“A generational opportunity hidden in plain sight. Its status of loneliness and ‘vox clamantis in deserto’ (a voice crying out in the wilderness) makes for potential outsized returns.” – Francesco Filia

Q3 hedge fund letters, conference, scoops etc

Plan 1: Buy-hold-rebalance. Buy lowest fee index funds you can find. In 40% to 60% corrections, close eyes, don’t panic, hold on, stick to plan. (Best for 20 and 30-year-olds.)

Plan 2: Seek growth while maintaining a level of protection against 40% to 60% corrections. Open eyes, don’t panic, become greedy when others are fearful, fearful when others are greedy, stick to plan. (Best for 50-year-olds and older.)

I’m a “Plan 2” guy. Maybe it’s due to one too many valuable knocks to the head. Back in 1984, no one I ever came across was a Plan 1 guy. My mentor and good friend, John Ray, handed me a book titled, Reminiscences of a Stock Operator by Edwin Lefevre. First published in 1923, Reminiscences is a fictionalized account of the life of the securities trader, Jesse Livermore. It’s the single best investment book I have ever read. Perhaps because the 1966 to 1982 bear market kicked everyone in the pants. Perhaps it was those client phone calls on October 19, 1987. Greedy when others were fearful? My firm was not prepared. I was not prepared. My clients were not prepared.

Crystalized in my mind is Dr. G. There were no cell phones back then. My hotel phone rang loud at 3:00 am Maui time. My assistant and a panicked Dr. G. were on the line. He had high yielding tax-free bonds that skyrocketed higher on that crash day. Why was he losing his mind, I wondered? He just was…

THE CRITICAL TRANSFORMATION HYPOTHESIS

Years of monumental Quantitative Easing / Negative Interest Rates monetary policy affected the behavioral patterns of investors and changed the structure itself of the market, in what accounts as self-amplifying positive feedbacks. The structure of the market moved into a low-diversity trap, where concentration risks of various nature intersect and compound: approx. 90% of daily equity flows in the US is today passive or quasi-passive, approx. 90% of investment strategies are doing the same thing in being either trend-linked or volatility-linked, a massive concentration in managers sees the first 3 asset managers globally controlling a mind-blowing USD 15 trillion (more than 20 times the entire market cap of several G20 countries), approx. 80% of index performance in 2018 is due to 3 stocks only, a handful of tech stocks – so-called ‘market darlings’ – are disseminated across the vast majority of passive and active investment instruments. The morphing structure of the market, under the unequivocal push of QE/ZIRP new-age ideologism, is the driver of a simultaneous overvaluation for Bonds and Equities (Twin Bubbles) which has no match in modern financial history, so measured against most valuation metrics ever deemed reputable; a condition which further compounds potential systemic damages. The market has lost its key function of price-discovery, its ability to learn and evolve, its inherent buffers and redundancy mechanisms: in a word, the market lost its ‘resilience’. It is, therefore, prone to the dynamics of criticality, as described by Complexity Science in copious details. This is the under-explored, unintended consequence of extreme experimental monetary policymaking. A far-from-equilibrium status for markets is reached, a so-called unstable equilibrium, where System Resilience weakens and Market Fragility approaches Critical Tipping Points. A small disturbance is then able to provoke a large adjustment, pushing into another basin of attraction altogether, where a whole new equilibrium is found. In market parlance, more prosaically, a market crash is incubating – and has been so for a while. While it is impossible to determine the precise threshold for such critical transitioning within a stochastic world, it is very possible to say that we are already in such phase transition zone, where markets got inherently fragile, poised at criticality for small disturbances, and where it is increasingly probable to see severe regime shifts. Fragile markets now sit on the edge of chaos. This is the magic zone, theorized by complexity scientists, where rare events become typical.

Source: Francesco Filia, Fasanara Capital

In 2006, 2007 and 2008, I wrote about subprime. It began with a 2006 call from one of the smartest investors I know, my friend, Mark Finn. “Steve, check your portfolio. Do any of the managers have subprime, MBSs, CDO exposure?” Mark, I asked, “What are you seeing?”

CDOs – Collateralized Debt Obligations: a Wall Street-invented product. A collection of pooled assets (like subprime mortgages) neatly delivered in various tranches you could buy depending on your risk appetite. Squash together a bunch of no-doc, no-down payment high credit risk mortgages, send it to Moody’s for a AAA stamp of approval and sell those yield hungry unsuspecting investors the high-rated, high-yielding debt they are looking for.

“… ‘vox clamantis in deserto’ (a voice crying out in the wilderness)”

Mark and his team get pitched on just about everything. When you’re deep inside the capital markets machine and regularly speak with smart people, you see things. One of those pitches was from a manager betting big time against those garbage mortgage pools. Then another made the same pitch. Lights on. Alan Greenspan later said nobody saw the crisis coming. Right.

In 2005, eccentric hedge fund manager, Michael Burry, discovered that the United States housing market was based upon high-risk subprime loans and, therefore, was extremely unstable. Anticipating the market’s collapse in Q2 2007, as interest rates would rise from adjustable-rate mortgages, he proposes to create a credit default swap market, allowing him to bet against market-based mortgage-backed securities, for profit.

