Barac Capital Management commentary for the third quarter ended September 30, 2019.

Q3 2019 hedge fund letters, conferences and more

Dear All,

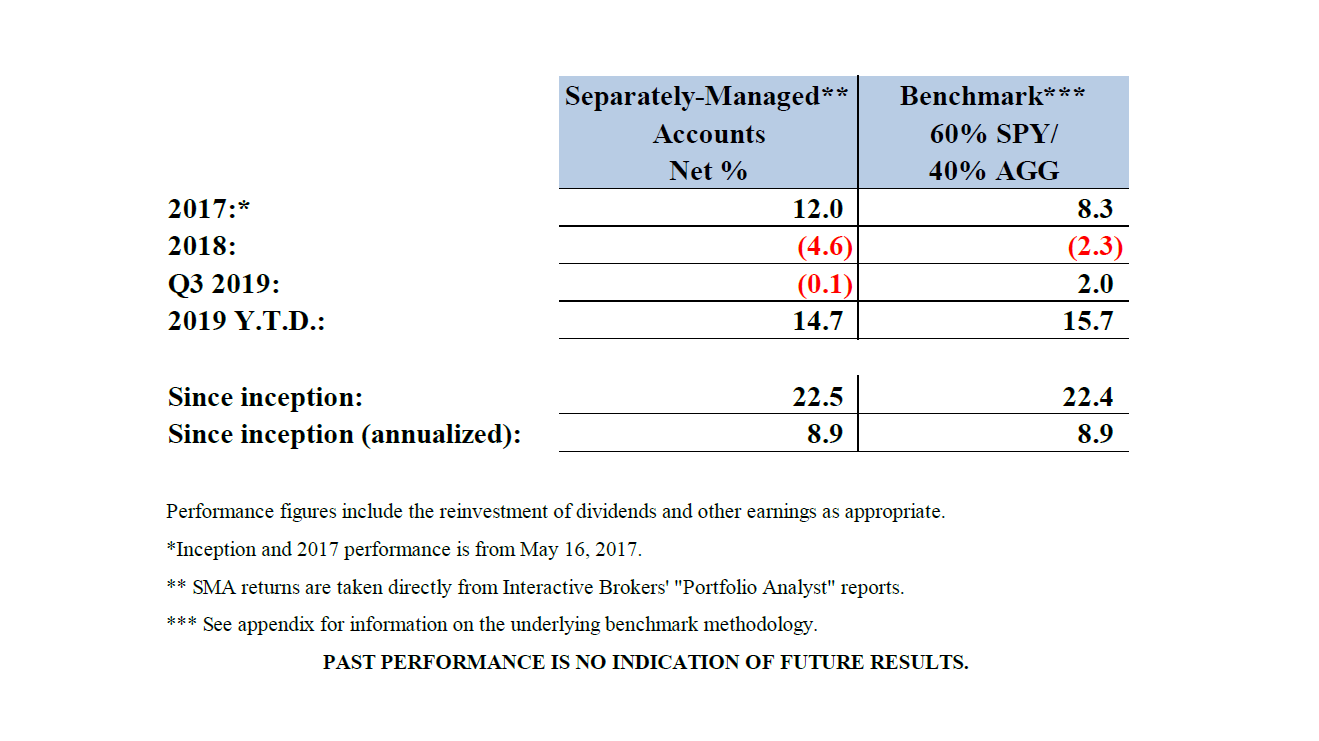

The aggregate performance of Barac Capital Management’s (“BCM”) separately-managed-accounts (“SMAs”)1 for the third-quarter ending September 30, 2019 was -0.1% relative to a 2.0% return for BCM’s benchmark.

Individual account performance may vary, depending on timing factors, fee levels, and customized asset allocations. Please check your brokerage statements for the actual returns of your individual accounts.

Second Quarter Performance

Second quarter returns amounted to -0.1% on a net basis (2.0% for the benchmark), bringing year-to-date returns to 14.7%. Cumulative returns since inception on May 16, 2017 amounted to 22.5% (8.9% annualized).

As always, it is important to re-state that returns were generated without leverage (either direct or effective leverage, through options), without taking highly concentrated positions, and while conservatively holding substantial cash and/or Treasury bond positions.

Performance Commentary

I’m not going to comment on individual positions in this letter, except to say that core positions remain similar to those of the prior period and I feel good about the forward prospect of the securities held. I’ll write more on individual positions in future letters; however, this letter will mainly focus on a key factor that has impacted longterm performance. That being, the recent decision to be cautious and not be more fully-invested in stocks.

