Asia Frontier Capital (AFC) newsletter for the month of September 2022.

“Most people get interested in stocks when everyone else is.

The time to get interested is when no one else is.

You can’t buy what is popular and do well.”

– Warren Buffett – American business magnate, investor, and philanthropist

Q3 2022 hedge fund letters, conferences and more

AFC Funds Performance Summary

- The NAV given is for the lead share series for the relevant master fund. Investors’ holdings may be in a different share class, series, or currency and have a different NAV. See the factsheets and/or your statement for full details.

- Between 31st May 2017 and 30th November 2021 the benchmark was adjusted to be 37% of the MSCI Frontier Markets Asia Net Total Return USD Index “MSCI Index” and 63% of the Karachi Stock Exchange 100 Index in USD due to the removal of Pakistan from the MSCI Index during this period.

- NAV and performance figures are all net of fees.

AFC Iraq Fund outperforms

The AFC Iraq Fund once again displayed its diversification benefits, especially in a month when all major global markets witnessed a steep selloff. The AFC Iraq Fund, with a year-to-date return of +3.8%, is one of only a few long-only equity funds showing a positive return so far in 2022.

AFC back on the road

AFC has once again begun its on-the-ground visits to countries and conferences after a gap of almost three years due to pandemic travel restrictions. Ruchir Desai, co-fund manager of the AFC Asia Frontier Fund, visited Dubai to attend the largest frontier markets conference globally and met with companies from Bangladesh, Cambodia, Georgia, Jordan, Kazakhstan, Oman, Pakistan, Sri Lanka, and Vietnam.

The key takeaway from the conference was that though headwinds remain in the form of rising global interest rates, valuations for many frontier markets are now very attractive after taking a 12-18 month view and on a bottom-up basis, almost all the companies we met with have very strong fundamentals.

On a country level, it was not surprising that Vietnam received the most attention given its strong macro and supply chain-driven story, while Georgia continued to make its case as the key beneficiary of the conflict in Ukraine.

With AFC being back on the road again, keep an eye out for the resumption of our travel reports starting in December 2022.

Asian Frontier Markets Update Webinar – Friday, 28th October 2022

AFC will hold its quarterly update webinar on Friday, 28th October 2022 at 9:00am NY, 2:00pm UK, 3:00pm Swiss and 9:00pm HK/SG time. As usual, the webinar will discuss the outlook for Asian frontier markets with a focus on our AFC Asia Frontier Fund, AFC Iraq Fund, AFC Uzbekistan Fund and AFC Vietnam Fund.

The speakers on the webinar will be:

- Thomas Hugger, CEO & Fund Manager

- Ruchir Desai, Co-Fund Manager of the AFC Asia Frontier Fund

- Ahmed Tabaqchali, Chief Strategist of the AFC Iraq Fund

- Scott Osheroff, CIO of the AFC Uzbekistan Fund

- Vicente Nguyen, CIO of the AFC Vietnam Fund

The webinar will run for an hour and will include a 15-minute Q&A session after the fund managers’ presentations.

The webinar will highlight the following key points:

- Impact of a hawkish Fed on Asian frontier economies and stock markets

- Impact of slower global growth on Asian frontier economies

- Which countries are still benefitting from a supply chain shift despite a global economic slowdown?

- What is the investment outlook for Asian frontier markets?

- Outlook for the AFC Asia Frontier Fund / AFC Iraq Fund / AFC Uzbekistan Fund / AFC Vietnam Fund