His long-term bet, exceeding $1 billion, is accepted by major investment and commercial banks, but as it requires paying substantial monthly premiums, it sparks his clients’ vocal unhappiness, believing he is “wasting” capital. Many demand that he reverse course and sell, but Burry refuses. Under pressure, he eventually restricts withdrawals, angering investors. Eventually, the market collapses and his fund’s value increases by 489% with an overall profit of over $2.69 billion. (Source: The Big Short, Wikipedia.)

Michael Burry was “a voice crying in the wilderness.” Mark Finn was a voice. Because of Mark, John Mauldin was a voice and I was a voice. I’m pretty sure Mark invested in those hedge funds and didn’t miss. As a fiduciary to his clients, he holds his cards close to the vest. I saw it and missed but, boy, did the crash create a fantastic buying opportunity (success was limiting downside loss and getting to the opportunity with available cash).

Did you catch that part in the Michael Burry story where he fought off client unhappiness? As withdrawals from his hedge fund mounted, he restricted withdrawals. Michael was early, Mark was early, Mauldin was early and I and other voices were early.

I believe we are in the early innings of another economic and capital markets storm approaching. Fed driven. I think I’m early. I believe this one will be bigger than the last. Lights on.

Plan 1 guys say I’m too bearish. Makes sense viewed through their lens as my message is not so good for the stock and bond market buy-hold-rebalance game plan. No sweat if you’re in your 20s. A disaster if you are nearing or in retirement.

Plan 2 guys are nodding their heads with me. Viewed through this lens, I see an epic buying opportunity approaching. And if you’ve got the chutzpah, a “Big Short” movie part two is coming your way. Instead of us hearing “housing will never crash,” we’ll be hearing there is “no way sovereign debts will ever crash.” Are the asymmetric bets a short Chinese debt, EM dollar-based debt, European sovereign debt or U.S. debt (especially corporate HY debt)? Perhaps all four. Key word: chutzpah!

Go grab that coffee and settle in your favorite chair. Today I am sharing with you my weekly dashboard of indicators. I believe the most important of which are the recession indicators. They are good and I think they can help us better light the path forward. Also today, and over the next coming weeks, I’m going to share some ideas around investment positioning and “big bets” to consider. Please understand this is not in any way a recommendation for you to buy or sell any security. So much depends on your personal situation, your willingness to take risk, your investment time horizon, your portfolio sizing and your patience.

Last request. Please see this as data. No emotion. See it as having a business discussion. I may be wrong, thus the participate-and-protect mindset. My advice is to tilt towards Plan 2: Seek growth while maintaining a level of risk management (i.e., a possible correction). Open eyes, don’t panic, become greedy when others are fearful, fearful when others are greedy, stick to plan. “Vox clamantis in deserto.”

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- Trade Signals Dashboard – Recession Watch Dashboard

- Why This Matters

- Investment Positioning and Big Bets

- Personal Note

Trade Signals Dashboard – Recession Watch Dashboard

I recommend a formal, disciplined analysis process looking at key indicators that have historically had a great track record in identifying global recessions and U.S. recessions. Each week in Trade Signals I post the following dashboard. My goal is to stay balanced and focused on a disciplined process. Full disclosure side note, I do use several of the signals in work with our clients.

First the Trade Signals dashboard, then the Recession Watch Dashboard, then select charts:

Trade Signals Dashboard

(Green is Bullish, Orange is Neutral and Red is Bearish)

Equity Trade Signals:

- Ned Davis Research CMG U.S. Large Cap Long/Flat Index: Buy Signal – 100% U.S. Large Cap Equity Exposure

- Long-term Trend (13/34-Week EMA) on the S&P 500 Index: Buy Signal – Bullish Cyclical Trend Signal for Equities

- Volume Demand (buyers) vs. Volume Supply (sellers): Buy Signal – S/T Bullish for Equities

- Don’t Fight the Tape or the Fed: Indicator Reading = -1 (Neutral to Bearish Signal for Equities)

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral Optimism (S/T Bearish for Equities)

- NDR Daily Trading Sentiment Composite: Extreme Pessimism (S/T Bullish for Equities)

Fixed Income Trade Signals:

- CMG Managed High Yield Bond Program: Sell Signal — Bearish on HY

- CMG Tactical Fixed Income Index: Treasury Bills (cash proxy) and EM Debt via ETFs

- Zweig Bond Model: Sell Signal — Bearish on L/T Bond Market Exposure

Economic Indicators:

- Global Recession Watch Indicator – High Recession Risk

- S. Recession Watch Indicators – Low U.S. Recession Risk (Next 6-9 Months)

- Inflation Watch – Neutral Inflation Pressures

Gold:

- Long-term Indicator — 13-week vs. 34-week exponential moving average: Sell Signal

- Short-term Indicator — Daily Gold Model: Buy Signal

Recession Watch Dashboard

- Global Recession Probability Indicator – High Recession Risk

- The Economy Based on the Stock Market Indicator – Low U.S. Recession Risk

- Recession Probability Based on Employment Trends – Low U.S. Recession Risk

- S. Credit Conditions – Recession Indicator – Low U.S. Recession Risk

Before you dig into the charts, an important note. The signals you see all presented before anyone knew the start and end dates of the recessions. All recessions are shaded. The reason is that recessions are defined as two consecutive quarters of negative growth. We only know that data more than six months after recession was officially deemed to have started. Knowing too late is not good for your equity portfolio. Thus we seek to get in front of recessions. I believe the following indicators can help.