Since inception, SMAs have performed broadly in-line their multi-asset benchmark while capturing 76% of the S&P 500 stock index’s total returns — with much less equity market exposure (given an average weighting in stocks of only 54%2). More specifically, net returns (after fees and expenses) amounted to 22.5% (8.9% annualized) versus 22.4% (8.9%) for the benchmark and 29.5% (11.5%) for the S&P 500 index (including dividends).

I believe this is a respectable result, given the circumstances. That said, I’m obviously not satisfied with broadly in-line performance (versus the benchmark) and I expect this to improve as we move forward and eventually go through a full-market cycle.

I aim to achieve this not just through the selection of individual securities that I expect to outperform. I also expect to have less downside (relative to the benchmark) during the next bear market and more upside on the subsequent return back up (after re-allocating more heavily into stocks if and when valuations and risk/reward dynamics substantially improve). Having dry powder available, for future market opportunities, is one of the advantages of not being fully-invested in stocks.

While there’s no guarantee of future results (and, obviously, all investment managers aim for improved relative performance), that’s my general expectation. I know this sounds like a plan to “time the market” but it’s really not. Rather, it’s about modifying asset class concentrations to reflect relative risks/reward dynamics, as I will discuss.

The stock market is near all-time highs and those who have been fully-invested (in stocks) are reaping the benefits and being lauded for their foresight into the markets. Even better if they took (what I would consider to be) irresponsibly large concentrations in volatile individual stocks that rallied. Conversely, those that have been more cautious are often mocked as “perma-bears” or failed “market-timers”.

As someone who has recently been cautious (averaging about 46%3 in cash and Treasury bills since the inception of these SMAs in 2017), I’m going to defend the more cautious position. Spoiler alert: this is going to be one of those “a sub-optimal outcome doesn’t mean a sub-optimal decision’’ arguments that can be made to justify just about any investment decision. In this case, however, I do believe that the argument is strong and the reasons for being cautious are justified. You can judge for yourself.

While I don’t believe in timing the market (and I think that short-term market movements are completely unpredictable) I believe that being underweight stocks during a period when there is strong evidence that market risks are elevated can be prudent. I believe that this can be the case even when the benefit of hindsight later proves one “wrong” (i.e. when a sell-off doesn’t subsequently occur).

I like to use the analogy of insurance. Just because your house didn’t burn down, doesn’t mean that it wasn’t prudent to have homeowner’s insurance for fire damage.

That said, there’s no tangible monetary benefit that can be seen for taking out that insurance in a year when no fire occurred. The same can be said for taking a cautious investment stance during a period when stocks continue to rise higher (despite elevated risks and worsened risk/reward dynamics).

Of course, people are generally more accepting of insurance costs versus stock market opportunity costs. While wealth managers often get punished for taking cautious positions (in years when stocks go up) you don’t often see life insurance customers grumbling about paying their premiums in years when they “didn’t even die”.

To be fair, it can also be completely justified to criticize wealth mangers for being too cautious and there are “perma-bears” that do consistently miss out on returns for being too cautious. In that regard, there’s a lot of truth in Peter Lynch’s quote that “far more money has been lost by investors anticipating market corrections or trying to anticipate corrections than has been lost in the corrections themselves”.

Stocks should do better than bonds (and obviously should do much better than cash) over the long-term, so I believe that being overweight stocks should be a normal weighting and being underweight should be the exception (and it has been for me). It just so happens that shortly prior to the inception of these SMAs (in May of 2017), we entered into a period when I believe that market risks became somewhat elevated.

While I have generally been underweight stocks since the SMA’s inception, I am willing and typically more prone to be overweight. In fact, the fund that I managed from 2011 to 2018 (before I transitioned exclusively to separately-managed-accounts) comfortably outperformed its benchmark from inception through dissolution, largely because it was overweight stocks throughout the first five years of its six-year existence.

For example, in mid-2013 stocks comprised about 83% of BCM’s assets (versus about 55% today). Around that time and up until late in 2016, I consistently made the case for being overweight stocks.

At this point in time, however, I still believe that caution is warranted for reasons that I have given before and will repeat again. Not only are price-to-earnings levels high (with a forward price-to-earning’s multiple of almost 19×4) by historical standards, but the earnings part of that equation continues to reflect very favorable dynamics that are cyclical and/or otherwise subject to potential adverse change: low interest rates (and low credit spreads), the positive wealth effect of 10 years of rising stock prices and home values, high levels of deficit spending, and record low unemployment levels.

Furthermore, current valuations still appear to incorporate too little with respect to geo-political risks at a time when there is much political change and uncertainty. It also warrants keeping in mind that if/when the business cycle does turn (and assets prices fall), a resulting “reverse wealth effect” could exacerbate the impact of a cyclical downturn. Finally, it’s worth noting that low interest rates and high deficits reduce the weapons that the government has to mitigate any substantial market downturn.

