocs’ core services, and are only partially integrated into Amdocs once acquired. Without these acquisitions, we estimate that Amdocs generates zero to negative organic growth.

- Management Not Transparent About Inorganic Sales Contributions: Management is frequently asked on earnings calls about the contribution of acquired businesses to total revenue. It often writes them off as “small” even when the announced purchase price is relatively sizable – and, when it does give more granular details, it appears to understate their likely contribution, thus inflating implied organic revenue growth.

Spruce Point Sees 25%-50% Downside In DOX

Non-Transparent PP&E Accounting Obfuscates Underlying Capex And Is A Sign Of Both Potential Cost Capitalization And FCF Inflation

- Explosion In European Assets Suggestive Of Cost Capitalization: DOX has seen the value of its European fixed assets more than double over the last five years. One problem: the Company has very little physical presence in Europe, nor has management discussed large efforts to grow its presence there. So what are these assets? Discrepancies between the way in which DOX and its subsidiaries account for software make us question the legitimacy of these reported assets. We believe that DOX may be capitalizing significant software development-related costs which ought to be expensed, and failing to amortize these costs once development is completed.

- Asset Sales Hidden By Non-Transparent Capex Accounting: Management discloses only net capex, grouping both purchases and sales of PP&E together on its cash flow statement. We find evidence that management has divested of assets since beginning this practice, thereby depressing reported capex and flattering free cash flow. Interestingly, in FY 2018, management did not explicitly state that its disclosed capex figure represents net capex, potentially fooling investors into thinking that Amdocs’ reported capex – surreptitiously deflated by asset sales or hidden write-downs – represents gross capex, as most investors are used to seeing.

- Irreconcilable Spending On New Israeli Campus Increases Fear Of Cost Capitalization Scheme and Cash Flow Struggles: DOX says it will spend $350M from FY18 -21 on a new Israeli HQ. Why is this needed for a no-growth company with most of its employees in India, and most of its customers in North America? We observe that DOX’s reported FY 18 campus spending is inconsistent – varying by as much as 50% of the $100M – at different points of disclosure. Furthermore, DOX obscured the fact that it received a loan for the purchase of the campus land, despite saying it could finance the project internally. Heightening our suspicion, we note that Electra Group, its Israeli construction partner, said that construction of the four building campus would cost just NIS 300m ($90m).

Highly Questionable Financing Behavior Hides True Leverage And Potentially Manipulates Tax Status

- New Accounts Receivable Factoring A Classic Sign of Stress: Management appears to rely increasingly on aggressive percentage -of-completion accounting for paper sales growth, manufacturing revenue which is not supported by cash flow. With Amdocs fast approaching its stated minimum cash balance, it has recently resorted to factoring receivables to generate cash as slow sales growth demands more M&A – but it won’t disclose the extent of its factoring. We note that this represents a non- transparent form of borrowing – convenient for a company whose closely-tied customers (AT&T, etc.) value a strong balance sheet. Based on Spruce Point’s experience, the initiation of receivable factoring is a strong indicator of near-term negative share price performance.

- Bizarre Borrowing And Investing Patterns Suggestive Of Financial Engineering: Like clockwork, Amdocs borrows ~$200M once a year at the end of one quarter, only to repay the loan just weeks later (at most). It has also historically – and inexplicably – purchased and divested of short-term investments in virtually equal amounts on a quarterly basis. Management’s desire to shift the weight of its balance sheet in certain quarters may have to do with its unique tax status as a Guernsey-domiciled entity: if the Company fails to meet certain standards as defined by the IRS, it would qualify as a “passive foreign investment company” (PFIC), which would bring materially higher taxes on U.S.-based DOX investors and precipitate forced stock sales. We suspect that management may be manipulating its balance sheet to maintain a preferable tax status for which it should no longer qualify.

Board Entrenchment, Particularly At The Audit Committee Level, Where An Original Member Was Accused Of A Software Capitalization Scheme

- Unique Structure And Insular Management Suspicious In Context: The Company is domiciled in Guernsey, an infamous tax haven. Its European subsidiaries are aggregated in the financials of its subsidiary in Cyprus – another recognized money laundering center – where DOX’s local financial statements appear to be delinquent, and where it shows limited physical assets. It does most of its business in the U.S., and most of its employees are located in India, yet its executives are almost exclusively based in Israel – and are notorious among employees for being extremely insular, protective, and driven to meet quarterly expectations.

- Entrenched Management Team, Board and Auditor Would Make Fraud Difficult To Detect: Many DOX executives have been with the Company for decades, while five Board members have an average tenure of 20 yrs. Our biggest concerns lie with the audit committee: Adrian Gardner has been on the committee since the 1998 IPO. Lawrence Perlman, former CEO of Ceridian, and another original audit committee member, was named in a (settled) lawsuit involving a $100m software development capitalization scheme: at best a pure coincidence, at worst the seeds of DOX’s current practices.

See the report here by Spruce Point Capital