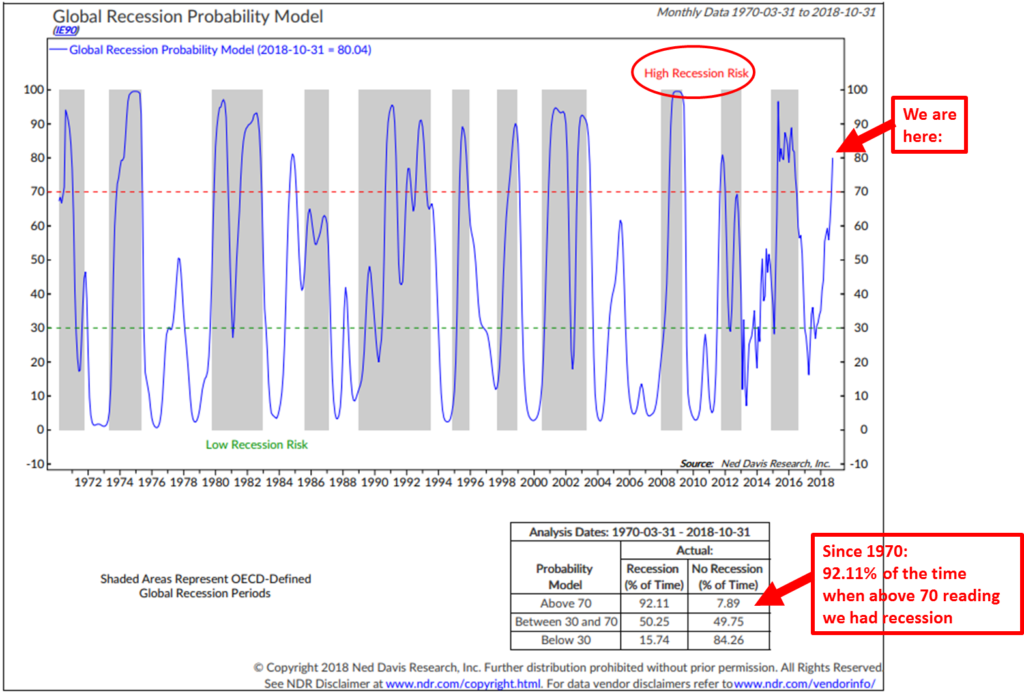

Global Recession Probability – High Recession Risk

In this first chart, note the red arrow at the top right. Readings above 70 have found us in recession 92.11% of the time (1970 to present). Several months ago, the model score stood at 61.3. It has just moved to 80.04. Expect a global recession. It either has begun or will begin shortly. Though no guarantee, as 7.89% of the time since 1970 when the global economic indicators that make up this model were above 70, a recession did not occur.

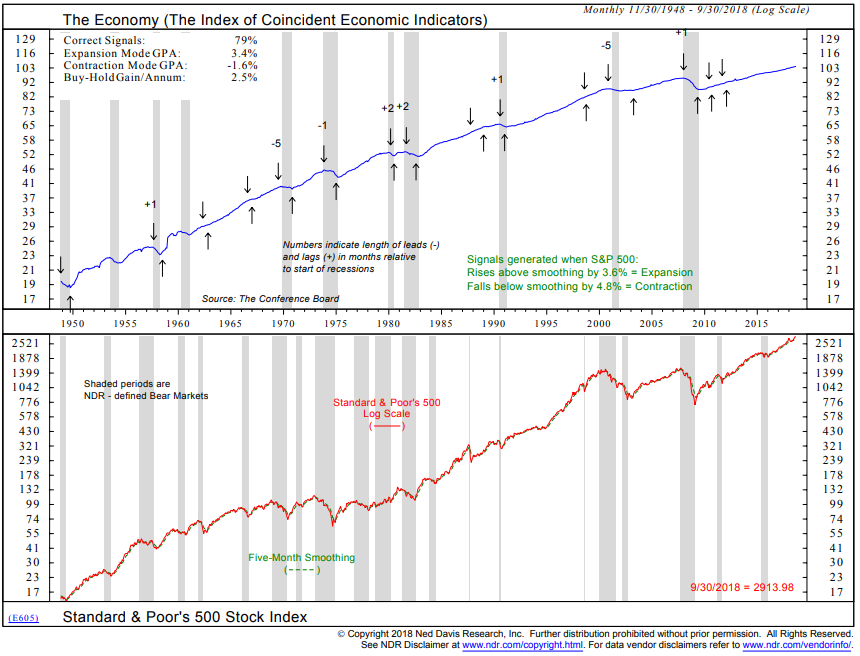

The Economy Based on the Stock Market

As you can see in this next chart, the S&P 500 Index is a good leading indicator for the economy. So when your brother-in-law is telling you to buy stocks because the economy is ripping at the same time stocks are breaking down, know that stocks are the lead dog, not the economy. You likely did not get a call from him in 2002 or 2009 when the economy was in recession. That was the best time to buy stocks.