For all of these reasons, SMA accounts remain more defensively positioned than the benchmark (which, itself, reflects a conservative asset allocation). This is reflected in the fact that 45% of the SMA assets are currently either in cash or U.S. Treasuries with maturities less than 5 years. Furthermore, I continue to believe that the equity holdings include idiosyncratic value opportunities (for specific stocks) that are superior to those of the equity markets as a whole.

Accounts also remain well diversified, with no single-stock position accounting for more than 5.5% of BCM’s assets-under-management. As always, risk management and capital preservation remain paramount to the investment strategy.

Thank you to everyone for your interest and support and please let me know if there are any questions you may have that I haven’t answered.

Sincerely,

Ted Barac

Managing Member of Barac Capital Management, LLC

Appendix: About the Benchmark

As multi-asset accounts whose objective is to seek investment opportunities across different asset classes (e.g. stocks, bonds, etc.), the benchmark used for the SMAs is a mix of 60% attributed to an S&P 500 index fund (SPY) including dividends paid, and 40% attributed to the Barclays aggregate bond index fund (AGG). The S&P 500 is a commonly used index of 500 U.S. large capitalization stocks while the Barclays aggregate index is a commonly used index of U.S. high-grade bonds.

The reason for using this specific benchmark is because it is comprised of two very commonly followed indexes for the two major investment classes (stocks and bonds) in the 60%/40% ratio mix, which has been a common allocation ratio recommended for long-term investors. In addition, both of these indexes can be easily purchased through low-fee and highly-liquid index funds, providing an easy alternative for investors. Long-term outperformance versus these indexes is necessary to justify an investment with Barac Capital and, therefore, this is the yardstick to which accounts will be compared.

To be clear, the benchmark is chosen only to provide an easy and simplistic comparison to how one’s investments might have performed if invested in low-fee index funds allocated in the commonly prescribed mix of 60%/40% (equities/bonds). Barac Capital does not endorse or make any attempt to follow such an allocation and in periods when I view equities as substantially over-valued, the equity allocation may be much less than 60% and vice-versa. In addition, accounts will also hold other asset classes, outside the scope of the benchmark, which may include cash, small-cap. equities, foreign equities, and high-yield bonds, among others. Overall, the investment strategy is about finding the best value across different asset classes and geographies while sizing positions to best optimize risk/reward.

As noted, the SMA benchmark methodology is linked to low-fee index funds that track the respective indexes (as supposed to using the actual indexes themselves). I believe that using passive-index funds (instead of the actual indexes) for the benchmark more accurately reflects the actual costs of investing in a passive strategy (where there are some fees, albeit very low: 10 bps/year for SPY and 5bps for AGG).

Fund Dissolution in October of 2018

In April of 2017, Barac Capital began offering separately-managed-accounts (S.M.A.) and the offering has been very successful (with assets in these accounts growing to substantially exceed those of the Barac Value Fund, L.P.; the “Fund” or “Partnership”). I started offering the S.M.A.s in order to address some of the inherent disadvantages of a hedge fund structure. While I continue to believe that the Fund’s terms were very attractive (within the confines of a hedge fund structure), there were still a number of inherent drawbacks for many investors, including:

- Limited control (e.g. ownership of a percentage of the Fund rather than complete ownership/control of your own brokerage account);

- A lack of individual customization;

- A regulatory requirement to be an “accredited investor”;

- Contributions required in cash (potentially requiring other investment liquidations and a crystallization of capital gains);

- Limited liquidity (monthly only); and

- Partnership “K1s” for tax preparation.

Because the S.M.A. offering addressed these issues and is inherently advantageous (for investors), relative to an investment partnership, I saw little on-going incentive for an investor to choose the Fund over this alternative relationship. As such, on October 16th 2018 the dissolution of the Fund was completed and the assets of the Partnership were distributed into the S.M.A.s of the limited partners.

Importantly, the Fund was dissolved in a tax efficient manner that didn’t crystallize the unrealized gains of the Partnership (via a dissolution in-kind). The time and administrative tasks required to complete this in-kind distribution was substantial (relative to what would have been required for a liquidation), but the relative tax benefits it provided to the limited partners was well worth the effort.

The aggregate net returns (after the deduction of fees and expenses) for the Fund since inception (on July 14, 2011) to the last business day prior to dissolution (October 15, 2018) amounted to 90% on a net basis (after management fees), compared to 84% for the Partnership’s benchmark5.