AFC Iraq Fund – Manager Comment

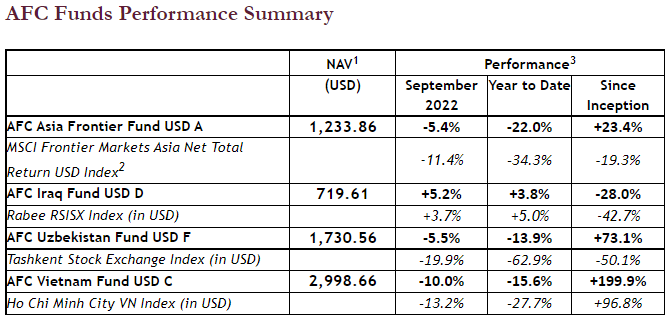

The AFC Iraq Fund Class D shares returned +5.2% in September with a NAV of USD 719.61, outperforming its benchmark, the Rabee Securities RSISX USD Index (RSISUSD index), which gained 3.7% during the month. The fund was up 3.8% year to date versus the index which was up 5.0%. Since inception, the fund has lost 28.0% while the RSISUSD index is down 42.7%.

During the month, the market’s average daily turnover showed signs of revival with the end of the 40-day Arbaeen pilgrimage on 17th September, which coupled with the RSISX USD Index’s second consecutive monthly increase which moved the index towards the upper end of its two-year up-trending channel (chart below) and reinforced the market’s positive technical picture. The macroeconomic fundamentals discussed here five months ago argue that the market’s two-year uptrend will likely remain in force, however, its upward slope might moderate, or even go sideways, as the liquidity injection – as a consequence of the passage of the supplementary budget – works its way through the economy and eventually into the equity market.

The significance of the passage of the supplementary budget to the economy, and the transformative impact of the higher oil price environment on Iraq, were discussed here in “Supplementary Budget Stabilises the Market” and on 28th July 2022 during AFC’s “Asian Frontier Markets Update” webinar.

RSISX USD Index versus Average Daily Turnover

(Source: Iraq Stock Exchange, Rabee Securities, AFC Research, data as of 30th September 2022)

Seven of the index’s constituents were up or flat with the National Bank of Iraq (BNOI) up 13.7%, Al Mansour Bank (BMNS) up 8.5%, the Bank of Baghdad (BBOB) up 8.0%, Al-Mansour Pharmaceutical Industries (IMAP) up 3.0%, the Commercial Bank of Iraq (BCOI) up 2.0%, and AsiaCell (TASC) up 0.1%, while Al-Kindi of Veterinary Vaccines and Drugs (IKLV) was flat. The decliners were led by Kharkh Tour Amusement City (SKTA) down 3.3%, followed by Iraqi for Seed Production (AISP) down 2.3%, and Baghdad Soft Drinks (IBSD) down 2.0%.

Political Stalemate and the Theatrics of Violence

The end of the violent clashes of 29th and 30th August 2022 gave way to a truce of sorts between the Sadrist Movement (the apparent winners of the October 2021 parliamentary elections), and the Coordination Framework (the apparent losers of these elections); as both parties sought to defuse tensions, especially during the important last 10 days of the 40-day Arbaeen pilgrimage. After this, moves by the Coordination Framework to cement its parliamentary advantage – made possible by the resignations of the Sadrist Movement’s parliamentarians – through holding a parliamentary session on 28th September, raised fears of a repeat of the series of events that led to the violent clashes of last month. Following this script, armed groups headed to Baghdad’s Green Zone on 28th September, and Baghdadies were readying themselves for a repeat of the violent clashes of 29th and 30th August. However, after a few hours of minor armed exchanges, the script was flipped, and the melodrama ended quicker than the lead up to it – so quickly that the city’s cleaning teams began cleaning at night, and Baghdad returned to normal before midnight.

Cleaning Crew in Baghdad’s Tahrir Square

(Source: NAS News, as of 28th September at 23.36 hrs)

Youth movements’ plans for demonstrations on 1st October to commemorate the third anniversary of the October 2019 youth-led nationwide protests raised fears that these demonstrations would be taken-over by supporters of the Sadrists Movement to be used in their conflict with supporters of the Coordination Framework. These fears did not materialise; however, this does not remove the potential for further conflict as the political impasse over government formation is far from over – but they are highly improbable to be anywhere as violent as those of the last month.