The next chart looks at the S&P 500 and when it rises above its five-month smoothed moving average line by 3.6%, it signals an economic expansion. When it drops by 4.8% below its five-month smoothed moving average, it signals recession (contraction). This chart is posted monthly after each month-end.

Note the down arrows just prior to or very shortly after recessions started (data 1948 to present). Also note the up arrows.

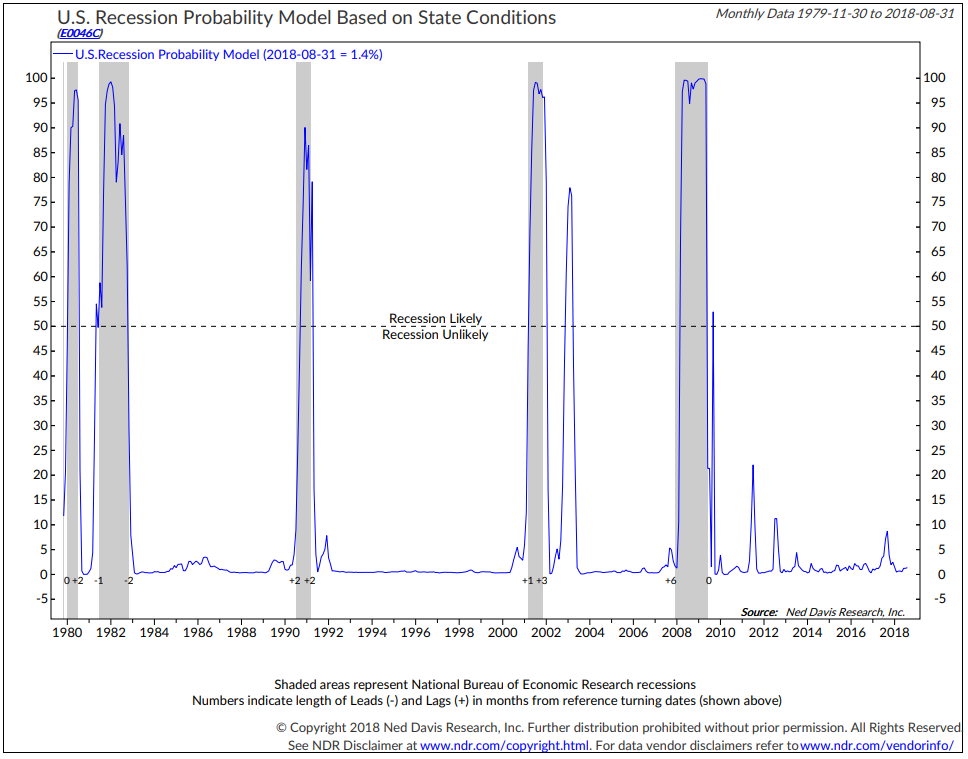

Bottom line: No current sign of U.S. recession.

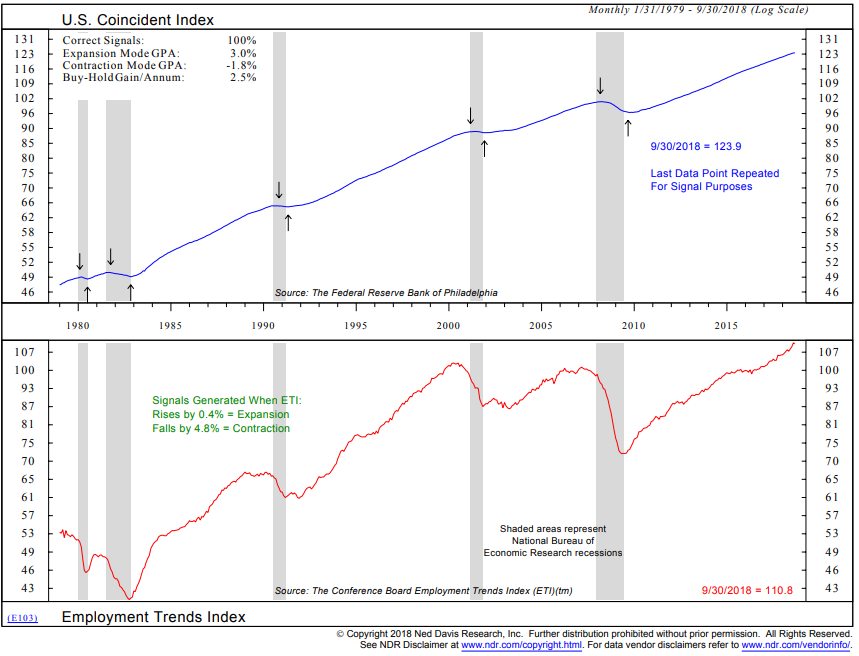

Recession Probability Based on Employment Trends

Again note the up and down arrows.

