Right now, anything Russian is toxic in the investment world.

But sometimes the vodka goes down the drain with the mineral water… and I found a stock that I think fits the bill.

The problem of Russia

Russian shares have for years traded at a much lower valuation than other emerging markets. I started working in the Russian stock market in the mid 1990s – I lived in Russia for nine years in part as a stock market analyst for a handful of investment banks – and for most of that time, Russian assets have been cheap.

The graph below shows the cyclically adjusted price-to-earnings ratio (CAPE) for a range of markets. The CAPE uses the average for ten years of earnings, and adjusts them for inflation. This smoothens the cyclicality of a single year P/E. It’s more difficult to calculate, but it’s a more complete valuation measure than the normal P/E ratio. According to the CAPE, Russia is the world’s cheapest stock market by far, with a CAPE of just 6.5, compared, for example, to Hong Kong’s 18.1 or Japan’s 27.7.

Why does Russia trade at such a big discount to other markets?

For starters, emerging market stocks are generally considered more risky… so they often trade at a valuation discount to developed markets.

Russia is even a lot cheaper than other emerging markets, though, in part because of the perception (and reality) that political risk in Russia is higher than in many other emerging markets. The country has a reputation for instability.

I was managing a hedge fund in Moscow during the summer of 2008 when Russia invaded neighbour, and fellow former Soviet republic, Georgia. The Russian stock market crashed. But that was soon overshadowed by the full force of the global economic crisis, during which the Russian economy contracted by more than any other big global economy… and its stock market similarly underperformed nearly every other country.

Morgan Stanley: Bear Scenario Is 30% Revenue Decline For Asset Managers By 2020

More recently, Russia’s invasion and annexation of Crimea, a Ukrainian territory, in 2014, started a conflict that is still going on today. Russian president Vladimir Putin has an image as a power-hungry dictator who will do anything to stay in power. And last month’s so-called presidential elections, which saw the re-election of Putin to a fourth term, will do nothing to reduce the perception of political risk in Russia.

Overall… it’s enough to make you think that the country’s market is a value trap.

The latest chapter

And in early April, we were given another reason for Russian assets to remain cheap.

On April 6, the U.S. Treasury Department announced new sanctions targeting seven Russian oligarchs, a dozen of the companies they own or control, 17 senior Russian government officials and a state-owned weapons trading company and its banking subsidiary.

Senior U.S. administration officials said the sanctions are a broader measure aimed at the “totality of the Russian government’s ongoing and increasingly malign activities in the world.”

The short-term impetus for that measure was the spy universe… last month, a former Russian spy and his daughter were poisoned on British soil. UK Prime Minister Theresa May, and many others, think that the Russian state was culpable. So in response, the UK announced the expulsion of 23 Russian diplomats identified as “undeclared intelligence officers”, the suspension of all planned high-level bilateral contacts between the UK and Russia, and plans to consider new laws to increase defenses against “hostile state activity”, and a number of other measures.

EM Recovery Is Grinding To A Halt: Capital Econ

In response to the sanctions, Russian stocks crashed last week, by 8.4 percent. Sanctioned aluminum producer Rusal, which is controlled by billionaire Oleg Deripaska, plunged more than 50 percent. The ruble also fell to its lowest level against the dollar since 2016.

What happened was that investors indiscriminately sold anything related to Russia. No one wanted to be left holding the next Russian company whose CEO the U.S. government decides is close to Putin. So it’s easier to sell first.

Russia’s Google

Another one of the stocks that was hit hard is Russia’s answer to Google. It’s a US$11 billion market cap company called Yandex (Nasdaq; ticker: YNDX). It is the world’s fourth-largest Internet search provider. And it has around a 55 percent market share of the Russian internet search market (in part because the Russian government has made it very difficult for Google to operate in Russia). For comparison, Google has a 42 percent market share in Russia.

Emerging Market Debt Funds On Track For A Record Year

Yandex doesn’t just operate in the search engine space. The company has an email service and a cloud storage product. It has also launched a voice-enabled digital assistant called Alice. Yandex also has a ride-hailing and food delivery business. And in March, it formed a joint venture with Uber (valued at more than US$3.8 billion) to combine their ride-hailing and food delivery businesses in Russia.