As written here over the last two months, both parties in the conflict, irrespective of their fierce rivalry, have been members of the all-inclusive governments formed following successive elections post the US invasion in 2003. Importantly, as major players in the post-2003 ethno-sectarian political system, both parties have built substantial patronage networks, and consequently could risk the loss of the wealth and sources of economic rent created by these networks, if their conflict evolved into a civil war.

In the meantime, the status-quo is retained by the parties in conflict, which despite the continued political uncertainty, would be a preferred solution for all political parties, as it would preserve the country’s ethno-sectarian parties’ share of the state’s resources achieved in the 2018 elections, while they work on the torturous process of modifying the elite bargain that has kept them in power since 2003 to accommodate the post-election developments.

Markets Continue to Discount and Look Through the Political Impasse

For the second month in a row, and in a similar fashion to last month, the markets were discounting and looking through the political impasse. The Rabee Securities RSISX USD Index was flat throughout the month but began to rise just as the political impasse was showing signs of turning to violence to close the month up 3.7%, and up 5.0% for the year. Whereas in the currency market of the Iraqi Dinar (IQD) versus the USD, the spread between the official exchange rate and the parallel market exchange rate (delta in the chart below) was essentially flat for the month, indicating stability of the parallel exchange rate.

USD/IQD Exchange Rate

(Source: Central Bank of Iraq, AFC Research, data as of 30th September 2022)

The positive market action in both the stock and currency markets for the second month in a row in response to similar negative political developments is encouraging. While more data is needed for confirmation, the positive actions imply that the markets are discounting events along the logic proposed above and discussed here over the last few months.

The year-to-date performance of the AFC Iraq Fund, and the RSISX USD Index, are now well ahead of global benchmarks, signifying the diversification benefits of the fund and Asian frontier markets which have a low correlation with global markets, especially during this period of global market volatility and macroeconomic uncertainty. Furthermore, the index’s 5.0% increase year-to-date, on the back of a strong year in 2021 in which the index was up 21.4%, while still 59.1% below its 2014 peak, shows solid signs of recovery – all of which indicate that its risk-reward profile is very attractive compared with most global markets (chart below).

Normalized Returns for the RSISUSD Index vs MSCI World Index, MSCI Emerging Markets Index and MSCI Frontier Markets Index

(Source: Bloomberg, data as of 3rd October)

At the end of September 2022, the AFC Iraq Fund was invested in 14 names and had a cash level of −1.4%. The fund invests in both local and foreign-listed companies that have the majority of their business activities in Iraq. The markets with the largest asset allocation were Iraq (99.0%), Norway (2.0%), and the UK (0.4%).

The sectors with the largest allocation of assets were financials (67.7%) and consumer staples (14.3%). The fund’s estimated weighted harmonic average trailing 12 months P/E ratio (only companies with profit) was 7.97x, the estimated weighted harmonic average P/B ratio was 0.93x, and the estimated weighted average portfolio dividend yield was 2.47%.

Factsheet AFC Iraq Fund (non-US)

AFC Asia Frontier Fund – Manager Comment

The AFC Asia Frontier Fund (AAFF) USD A-shares returned −5.4% in September 2022 with a NAV of USD 1,233.86. The fund outperformed the MSCI Frontier Markets Net Total Return USD Index (−9.3%), the MSCI World Net Total Return USD Index (−9.3%), and the MSCI Frontier Markets Asia Net Total Return USD Index (−11.4%). The performance of the AFC Asia Frontier Fund A-shares since inception on 30th March 2012 now stands at +23.4% versus the benchmark, which is down by −19.3% during the same period. The broad diversification of the fund’s portfolio has resulted in lower risk with an annualised volatility of 10.8% and a correlation of the fund versus the MSCI World Net Total Return USD Index of 0.54, all based on monthly observations since inception.

A stronger U.S. dollar and continued hawkishness from the U.S. Fed rattled global stock markets. With market expectations for U.S. interest rates to peak out getting extended into the first half of 2023, global stock markets are expected to remain volatile. However, as we have discussed in past manager comments, this volatility would be a good time to start building positions in frontier and emerging markets as valuations have only gotten more discounted and attractive in the last few months.

