This article first appeared on HiddenValueStocks

- Shares of Limbach appear extremely cheap based on 2018 EBITDA guidance, which includes unanticipated expenses (aka one-time) that are unlikely to recur in

- Assuming nothing worsens when the company reports 3Q results in November, we expect a significant relief rally. Recent management commentary appeared bullish regarding

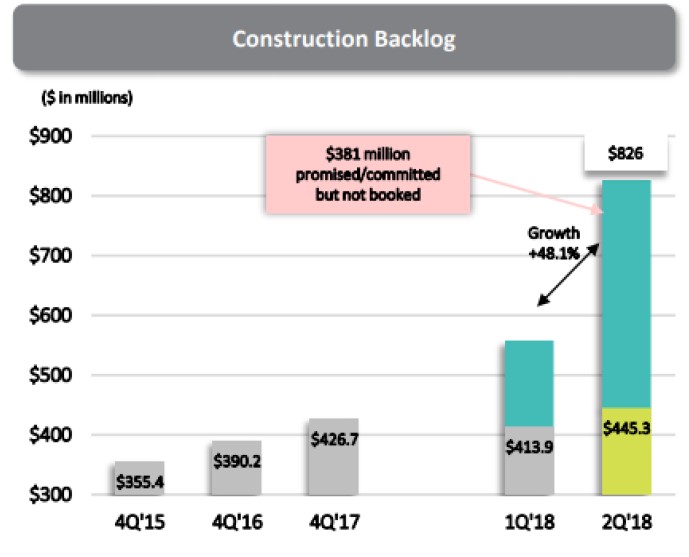

- Adding back non-recurring costs, substantial backlog growth coupled with higher pricing on that backlog, and a recently announced accretive acquisition, EBITDA should expand dramatically in 2019, even with conservative

- We believe that 2019 EBITDA that could approach $37-$41mn$18-20mn in 2018. Additional acquisitions or reimbursement from claims settlements could add further EBITDA upside.

- At a 1-2 EBITDA turns discount to 2019 peer multiples, Limbach shares would triple. Heads, I win (a lot); tails, I don’t lose much!

Q3 hedge fund letters, conference, scoops etc