- Expansion (up arrow) signals are generated when the Employment Trends Index rises by 0.4%

- Recession (or Contraction – down arrows) signals are generated when the ETI falls by 4.8%

- The up arrow signals were very good

- The 1992 recession down signal was a little late

- Overall, 100% correct signals

- Bottom line: No current sign of recession

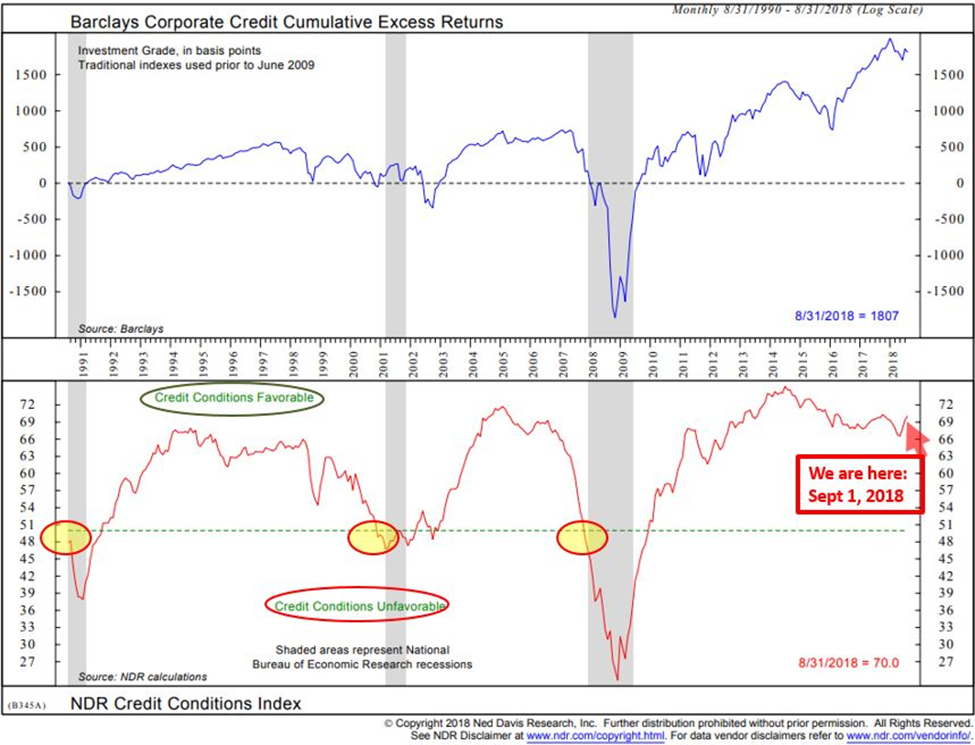

U.S. Credit Conditions – Recession Indicator

- Recession is probable when Credit Conditions drop below the green dotted line (a move from “Favorable” to “Unfavorable” credit conditions)

- Bottom line: Credit conditions remain favorable. No sign of recession in the next six to nine months.

Let’s look at the charts:

U.S. Recession Probability Based on State Conditions

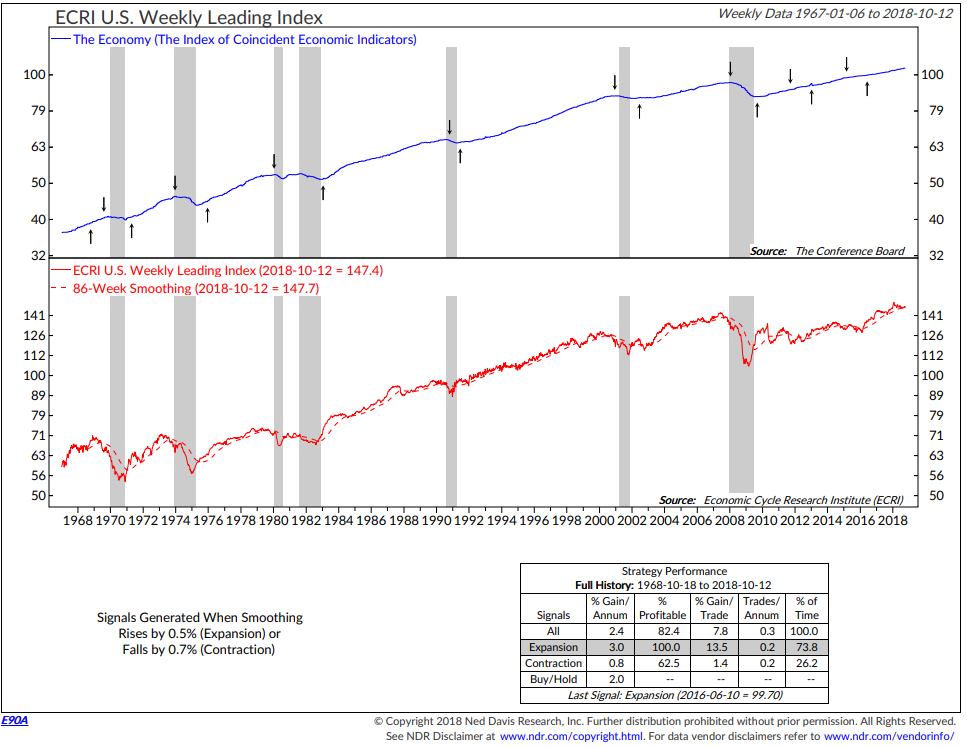

ECRI U.S. Weekly Leading Index

- Note up and down arrows.

