So first of all let’s just get straight into dealing with that title…

Q2 2020 hedge fund letters, conferences and more

Why did I write “(Another)” New Bull Market in Global Equities?

The reason is very simple, I wrote an article in October last year, documenting the technical triggers that indicated a new bull market was getting underway in global equities.

Obviously (in hindsight) that ended up getting derailed, but it was quite an interesting case study in being right and wrong, or knowing and not knowing.

I was thinking about this the other day, and I remember responding to a tweet on Twitter, something along the lines of “nobody really knows what will happen next in markets, even when you know you don’t know”

That October article is a case study in knowing but not knowing. I “knew” that global equities were entering into a new cyclical bull market, the indicators were clear (and the bullish case stacked up beyond the technicals as well). And strictly speaking, I was “right” up until the pandemic became a clear reality.

I knew what markets were going to do conceptually, but I did not know that the “new bull market” would suffer from premature evacuation.

Fast forward to March 2020, I found myself again in possession of knowledge on the market outlook. I highlighted the emergence of a “Generational Buying Opportunity” in global equities. And, so far so good on that… (but with an obvious disclaimer at this point with regards to knowing and not knowing)

Thus this article today serves as an echo of that older New Bull Market blog from October last year, and also a follow-up to the Generational Buying blog in March.

I think importantly also, this blog addresses the growing question/concern around whether or not we have come “too far too fast” since the bottom. And by the way, when smart people think that we have come too far too fast, of course it’s worth probing into what they’re thinking, but also worth remembering that line:

“nobody really knows what will happen next in markets, even when you know you don’t know”

And you know what? Maybe it’s actually worth taking that quote and writing it up on your wall or putting a post-it note on your screen with this line as a sort of enduring keep-it-humble market-memento-mori.

That all said, let’s review some charts and indicators which lead me to “know” that we could be entering into a new cyclical bull market for global equities…

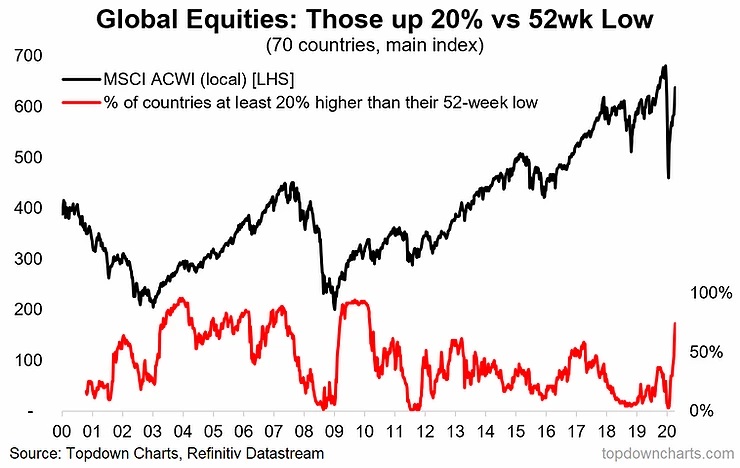

- Percentage of Countries in a “Bull Market” This is an interesting one. The red line shows the proportion of the 70 countries that we track whose main equity benchmark is up at least 20% vs its lowest point of the past year.

This is a reference to the media definition of a “bull market” as something that’s gone up at least 20%. As of the time of writing, 74% of (or 52 out of 70) countries are now in a (new) bull market.

Now… We can of course debate about what a “bull market” really is, and whether 20% makes sense, but one thing is clear. Looking at the history of this indicator over the past couple of decades: when it turns up like this – typically it means good things for the medium-term outlook for markets.

- Global Equities — Medium-Term Market Timing Signal: While the previous chart admittedly is almost a bit of a gimmick chart, this next one is the real deal, and there’s a few key things to note with its use.

Quickly on definitions: the red line again tracks the same 70 countries, but this time is presenting the percentage of countries whose main equity benchmark is positive on a year-over-year percentage basis (or simply is higher now vs this time last year).

Firstly, from a bullish/buy-signal perspective, there really are 3 signals to note:

- when the indicator collapses to washed out levels (~20% and below);

- when it does that and then turns up (like now);

- when it passes above 60%

So clearly, we have the first two signals checked off now. In terms of those signals, it’s basically also a rank order of certainty: with the first signal you run the risk of getting in too early; with the last signal you tend to get less “false positives”, but also you miss the meaty first part of the move (e.g. the MSCI All Countries World Index is up 38% off the March 23 low, at the time of writing).

Option b provides a good compromise between going too early and waiting too long. For reference, that signal first lit-up in early May.

While there are a couple of notable exceptions for the efficacy of option b (e.g. 2001), it otherwise has a solid track record for producing profitable medium-term buying signals for global equities. (But for those who want to wait for option c, stay tuned, I’ll let you know when it gets there!)

- Global Central Bank Stimulus Tailwinds: Back in March my key arguments on the compelling bullish medium-term setup for global equities consisted of: oversold technicals, extreme pessimistic sentiment, extremes reached in valuations (multi-year cheap levels)…

…and of course the monetary policy response, which was: swift + coordinated globally + coordinated with fiscal policy + targeted at the unique cashflow/liquidity challenges of this crisis + a mix of traditional and non-traditional policy tools.

In short, the speed, coordination, and magnitude of the policy response has been absolutely historic. Some folk have accused central banks of driving a wedge between markets and fundamentals, but you need to remember that monetary policy/financial conditions is perhaps THE most important macroeconomic fundamental factor for the economy and markets (and by the way, don’t forget that equities are *forward looking*).

And look, remember guys, we’re here to make money, not to try and impose our will or opinion on the markets. Price discovery is the process of pricing in all the things that matter – whether you think the things should matter or not.

“trade what you see: not what you want to see”

And yeah, basically the market tends to do well when policy stimulus is implemented…

For completeness, the channels of transmission for this are: 1. the expected future growth that may come if the stimulus works; 2. the signalling and confidence effects (that policy makers will/are actually doing something about it, and may do more); 3. the valuation uplift from a lower discount rate (or aka, when cash is zero “TINA”); and 4. the liquidity/flows/ money supply effects, if any.

The chart basically speaks for itself, but the key soundbite stats are that G3 central bank balance sheets went from contracting at a pace of -US$200B in September last year to expanding at a pace of +US$5T (capital T for TRILLIONS) now. To labor the point: stimulative macroeconomic policy settings tend to be good for risk assets.

Final Thoughts and Bottom Line

Bottom line: with historic stimulus tailwinds and a series of bullish medium-term technical signals, it looks as though a new cyclical bull market is getting underway in global equities.

As outlined, this article basically provides an echo of the October call and perhaps more importantly a follow-up on the March post. In March I highlighted the bullish medium-term case for global equities on the basis of extreme cheap valuations, oversold technicals, extreme pessimistic investor sentiment, and historic stimulus tailwinds. In this article I highlight how a number of bullish medium-term technical signals have been triggered; meaning that we need to at least consider the possibility that we may now be in the early stages of a new cyclical bull market (which could end up being a multi-year phenomenon).

For more detail on this this topic or any other specific questions get in touch…

You can contact us direct or by social media.

Best regards,

Callum Thomas

Head of Research at Topdown Charts Limited