As the chart below shows, the P/E ratio of the AFC Asia Frontier Fund at only 7.3x is now even below the level it reached during the peak of the pandemic in 2020. Fundamentals of the companies we own are extremely strong and there is now clear value on offer in Asian frontier markets with a 12-18 month view in mind.

The big news from our universe in September was Chinese President Xi Jinping’s visit to Kazakhstan. This was President Xi’s first visit outside of China after the onset of COVID-19. In our view, this visit sent a powerful message to Russia from China and Kazakhstan regarding any future adventurism in Central Asia in which China has many interests.

Hence, though there are geopolitical concerns surrounding Central Asia and Kazakhstan, we believe this visit by President Xi to Kazakhstan will help balance and support the region going forward and put a lid on investor concerns about potential Russian hostility in the region.

Despite the gloom and doom in the global world, Vietnam’s macroeconomic engine is firing on all cylinders, with 3Q22 GDP growth coming in at +13.7%. Though there was a favourable base due to last year’s lockdown, in the first nine months of 2022, GDP growth came in at +8.8%, the highest for this period since 2011.

The impact on Vietnam from slower economic growth in the U.S. and Europe is a valid concern, however as the GDP growth results show, Vietnam is clearly seeing economic momentum and export growth was also still healthy at 10% in September 2022.

(Source: Bloomberg)

Bangladesh’s export momentum is also continuing with export growth of 36% in August 2022, taking the year-to-date export growth to a strong 36%. Bangladesh’s garment sector continues to make inroads into the U.S. and European markets not only due to competitive prices but also due to the supply chain shift from China.

Bangladesh has almost reached China’s market share for garment exports to the European Union (E.U.), for example, with USD 11.3 bn of garment exports in the first six months of 2022 against China’s USD 12.2 bn.

Bangladesh Export Momentum Remains Steady (Monthly Exports in USD bn)

(Source: Bangladesh Export Promotion Bureau)

Sri Lanka was one of the outliers in global markets with a positive return in September. The Colombo All Share Index rallied for a second month in a row with a gain of 9.5% this month. Though the fund’s current exposure to Sri Lanka is small at 2.7%, our holdings have done well, led by John Keells Hotels as a more stable situation in the country has led to an increase in tourist arrivals. Furthermore, John Keells Hotels generates most of its revenues from the Maldives where tourist arrivals are back to pre-pandemic levels.

The Sri Lankan government also passed a new casino licensing regulation which we believe will go a long way in making the country an attractive tourist destination in the longer term. The fund holds John Keells Holdings, whose Cinnamon Life multi-use project in Colombo should benefit since it has plans to set up a casino in its premises.

John Keells Hotels in Sri Lanka has Outperformed the Colombo All Share Index as Tourist Arrivals Witness a Recovery

(Source: Bloomberg, % change in prices between 31st December 2021 – 30th September 2022)

The best performing indexes in the AAFF universe in September were Laos (+36.3%) and Sri Lanka (+9.5%). The poorest performing markets were Vietnam (-11.6%) and Pakistan (-2.9%). The top-performing portfolio stocks this month were a Sri Lankan tobacco company (+14.4%), a Sri Lankan consumer and healthcare conglomerate (+10.0%), a Maldivian resort operator listed in Sri Lanka (+9.1%), a diversified Sri Lankan conglomerate (+7.4%) and a Pakistani aluminium can producer (+7.3%).

In September, the fund exited its investment in a Mongolian hotel in Ulaanbaatar and added to existing holdings in Mongolia.

At the end of September 2022, the portfolio was invested in 75 companies, 2 funds and held 6.5% in cash. The two biggest stock positions were a convenience store operator (4.7%) and a beverage producer (3.4%), both in Mongolia. The countries with the largest asset allocation were Mongolia (15.9%), Iraq (14.2%), and Vietnam (12.3%). The sectors with the largest allocation of assets were consumer goods (24.3%) and materials (12.1%). The fund’s estimated weighted harmonic average trailing 12 months P/E ratio (only companies with profit) was 7.33x, the estimated weighted harmonic average P/B ratio was 1.13x, and the estimated weighted average portfolio dividend yield was 2.62%.