- Signals generated when the smoothed moving average line rises by 0.5% (expansion signal) or falls by 0.7% (recession or contraction signal).

- Several false signals.

- Take a look at the solid red index line. Just noting that it has dropped below its smoothed moving average trend line (dotted red line). That is something that has happened just prior to past recessions. Yet you can also see several head fakes since the last recession in 2008/09.

- Bottom line: Currently in an expansion signal… No current sign of recession.

Jeffrey Gundlach was interviewed by Forbes a few days ago. I think he sums up the current potential for U.S. recession well.

Karl Kaufman: Do you think there could be a recessionary swing in the market because of interest rates moving too fast?

Jeffrey Gundlach: There are no signs of that yet. We have developed over a dozen forward-looking recession warning indicators: things like year-over-year leading economic indicators that always fall below zero before the recession comes. Right now they’re at 6.4% year-over-year, miles away from a recessionary signal.

Junk bond spreads are nowhere near widening enough to signal the recession and unemployment rates just hit a new low. Obviously, not recessionary. PMI surveys are at multi-year if not decade highs, small business confidence broke the record, etc. All of these things should be deteriorating very sharply to create the potential for a recession warning.

Maybe it’ll start happening next month, I don’t know. Right now, it’s not in the data.

On interest rates:

The Fed’s going to raise interest rates in December unless something really bad happens to the stock market.

It seems quite likely that the 30-year will be headed towards 4% in the not too distant future and that would mean a steeper yield curve. The movement now in the long end has been occurring faster than the changes in the perception of the Fed, which hasn’t changed much. The long end is going up by 50 basis points in a month, which is a pretty quick annual rate and will probably continue as long as we have this situation with moving higher rates.

Rates in other parts of the world, Germany in particular, are ridiculously low relative to the economic reality. On the CPI, year over year, Germany is almost exactly the same as the United States.

Yet their rate is at 55 basis points [0.55%] and ours is at 3.15% or so. There’s a lot of room for German rates to go higher in case the ECB stops pegging it at this ridiculous rate of negative 180 basis points less than the inflationary rate.

There are two ways for things to go wrong, meaning bond yields go higher. Both of them seem to be at least plausible in the short term, if not the base case.

Here is the link to the full piece in Forbes.

Why This Matters

“There is nothing new in Wall Street. There can’t be because speculation is as old as the hills.

Whatever happens in the stock market today has happened before and will happen again.”

– Edwin Lefevre in Reminiscences of a Stock Operator

From Ambrose Evans Pritchard – The Telegraph

Prof Feldstein said the next bear market – most likely triggered by a spike in 10-year Treasury yields – risks setting off a $10 trillion crash in US household assets. The cascading ‘wealth effects’ will drain the retail economy of $300bn to $400bn a year, causing recessionary forces to metastasize.

“Fiscal deficits are heading for $1 trillion dollars and the debt ratio is already twice as high as a decade ago, so there is little room for fiscal expansion,” he said, speaking earlier on the sidelines of the Ambrosetti forum on world affairs at Lake Como.

The eurozone faces an even worse fate when the global cycle turns since the European Central Bank has yet to build up safety buffers against a deflationary shock. The half-constructed edifice of monetary union almost guarantees than any response will be too little, too late.

“The Europeans don’t have a fiscal back-up. They don’t have anything. At least you have your own central bank and treasury in Britain, so you will be happier,” he said.

“Mario Draghi is going to be very happy when he has left the ECB because it is not clear how they are going to get out of this when they still have zero rates. They can’t play the trick of the cheap euro again,” he said.

The ECB has already pre-committed to holding its reference rate at minus 0.4pc until late 2019. By then the global economy will be acutely vulnerable since the sugar rush from Donald Trump’s tax cuts and infrastructure spending will have faded.

The US is entering uncharted and perilous waters. The jury is out over whether it can – in extremis – follow the example of Japan and push the public debt ratio to stratospheric levels (245pc of GDP).

The difference is that the Japanese are the world’s biggest savers and external creditors. The Americans must import capital to finance their twin deficits.

Foreign investors own half the stock of US Treasury bonds. They will not fund ballooning deficits indefinitely. Prof Feldstein said Americans will have to cover a bigger share of the burden themselves and this will “crowd out” the US bond markets, with knock-on effects for equities.

Olivier Blanchard, ex-chief economist of the International Monetary Fund, said the US has big enough buffers to cope with a “run-off-the-mill” recession but would need to tear up the rule book altogether in a deep downturn.

Prof Blanchard, now at the Peterson Institute, said the Fed could buy equities. The Bank of Japan already does this. It is the biggest holder of exchange traded funds on the Tokyo bourse. “This could do the trick and could work even better than buying long bonds,” he said.

The Fed could even print ‘helicopter money’ to fund the fiscal deficit directly, an idea floated by academics after the last crisis but deemed too radical for the political system.

This variant of ‘people’s money’ injects stimulus directly into the veins of the economy rather than channeling it through asset markets, the post-Lehman trickle down mechanism that has greatly benefited the rich and entrenched wealth inequality. But it is difficult to reverse later when the time comes to drain excess liquidity.

