I’ve done up a free video case study under our Investment Case Studies Series for the Astrea bond series now that Astrea V is on its way.

Q1 hedge fund letters, conference, scoops etc

You can watch it here:

Astrea Bonds Investment Case Study

The essential structure and safeguards are similar to that of Astrea IV and its helpful to review what’s happened in so far.

In this video case study, I help breakdown:

- What private equity bonds are

- Discussion on private equity funds

- How fund vintages are like wine and why they matter

- What the J-Curve is and why it is so important

- What are structural safeguards and why they play such an important role in protecting your investment

The Astrea bonds are private equity bonds, and were very new and novel when first released. The management team at Azalea has gone to great efforts to educate the public about it.

I am really biased to the Astrea bonds. They have put in a lot of effort to structuring in safeguards to protect retail investors.

I had a chance to meet management at the Astrea IV Investor Day earlier this year and walked away with a positive impression.

You can read more about it here:

Astrea Investor Day 2019 Write-Up & Thoughts

The older Astrea issues have also been upgraded by the ratings agencies.

Allocation is an issue

The only beef I have is that you are likely to run into a situation like last year of it being oversubscribed.

This means that for practical purposes, most retail investors looking to subscribe to the A1 tranche will not get much of an allocation from their intended subscription amounts.

I understand the constraint as there is a finite amount of PE funds that they can place into the structure. You don’t really want a situation whereby they try to raise as much money as possible and disregard asset quality.

There is probably where the fear that people have with CDOs / Lehman Minibonds / Watching The Big Short are arise from.

Suffice to say, there is a real reputational risk involved and I don’t see Azalea heading down the route.

Astrea IV Bonds Are An Option

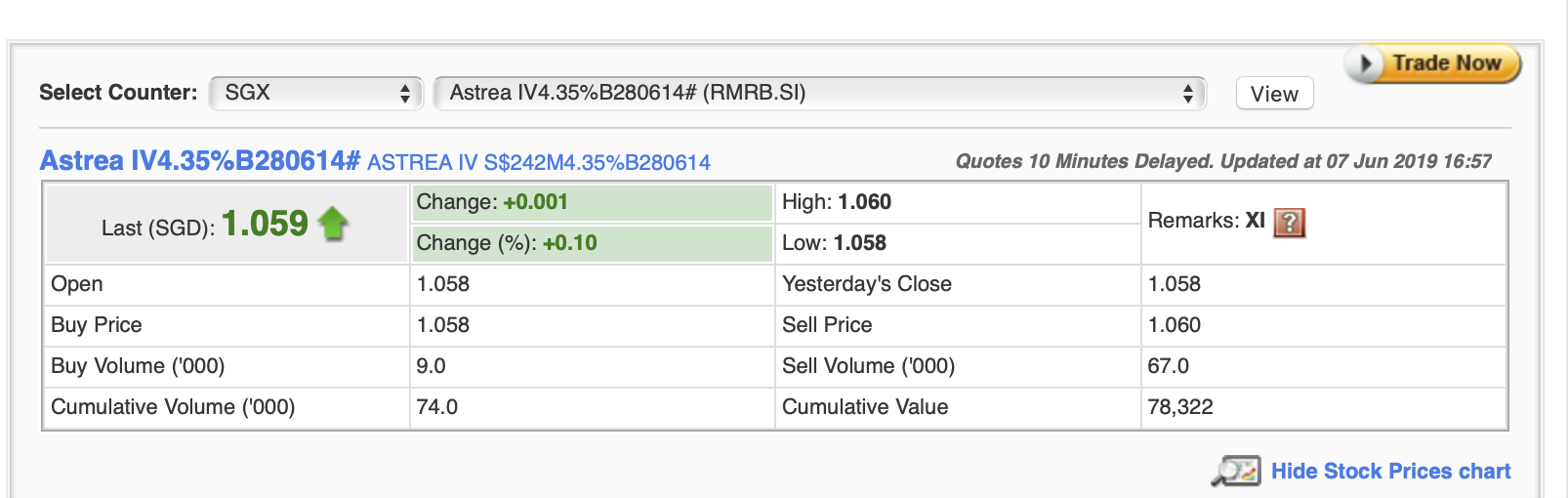

Finally for investors looking for more substantial allocations, there is actually a fairly active market for the previously listed Astrea IV bonds.

You have to pay a premium to par value… but it still yields a generous 4+%.

Furthermore, the bonds only have about 4 years left to maturity and the average fund vintages are also older compared to the upcoming Astrea V bonds which are a plus in my book.

PS: We are hosting a webinar on whether the three Singaporean banks are undervalued today:

Are UOB, OCBC and DBS undervalued now?

Wednesday, 12th June AT 8:30PM

I will be covering several topics such as:

1. HOW DO SINGAPORE BANKS MAKE ACTUALLY MAKE MONEY?

I will breakdown the business models of banks and explain the common financial ratios to look at to assess their long term profitability.

This is to help you put their results in context and to understand whether their earning and dividend growth is sustainable over the long run.

2. SUMMARY OF THE FINANCIAL RESULTS FOR FY 2018

I will run investors through the bank’s recent financial results and explain it in the context of what has happened over the last three years.

3. MAJOR FACTORS THAT HAVE AFFECTED BANK VALUATIONS RECENTLY

I will talk about the recent events which have negatively impacted their stock prices and discuss the long term implications of these events on their long term profitability.

4. ARE SINGAPORE BANKS CHEAP? (VALUATION)

I will discuss the valuation ratios that I use to assess when bank stock prices are cheap. I will talk about current valuations and whether I think they offer compelling value at current prices.

Article by Jun Hao, The Asia Report