Factsheet AFC Asia Frontier Fund

Factsheet AFC Asia Frontier Fund (non-US)

Presentation AFC Asia Frontier Fund

AFC Uzbekistan Fund – Manager Comment

The AFC Uzbekistan Fund Class F shares returned −5.5% in September 2022 with a NAV of USD 1,730.56, bringing the return since inception (29th March 2019) to +73.1%, while the year-to-date return stands at −13.9% at the end of September 2022. On an annualized basis, the fund returned +16.9% p.a. with a Sharpe ratio of 1.06.

Amid extreme volatility in global financial markets in September as governments around the world race to raise interest rates in an attempt to stem inflation, while others negotiate IMF bailouts due to collapsing foreign exchange reserves, Uzbekistan, while insulated from this volatility, saw some selling pressure in the stock market during the month. This impacted the performance but also allowed the AFC Uzbekistan Fund to acquire some blocks of shares at attractive prices.

AFC Uzbekistan Fund valuations as of 30th September 2022:

| Estimated weighted harmonic average trailing P/E (only companies with profit): | 5.15x |

| Estimated weighted harmonic average P/B: | 0.90x |

| Estimated weighted portfolio dividend yield: | 3.40% |

Uzbekistan heads 22nd meeting of SCO

The Shanghai Cooperation Organisation (“SCO”) was established in 2003 as an amendment to an earlier organisation between China, Russia, and Central Asian countries with a focus on economic, military, and cultural cooperation. An annual meeting is held with all member states which currently includes China, India, Russia, Kazakhstan, Kyrgyzstan, Pakistan, Tajikistan, Iran, and Uzbekistan (observing nations include Afghanistan, Belarus, and Mongolia, with over a dozen other nations as either observers or guest attendees) where various topics on regional cooperation are held.

While the organisation has been argued as being ineffective at driving regional development, the organisation’s membership growth over the years is certainly indicative of a bifurcating world. The SCO now represents the majority of countries in what we refer to as the “New Fertile Crescent”, an economic corridor stretching from the Middle East to Central Asia, including Russia and China. This is a region which should see sustained growth over the coming years as it hosts a large, young population, manufacturing infrastructure, is relatively self-sufficient in energy and food, and has varying degrees of protectionist policies to support the domestic economy, rather than playing into the hands of western organisations and opening their economies to free trade as part of the globalisation movement of the past several decades.

The SCO’s 2022 meeting was held on 15th and 16th September 2022 in Samarkand, Uzbekistan, the heart of the ancient silk road. Much of the press covered the meeting between Xi Jinping and Vladimir Putin as this was Xi’s first trip abroad (after a visit to Kazakhstan days before) since the start of the COVID-19 pandemic. While the conference was overshadowed by the war in Ukraine, the highlight for Uzbekistan was agreeing with China to increase bilateral trade from USD 8 billion in 2021 to USD 10 billion in 2022. Further, China, Kyrgyzstan, and Uzbekistan signed an agreement to pursue the construction of a railroad across Kyrgyzstan which would further integrate Central Asia into the regional economy and lower logistics costs for Uzbekistan.

However, when all is said and done, in our view the biggest takeaway from the conference is that it shined a light on Uzbekistan’s fast-growing and dynamic economy (the Asian Development Bank recently raised its 2023 GDP forecast from 4.5% to 5% and the EBRD did the same, from 5.5% to 6.5%) and should lead to continued foreign investment in the country, namely in the areas of manufacturing, agriculture, and logistics.

In this regard, the most recent high-profile announcement of foreign direct investment came on 29th September 2022 by Mareven Food Holdings, a Japanese-Vietnamese joint-venture which announced a USD 125 million investment in the Angren Free Economic Zone (near the capital city, Tashkent) between 2023 and 2031 to produce instant noodles, pasta, drinks, canned food, and sauces. 50% of production is expected to be sold in the domestic market with the balance to be exported to neighbouring countries, giving further validation to our viewpoint that Uzbekistan will become the manufacturing and logistical heartland of the greater Central Asian region.

