Skenderbeg Alternative Investments put into perspectives for the month of December 2018.

“I love it when people always say I’m always ‘too early’. You can be late to a bull market—it’s an escalator on the way up. You can’t be late to a bear market—because it’s an elevator going straight down.” – David Rosenberg

Q3 hedge fund letters, conference, scoops etc

Hedge Funds

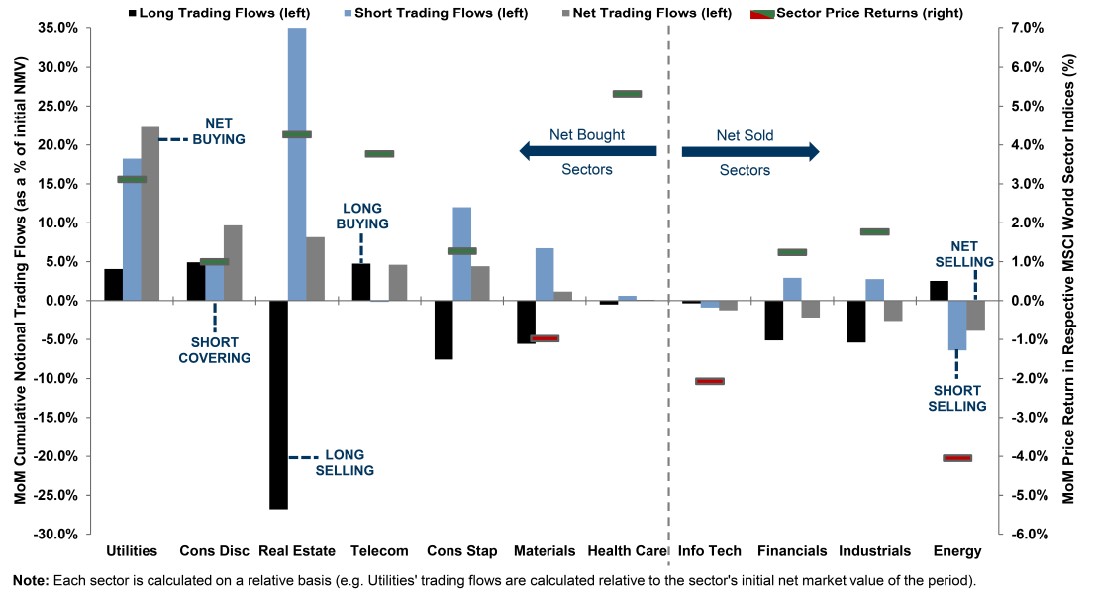

Hedge fund positioning and trading flows

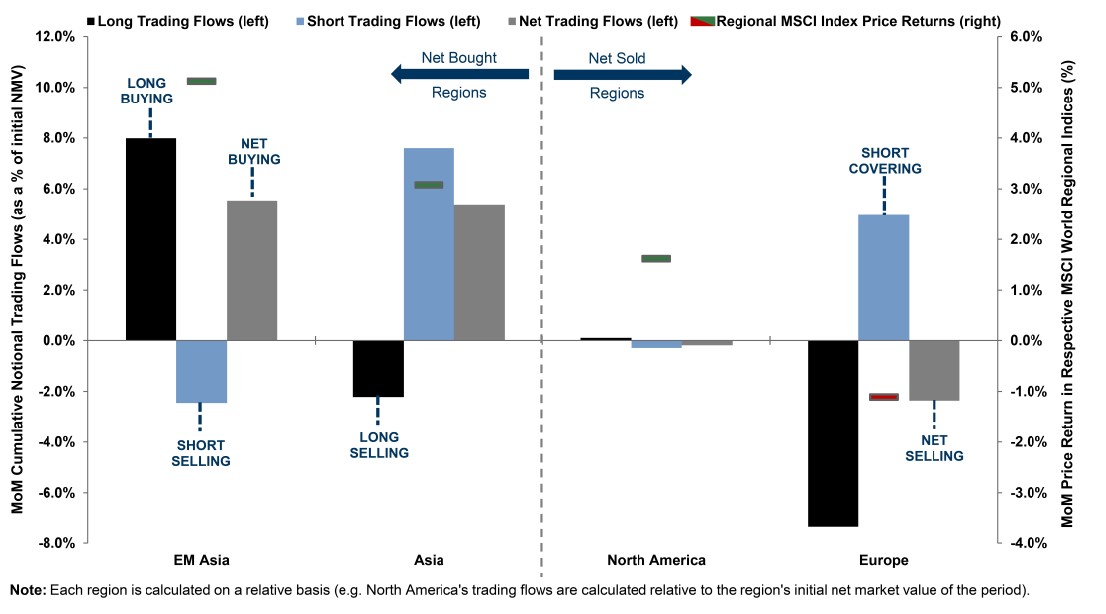

November hedge fund trading flows by region (vs. MSCI World regional price returns)

November hedge fund trading flows by region (vs. MSCI World regional price returns)

Compensation soars for hedge fund managers

The wallets of hedge fund managers are looking fatter this year. Total compensation for hedge fund portfolio managers is expected to climb 40 percent, to $1.4 million, in 2018, according to Institutional Investor’s second annual All-American Buy-Side Compensation Survey. The hedgies on average reported a 25 percent jump in base pay — to $346,164 — and more than $1 million in variable compensation.