While the US could in theory experiment with helicopter money, Congress would be hostile to any such form of monetary adventurism. It would be a last resort. In the eurozone it would be completely impossible under EU treaty law and the restrictive fiscal rules of the Stability Pact.

Mr Blanchard said it took at least 850 basis points of rate cuts to fight the post-Lehman recession – directly or synthetically through bond purchases under the Wu-Xia model – and this is clearly not available now. His advice is to delay monetary tightening and run the US economy hot until it is safely out of the deflationary doldrums.

A fresh crisis would expose another huge problem. Capitol Hill has tied the hands of the US Treasury and the Fed, raising serious doubts over whether the authorities could legally repeat the crisis measures that rescued the financial system in 2008.

The fire-fighting trio of the day – Ben Bernanke, Hank Paulson, and Tim Geithner – wrote a joint article in the New York Times last week lamenting that Congress had stripped the watchdog bodies of “powerful tools”.

The tougher rules constrain the Fed’s ability to halt fire-sale liquidation. The Dodd-Frank Act stops it rescuing individual companies in trouble (there must be at least five, and they must be solvent) or lending to non-banks. The Fed cannot issue blanket guarantees of bank debt and money market funds. It can lend only to ‘insured depository institutions’.

What saved capitalism in 2008 were lightning-fast moves by the Fed and the US Treasury to shore up the markets for commercial paper and the asset-backed securities markets, and to stop a run on the money market industry. It took $1.5 trillion of emergency loans to halt the vicious cycle. “These powers were critical in stopping the 2008 panic,” they said.

It is often forgotten that the Fed also saved the European financial system when the global dollar funding markets seized up in the days after the Lehman and AIG crashes. It became nigh impossible to roll over three-month dollar credits. The ECB and its peers could not create the dollars desperately needed to buttress Europe’s interbank markets.

The Fed responded with liquidity swap lines in US dollars to central bank peers, removing all limits over the wild weekend of October 14 2008. Total swaps surged to $580bn.

The problem today is that Fed no longer has the authority to do this. It needs the approval of the US Treasury Secretary, and therefore the Trump White House.

The worrying question is whether Mr Trump would refuse to “bail out” Europe in a crisis – deeming it their own problem – or might try to use this enormous power as leverage for political or trade policy objectives.

In short, it is no longer clear that there is a lender-of-last resort standing full square behind the dollarized global financial system and able to act instantly in a crisis.

Gordon Brown warned last week that lack of global solidarity threatens to leave a poisonous situation when the next storm hits. Almost all the policy survivors of the last crisis agree with him.

OK, factor all of that into your Plan 1 playbook. And to my Plan 2 friends, see the investment return opportunities on one or both sides of the coming trade. Be better prepared and aware should a reset come or not come.

Investment Positioning and Big Bets

“There is one side to the stock market; and it is not the bull side or bear side, but the right side.”

“I never argue with the tape. Getting sore at the market doesn’t get you anywhere.”

Investment Positioning

For a core portion of an investment portfolio, my firm favors diversifying to trading strategies that are global and flexible in nature. Mix those exposures with low-fee U.S. equity market exposure and make sure you’re driving forward with breaks that work. A stop-loss risk management process that may get you out and back in. A participate-and-protect approach. I also favor very selective private investment opportunities, but those are not available for all investors and something we’ll write about another day.

A few months ago, John Mauldin joined the CMG team as Chief Economist and Co-portfolio Manager of the CMG Mauldin Smart Core Strategy. John has five best-selling books and writes a free weekly e-letter called, Thoughts From the Frontline. It is one of the most widely read newsletters on the planet. I first met John in 1999. We have been friends and business partners for years. I’m thrilled he is on our team!

John wrote an excellent paper about what he is calling, The Great Reset. It describes what he sees ahead and his idea about how to get from here to there in good shape. You can sign up for a copy of the paper by clicking here. You can leave a note for John or me. Please let us know if you’d like someone from our team to call and explain the strategy to you, how it works and what portion of your portfolio may be appropriate. The paper may give you a deeper understanding of what he (we) see ahead and how to best approach the challenges.

I like to think in terms of a risk budget for an overall portfolio. For example, if one invests 80% of a $1 million portfolio in a diversified “participate-and-protect” investment approach and 20% or $200,000 in select return accelerators (liquid or private investment opportunities), the $800,000 will grow back to $1 million in a little more than six years at a 4% annualized return and sooner if returns are 5%, 6% or 7%. The idea with the $200,000 is to find four or five big return accelerators. They may be in biotechnology, private venture capital, or real estate.

I like thinking about sizing portfolios to protect what I’ve got and do so in a way that can really grow my personal wealth. Select opportunities can really make a difference and psychologically, the 80%/20% may make the ride a little easier. One keeps my wealth smartly on path while the other can accelerate my wealth. Of course, you may like 70/30 or 50/50 or 90/10. It’s important to talk to your advisor and figure out your particular risk tolerance, individual/family needs, specific goals and time horizon.

