Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Q3 hedge fund letters, conference, scoops etc

Register for our CE-eligible webinar on this topic here. This webinar will be on November 15 at 4:15pm ET.

Advisors tout the obvious advantages of liquid portfolios and investments. But they are slower to mention that this liquidity comes at a cost. A vast literature in finance supports the idea that less liquid assets offer higher expected returns. This is the so called “liquidity premium.”

Given these premiums, advisors should look more closely at their clients’ investments as well as portfolio design from a liquidity perspective. Investors, particularly those with long-term goals, may be paying for daily liquidity they don’t need. By ignoring liquidity premiums, advisors are not maximizing the funds of their clients.

What is liquidity – and what is the liquidity premium?

Liquidity is a slippery topic. There is no universal definition, except for maybe that of economist Maureen O’Hara, who said, “liquidity is hard to define but you know it when you see it.” Part of the problem is that liquidity is phase dependent. It varies through time and by market condition.

In general, liquidity refers to how easy it is to buy or sell assets. This turns out to be a multi-dimensional concept. It involves speed (how long it takes to sell something), cost (the bid-ask spread), and the price impact of a trade. Volume, used by some analysts as a measure of liquidity, is a very poor proxy for liquidity. More telling is the price impact induced by volume, that is, how much can you trade without moving the price?

More interesting for investors is what this means for returns. Investors need to be compensated for the cost of trading less liquid securities, as well as the risk that assets could turn illiquid in a crisis. The result is that these securities should offer investors higher expected returns, the “liquidity premium.”

Liquidity premiums have been found in many different asset classes, such as stocks or corporate bonds. They can be seen in even the most seemingly liquid asset class of all: US Treasury securities. There are liquidity differences in the Treasury market, with the older “off the run” securities less liquid than their newly issued on the run counterparts. Both of course have the same risk of default, yet there are differences in yield. One research study found that the less liquid off-the-run Treasury notes had an average yield of 43 basis points higher than their on-the-run counterpoint.

Liquidity premiums are difficult to quantify and vary by market condition. However, the CEO of the Harvard Management Company, Jane Mendillo, in 2014 put a number on them, in an expected returns framework. She said, “We should be getting an incremental return for that illiquidity – and we call that our illiquidity premium – of at least 300 basis points annually on average over what we are expecting in publicly traded stocks.”

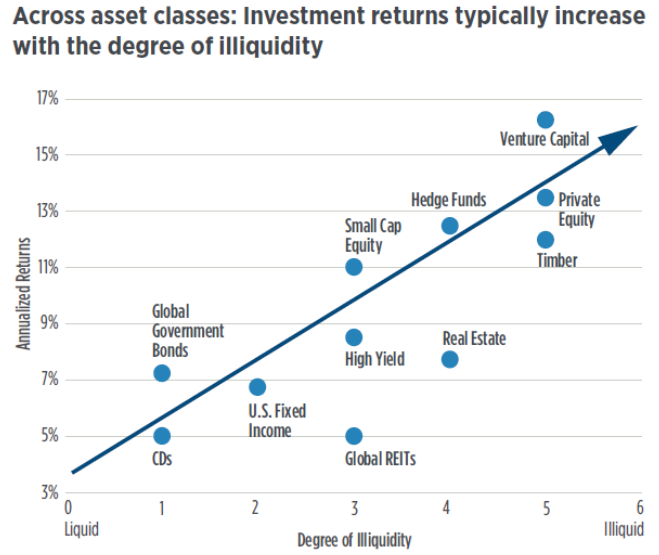

The idea that there are liquidity premiums within an asset class is well-established. More controversial and hotly debated is the idea that liquidity can explain the return differences between asset classes, given their different risks, characteristics, and role for management skill. Nonetheless, researcher Antti Ilmanen, found a relationship between an asset classes’ degree of illiquidity and expected returns.

Liquidity premiums (along with better information) therefore go a long way in explaining the seeming “magic” of the high returns of alternative asset managers.

Read the full article here by David Adler, Advisor Perspectives