Capital Markets News

As economic growth continues apace, we continue to see positive results from the fund’s holdings. Over the past several weeks, new dividend announcements were made for 2021 earnings distributions. ToshkentVino Kombinat (TKVK) and Biokimyo (BIOK), a consumer goods conglomerate and white spirits producer announced 2021 dividends which translate into dividend yields of 10.74% and 14.61% as of 30th September 2022.

With double-digit dividend yields amid inflation of 12.3% (much better than the situation of double-digit inflation in Europe for example), the fund’s position in TKVK has managed to appreciate by 39%, and 82% for BIOK. This is down from the 20% to 30% yields we saw in the first few years we began investing in Uzbekistan. We therefore expect a further yield decline and overall multiple expansion as stock market liquidity continues to improve, accelerating this early re-rating as investors allocate capital toward “blue-chip” names, which are the core holdings of the fund.

At the end of September 2022, the fund was invested in 27 names and held 7.5% in cash. The portfolio was allocated to Uzbekistan (92.41%) and Kyrgyzstan (0.04%). The sectors with the largest allocation of assets were materials (45.6%) and financials (28.0%). The fund’s estimated weighted harmonic average trailing 12 months P/E ratio (only companies with profit) was 5.15x, the estimated weighted harmonic average P/B ratio was 0.90x, and the estimated weighted average portfolio dividend yield was 3.40%.

Factsheet AFC Uzbekistan Fund (non-US)

Presentation AFC Uzbekistan Fund

AFC Vietnam Fund – Manager Comment

The AFC Vietnam Fund returned −10.0% in September with a NAV of USD 2,998.66, bringing the year-to-date return to −15.6% and return since inception to +199.9%. The fund outperformed the benchmark, the Ho Chi Minh City VN Index, which lost 13.2% in September 2022 and has lost 27.7% year to date in USD terms. The fund’s annualized return since inception stands at +13.3% p.a. The broad diversification of the fund’s portfolio resulted in an annualized volatility of 14.49%, a Sharpe ratio of 0.86, and a low correlation of the fund versus the MSCI World Index USD of 0.56, all based on monthly observations since inception.

Market Developments

One of the main topics for global investors in September was the renewed worry about a recession in the U.S. and Europe, after central banks aggressively hiked interest rates. This triggered a sharp selloff in many stock markets around the globe this month.

With higher-than-expected interest rate increases, the markets seem to go through a crisis of confidence, wondering how far the Fed and ECB will need to hike rates in order to bring inflation back under control.

September Stock Market Performance (in USD Terms)

Also, Vietnam’s central bank decided to increase its policy rate by 100 basis points a little bit more than a week ago in an attempt to keep inflation under 4% this year. This rare monetary tightening move by the State Bank of Vietnam followed shortly after rate hikes by the U.S. Federal Reserve, the ECB (European Central Bank), the Bank of England and other central banks around the region as inflation rose across the world.

The Strong U.S. Dollar

The reason for the USD strength is that in times of elevated geopolitical risk and macro-economic uncertainty around the world, the U.S. dollar benefits from its perceived safe haven status. Also, the Fed has been much more aggressive in hiking rates than its peers.

But the situation in Vietnam doesn’t look as bad, given its strong macro-economic numbers. The 4.4% weakening of the Vietnamese dong versus the USD since the beginning of the year compares relatively favourably to most other Asian countries.

Depreciation versus the USD in 2022

(Source: Bloomberg, AFC Research)

Vietnam’s inflation seems to be under control

In order to carefully control inflation, the Vietnamese government, through its petrol and oil price stabilisation fund, intervened in the market to bring the petrol price from its recent peak of VND 32,873 per litre down to VND 22,580 per litre (around -31%). The government reduced for example taxes and fees on petrol prices and improved policies to increase production of local oil refineries. The latest CPI numbers from end of September showed an inflation number of 2.73% yoy which seems to be very manageable.