And then there are the “Big Short” types of bets. Next we’ll look at general ideas and in coming OMRs, we’ll look to get more specific. But please know this is not a recommendation to buy or sell any security and not specific investment advice for you. Please talk to your advisor.

Big Bets

Last week I shared my bullet point notes from a Felix Zulauf Barron’s article. He shared several ideas, most of which I agree with. You can find that post here.

I’m uber-focused on recessions because that’s when the bad stuff tends to happen. As long as rates are low and funding ability is high, then the party moves on. However, zero interest rate policy (“ZIRP”) has caused investors to stretch for yields and take on risks I don’t believe many fully understand. When the liquidity music stops (Fed, ECB, JCB, tax cuts, etc.), the markets will reset. The key trigger in all of this may be rising interest rates.

Debt is the central theme. We are at the end of a long-term debt cycle. That’s where I believe we’ll find the next great short opportunities. Ideas:

- Short High Yield Junk Bonds – Far too many companies received financing. Covenant quality is a bad as it’s ever been. Defaults will be epic and they will occur in the next recession when companies living on debt will no longer find funding. Watch the U.S. recession indicators and use a trend following buy/sell trigger.

- Short Emerging Market Dollar Denominated Debt

- Short Italy, short Italian banks, short Eurozone equities, short European banks and short the Euro currency vs. the dollar. As Zulauf said last week, and I concur,

On the Euro – Right on point! Watch the banks!

- Introducing the euro led to forced centralization of the political organization, as imbalances created by the monetary union must be rebalanced through a centralized system. As nations have different needs, the people are revolting; established parties are in decisive decline, and anti-establishment organizations are rising.

- The risk of a hard Brexit is high. Italy doesn’t listen to Brussels any longer. The March election brought anti-establishment parties to power that proposed a budget with a 2.4% deficit target. Eventually it will be closer to 4%. The Italian banking system holds €350 billion of government bonds. If 10-year government-bond yields hit 4%, banks’ equity capital will just about equal their nonperforming loans.

- By the middle of next year, you’ll see more fiscal stimulation in Germany, Italy, France, and possibly Spain. Governments will not care about the EU’s directives. The EU will have to change, giving more sovereignty to individual nations. If Brussels remains dogmatic, the EU eventually will break apart.

The European Central Bank

-

ECB quantitative easing ends by the end of this year. The economy has been doing well, the inflation rate has risen, and yet the ECB has continued with aggressive monetary easing, primarily financing the weak governments. This is nonsense.

-

They are the worst-run central bank in the world. I expect the euro to weaken further, possibly to $1.06 from a current $1.15.

Let’s stop for today and keep thinking this through over the coming weeks and months. There is an abundant universe of ETFs that we can use as tools to express most any bet we wish to make. We’ll get more specific in coming letters.

Let’s stay focused on what happens at the end of long-term debt cycles, how legislators and central bankers may respond and which countries sit at the probable epicenters to potential break.

As Zulauf stated last week, “Global fiscal stimulus initiatives are poison for bond markets. Bond yields are rising around the world. After major new fiscal stimulus programs are announced, perhaps from mid-2019 onward, yields will rise quickly, resulting in a decisive bear market in bonds.” More supply equals higher interest rates. The U.S. economy is growing above trend, capacity utilization is high, and the intensifying trade conflict with China suggests disruption in some supply chains, which leads to higher prices. The Federal Reserve is selling $50 billion of Treasurys per month and the U.S. Treasury must issue $1.3 trillion of paper over the next 12 months. All these factors are pushing yields up. The Federal Reserve is draining liquidity from the financial system [by not buying new bonds to replace maturing paper]. It will remove another $600 billion from the market in the next year.

Bottom line: All of this means a lot of liquidity is being withdrawn from the market, which is bearish for financial assets. How much of a decline? We don’t know. Zulauf sees maybe 25% to 30% from the top, taking nearly all other markets down with them. I’m in the -40% to -70% camp. When the declines are big enough, the central planners will come in. Central banks will ease monetary policy, buying assets if necessary. We’ll want to cover shorts and move big bets to the long side when that day comes.

I’m sticking with Plan 2: Seek growth while maintaining a level of protection against 40% to 60% corrections. Open eyes, don’t panic, become greedy when others are fearful, fearful when others are greedy, stick to plan.

Personal Note

“Promise yourself to be so strong that nothing can disturb your peace of mind. Look at the sunny side of everything and make your optimism come true.

Think only of the best, work only for the best, and expect only the best. Forget the mistakes of the past and press on to the greater achievements of the future.

so much time to the improvement of yourself that you have no time to criticize others.

Live in the faith that the whole world is on your side so long as you are true to the best that is in you!”

– Christian D. Larson

I was cleaning up at home and came across the words above. It was a card we gave to one of our kids recently. Thought I’d share it with you. Weekend game plan: let nothing disturb my peace of mind. I’m going to work on that.

Next week finds me in Las Vegas for advisor meetings next Tuesday and Wednesday. Hopefully, I can take in a show. That will help “peace of mind.” Denver follows for the TCA by E*Trade Focus on the Future event on November 5-7.

Wishing you a fine glass of wine, peace of mind and the whole world on your side. Have a wonderful weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO