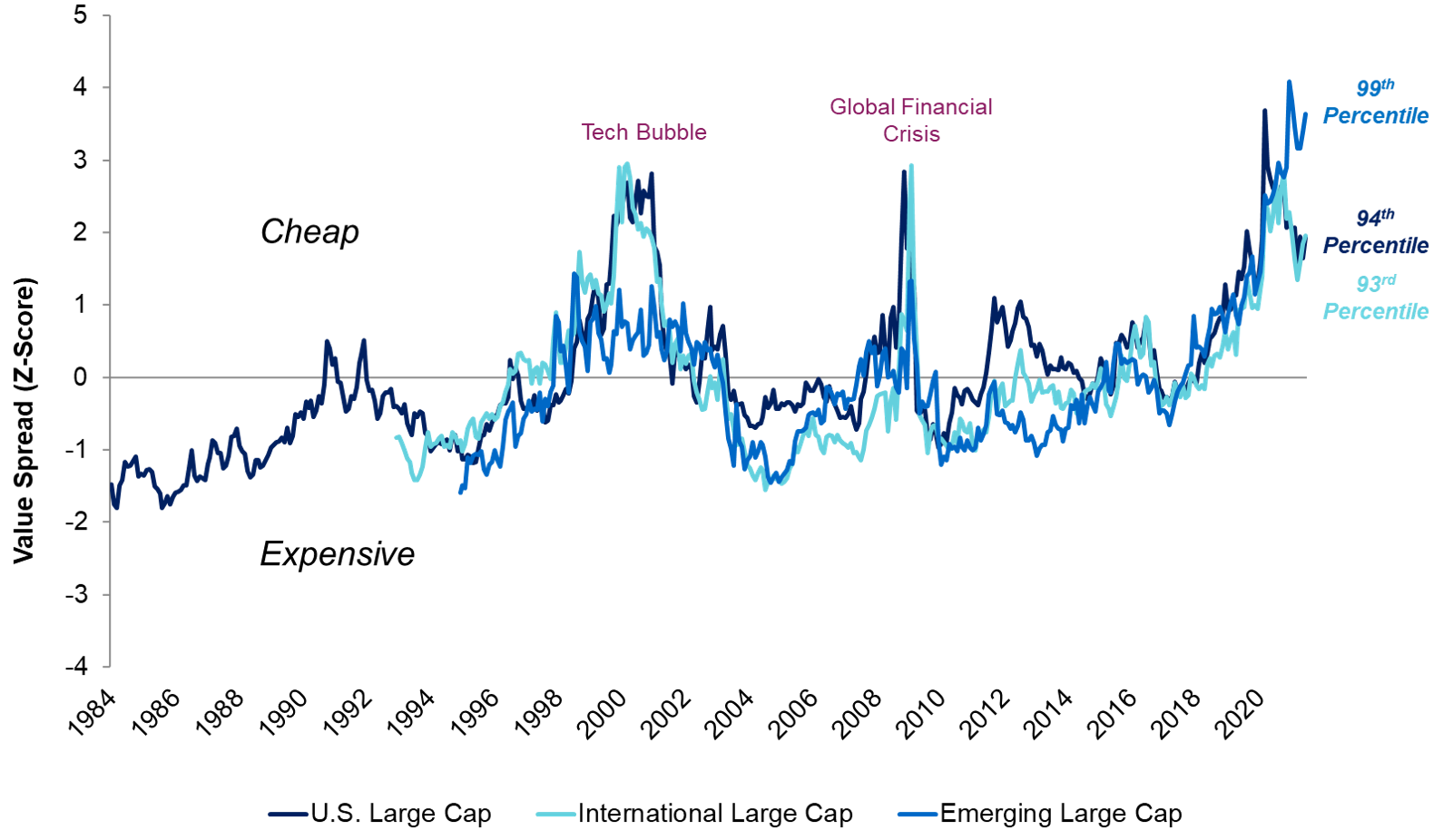

We have been discussing the attractiveness of the value factor for many months based on the unusually high value spread, which compares the valuation multiples of expensive stocks to cheap stocks. This metric is still extremely cheap… 90th+ percentile cheap across all regions.

Q2 2021 hedge fund letters, conferences and more

Value Spreads for Hypothetical AQR Industry-and-Dollar-Neutral Value Portfolios*

January 1, 1984 – June 30, 2021

*Spreads are constructed using the Hypothetical AQR Value portfolio as described below, and are adjusted to be dollar-neutral, but not necessarily beta-neutral through time.

Source: AQR. Hypothetical value compos …

We think this signals an unusually attractive forward-looking return for the value factor, but some investors have wondered if value is cheap for a reason. Maybe the fundamental prospects for value stocks are unusually poor today, justifying the high value spread? This is by far the most popular question we get from skeptics. And, yes, we have an answer that doesn’t require a four-hour time commitment nor a PhD (though finance PhDs may also be able to follow along). In a recent webisode, “Are Value Stocks Cheap for a Fundamental Reason?,” we explain why we look at the value spread, and why the current high value spread is forecasting high expected returns, not lower than usual fundamental growth rates for cheap versus expensive stocks. And we cover all of this in five minutes. We encourage all investors, both skeptics and value geeks, to listen to this new webisode, and we welcome any feedback.

Article by Cliff Asness, AQR