Portfolio managers at hedge funds with more than $5 billion in assets are feeling even more flush, as they are expected to earn $2.8 million in total compensation. The big gains are due in part to bonuses for 2017 performance — when hedge funds returned 8.6 percent — being paid in 2018.

Institutional Investor noted that hedgies were “broadly optimistic” about their future paychecks, even amid fears of an economic slowdown.

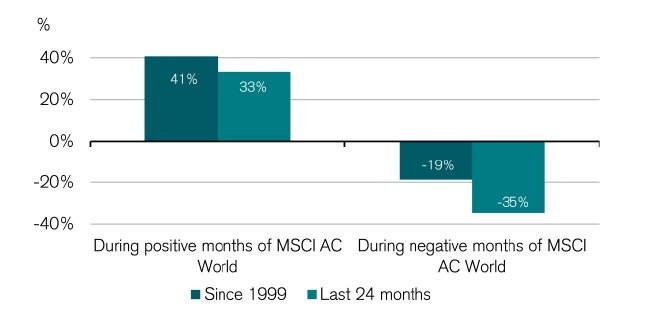

Upside/downside capture ratios (as per cent of MSCI AC World)

Long-term economic consequences of hedge fund activist interventions

University of Washington – Michael G. Foster School of Business

Stanford University – Graduate School of Business

University of Chicago Booth School of Business

Abstract: We examine the long-term effects of interventions by activist hedge funds. Prior papers document positive equal-weighted long-term returns and operating performance improvements following activist interventions, and typically conclude that activism is beneficial. We extend prior literature in two ways. First, we find that equal-weighted long-term returns are driven by the smallest 20% of firms with an aver-age market value of $22 million. The larger 80% of firms experience insignificant negative long-term returns. On a value-weighted basis, which likely best gauges effects on shareholder wealth and the economy, we find that pre- to post-activism long-term returns are insignifi-cantly different from zero. For operating performance, we find that prior results are a manifestation of abnormal trends in pre-activism per-formance. Using an appropriately matched sample, we find no evidence of abnormal post-activism performance improvements. Overall, our results do not strongly support the hypothesis that activist interventions drive long-term benefits for the typical shareholder, nor do we find evidence of shareholder harm.

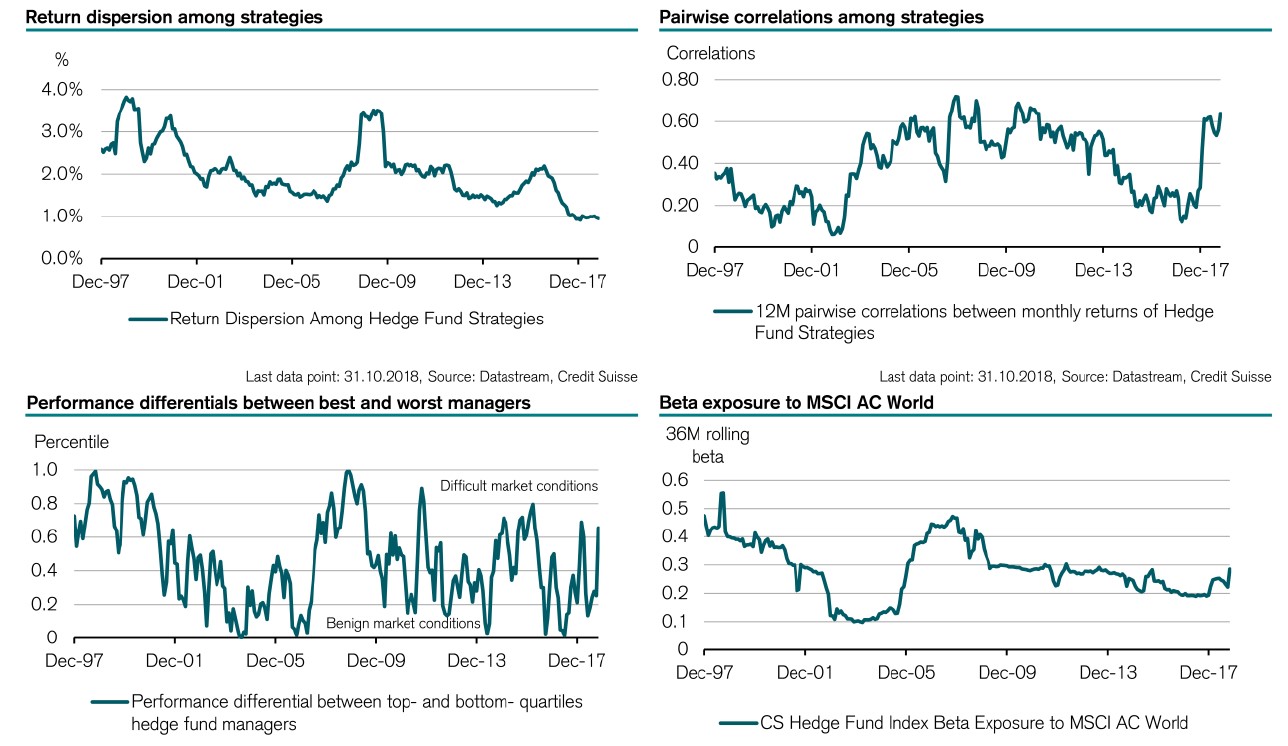

Hedge fund barometer inputs: Breakdown of systemic risks

See the full PDF below.