“Davidson” submits:

[REITs]

Q2 hedge fund letters, conference, scoops etc

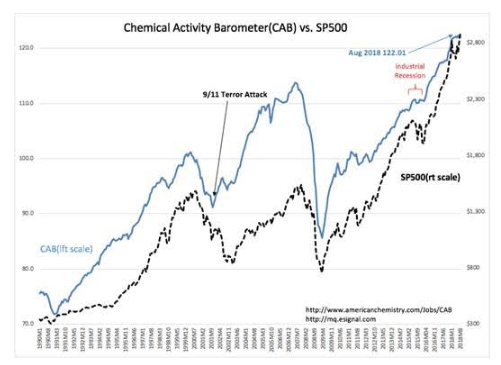

Markets reach new highs as many feared issues did not come to pass. While many fret that this market is ‘too long in the tooth’ or tariff policies or fear of No. Korea or Iran or China or some other issue unseen will result in economic correction, we are not seeing this in the data. The Chemical Activity Barometer(CAB), one of several reliable economic indicators, just reported 122.01. Somewhat slower than the torrid pace seen May-2016-May 2018, but still higher which bodes well for US economic expansion the next 12mos-18mos. An excerpt from the Aug 21st press release:

“Nearly all manufactured goods are produced using chemistry in some form or another. Thus, manufacturing activity is an important indicator for chemical production. On a three-month-moving average basis, manufacturing activity edged higher by 0.4 percent in July, following a 0.1 percent gain in June. Output expanded in several chemistry-intensive manufacturing industries, including aerospace; construction supplies; machinery; fabricated metal products; computers & electronics; semiconductors; petroleum refining; plastic products; tires; structural panels; and textile mill products.”

Note, the CAB shifted higher even as the SP500 corrected when investors became spooked with US tariff policy initiatives. In the battle of market psychology vs economic activity, it has always been economic activity which wins out and drives market psychology higher during economic expansion.

The first outcome of the US tariff policy initiatives resulted in a ‘deal’ with Mexico. The administration strategy is much like playing Dominos. Get one domino to fall and the rest will follow. Even though the Mexico agreement is only part of the renegotiation of NAFTA (Canada is required for full agreement) what has been accomplished is already much further than many thought possible. The market fear we saw in recent US$ strength appears to be reversing as last week’s headlines turned favorable. As a proxy for the US$, DXY peaked August 14th at 97 and today has fallen to 94.5. This is almost a 3% decline. Is this it for US$? One doesn’t know, but the Mexico agreement could be the beginning of the US$ return to its long-term trend if Canada falls in line and then followed by Europe.We have seen several US policy shifts which have had positive economic impacts. This is why so many predictions of even the past 12mos are off the mark. As policy initiatives produce impacts, one can only observe the outcome and adjust one’s investment stance accordingly. Thus far, this is very favorable for equity investors.

https://www.marketwatch.com/investing/index/dxy

The Investment Thesis August 28, 2018:The lesson, which seems to have to be relearned frequently, is that market psychology drives prices and is itself driven by economic headlines. Markets follow, they do not lead. Policy initiatives have had a hand the last 18mos in accelerating economic expansion thru regulation and tax reduction. Tariff and economic sanction initiatives appear to be additional stimuli. Should the US$ decline to its long-term trend, estimated at ~30% below today’s level, the US economic expansion could continue for several years.

So far, so good!