(Source: Petrolimex, AFC Research)

Even though inflation is not a concern currently in Vietnam, the latest 100 basis point rate hike by the State Bank of Vietnam showed that it is determined to keep inflation below its 4% target this year. This latest monetary tightening increased the discount rate from 2.5% to 3.5% and the refinancing rate from 4% to 5% per year. Also, interest rates of Vietnamese dong-denominated deposits will increase by 0.3% to 1%, depending on maturities. The Vietnamese stock market dropped by a moderate -0.94% after the interest hike announcement, but as expected insurance stocks jumped strongly the same day. As mentioned in our previous reports, higher deposit interest rates have a positive impact on insurance companies’ profitability, since the large bank deposits generate higher interest income which contributes more than 80% of insurance companies net profit. This is also the reason why our fund was able to perform somewhat better than the VN Index in September, given that around 20% of our portfolio is invested in insurance stocks.

Insurance Sector Outperformed the VN Index in September 2022

(Source: HSX, AFC Research)

Vietnam’s economic growth story on track

The Vietnamese Government just released its third quarter macro-economic numbers with an impressive Q3/2022 GDP growth of 13.67%, the highest in more than 2 decades, but also partly due to the comparison period being a period of weak growth during the COVID-19 pandemic (low base effect). The economy has improved in all aspects including manufacturing (+12.1%), exports (+17.2%), FDI (+12.1%), and retail sales (+21%). These numbers compare very favourably with Western economies and other big Asian countries such as South Korea, Japan, China, and India.

Q3/2022 Macro-economic Numbers

(Source: GSO, AFC Research)

After successfully combatting COVID-19, Vietnam is considered to be one of the fastest growing countries in the world. According to Nikkei Asia Research, Vietnam ranks number 2 in terms of speed of recovery from the latest pandemic.

Nikkei COVID-19 Recovery Index as of August 31st

(Source: Nikkei Asia Research)

Vietnam the only country in Asia-Pacific to be upgraded by Moody’s in 2022

In September 2022, Moody’s Investors Service upgraded Vietnam’s long-term issuer and senior unsecured ratings to Ba2 from Ba3 and changed the outlook to stable from positive. Vietnam is the only country in the Asia-Pacific and one of four countries globally to have ratings upgraded by Moody’s since the beginning of this year! This shows Vietnam’s economic strengths and greater resilience to external macroeconomic shocks that are indicative of improved policy effectiveness. Moody’s expects the situation should continue as the economy benefits from supply chain reconfiguration, export diversification and continued inbound investment in manufacturing. Over the past 10 years, Vietnam has continued to improve its economic fundamentals (current account, trade balance, foreign reserves) and hence Moody’s had upgraded Vietnam’s credit rating from B2 in 2012 to now Ba2 in September 2022.

Vietnam Credit Rating by Moody’s

(Source: Moody’s, MoF, AFC Research)

At the end of September 2022, the fund’s largest positions were: Agriculture Bank Insurance JSC (7.9%) – an insurance company, PVI Holdings (6.6%) – also an insurance company, Power Engineering Consulting JSC No. 2 (5.6%) – a consulting firm, Minh Phu Seafood Corp (5.4%) – a seafood company and Lam Dong Minerals, and Building Materials JSC (5.0%) – a building material supplier.

The portfolio was invested in 48 names and held 2.7% in cash. The sectors with the largest allocation of assets were consumer (42.7%) and financials (27.5%). The fund’s estimated weighted harmonic average trailing 12 months P/E ratio (only companies with profit) was 8.94x, the estimated weighted harmonic average P/B ratio was 1.28x, and the estimated weighted average portfolio dividend yield was 5.06%.

I hope you have enjoyed reading this newsletter. If you would like any further information, please get in touch with me or my colleagues at info@asiafrontiercapital.com

With kind regards,

Thomas Hugger

CEO & Fund Manager