Yandex has also developed a self-driving car (which it’s already testing in Russia). It also recently signed a deal with Russian state-run bank Sberbank to create a joint e-commerce venture. And it has introduced a new feature for online shopping in around 76,000 global stores and services that give customers the option of paying for purchases in installments.

So Yandex is a rapidly growing company that’s expanding far beyond search. Revenues were up 24 percent in 2017, and adjusted net income grew 9 percent.

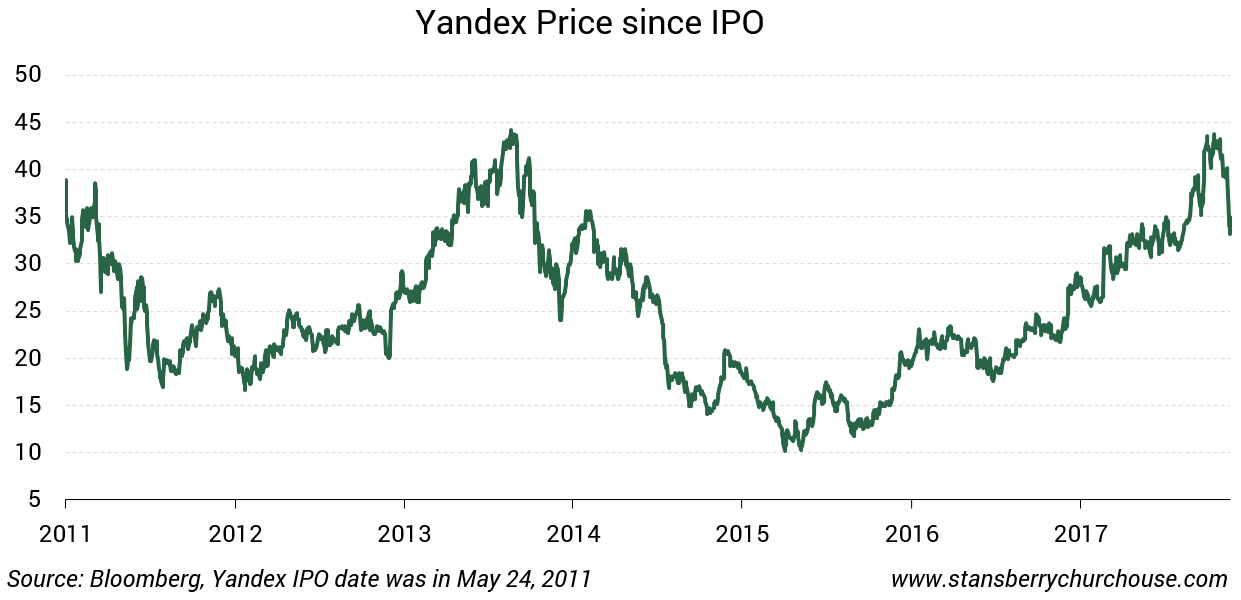

However, the stock’s performance leaves a lot to be desired. The shares are up 150 percent since early 2016. But the stock is at about the same price level today as it was for its IPO in 2011 (although revenues are up 160 percent in U.S. dollar terms since then). And after the recent selloff, the shares are down 25 percent over the past month. On April 9, in response to U.S. sanctions, it fell 12 percent.

Thrown out with the bathwater

But here’s the thing. Yandex, or its CEO, Arkady Volozh, is highly unlikely to be targeted by the U.S. government, or anyone else. He’s not really on the radar. He’s not a chum of Putin’s, and (unlike the heads of businesses that may be included on a second wave of U.S. sanctions) he didn’t make his money by knowing the right people at the right time in the Russian government.

Yandex has to colour between the lines set by the Kremlin – as does any business in Russia, China and other economies where the government plays a big role in the economy. But he’s the opposite of a Russian oligarch who’s going to fall under U.S. sanctions.

Stress in S&P500 vol appears extreme: BAML

At least as importantly, American problems with Russia haven’t usually touched on technology. Russia is a commodities-driven economy (despite years of rhetoric about diversifying its economy)… and its search engine isn’t really a concern to the U.S.

I’ve followed and liked Yandex for a long time (I recommended it to the subscribers of a premium investment service I wrote several years ago). If relations with the west further sour, or if hot words turn to hot war in Syria, Yandex shares are going to suffer along with other Russian shares. But if not, Yandex is a great example of a stock that’s being unfairly tarred with the rest of a difficult market… and likely to recover sooner rather than later.