Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

Q3 hedge fund letters, conference, scoops etc

Noise traders – individuals that distort the market by trading on incomplete or inaccurate information – have been discussed by academics and investors alike for decades.[1] No one could ever deny the existence of noise traders, but proponents of the efficient market hypothesis (EMH) have long contended that these traders have little-to-no impact on the overall market.

The past twenty years – which includes the tech bubble, housing bubble, and dozens of boom and bust “story stocks” – make it clear that noise traders have much more influence than EMH doctrinaires admit. That influence is only growing, as the rise of self-directed traders and the relentless noise of the financial press mean the noise to signal ratio is worse than ever. Wild swings in stocks such as Tilray (TLRY) show just how inefficient markets can be.

Get the best fundamental research

The Rise of the Noise Traders

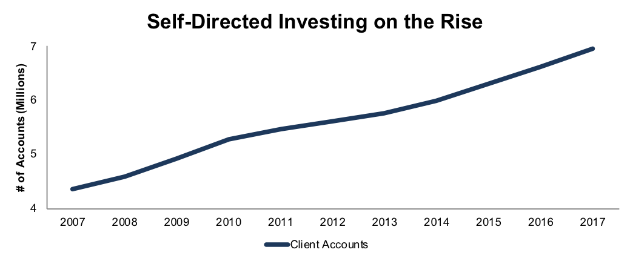

The market has more self-directed investors than ever before. New self-directed trading platforms keep cropping up, and existing platforms are gaining more and more users. Figure 1 shows that the number of accounts at TD-Ameritrade grew by 60% from 2007 to 2017.

Figure 1: Number of TD Ameritrade Accounts: 2007-2017

Sources: New Constructs, LLC and company filings

Add in Robinhood, which doubled its number of accounts to 4 million in the past year, and a wide variety of other trading platforms, and we’ve reached a point where a quarter of all U.S. adults with internet access are self-directed investors. That’s ~50 million amateur traders out there, many of whom weren’t invested during the last market crash.

By contrast, the Bureau of Labor Statistics counts just ~2.8 million professionals associated with investing,[2] many of whom are engaged in bookkeeping and other administrative tasks. The number of “professional” investors is actually much smaller than 2.8 million.

To be clear, we’re not saying that amateur investors are always bad and professional investors are always good. Many individual investors are capable of intelligent and in-depth analysis, while many professional investors – such as Bill Ackman with Valeant (VRX) – can be biased or fall prey to misleading earnings.

Moreover, our experience and independent research show that many professionals are noise traders, too. Wharton professor Brian Bushee published a study in 2004 that showed 61% of institutional investors describe themselves as “Quasi-Indexers” and 31% as “Transients” with short holding periods. Only 8% claim to be “Dedicated” investors that care to perform diligence because they hold a small, concentrated portfolio of stocks for long periods of time.

Noise Trading Works…Sometimes

These numbers might not surprise you. For most of the last twenty-five years, being a “Dedicated” investor has not paid. Momentum, high frequency, sentiment and other trading strategies have ruled the roost and generated significantly higher returns than value-based strategies.

Nevertheless, most professional investors tend to have more experience, time, and resources to understand a company’s fundamentals. They also know how to parse sell-side research and understand when a “buy” is not really a buy. They are not as likely to completely overlook fundamentals in favor of short-term trading strategies built on reactions to headlines or other noise.

Noise Trading Can Be Extremely Risky: Example: Tilray (TLRY)

Over the past few weeks, noise traders have completely controlled the market for Canadian medical marijuana producer Tilray. In just two months since its (already very expensive) IPO, TLRY rose over 1,500%, from its IPO price of $17/share to $300/share, and then dropped ~70% back down to $100 share. At its peak, the stock had an EV/Revenue ratio over 1,000.

The only other companies with such high multiples are biotech firms that trade on the hopes of successful drug research. Investors seem to be lumping TLRY in with these companies due to its status as a medical marijuana grower, but the differentiation between strains of marijuana is nowhere near as large as the patent protection that successful drug breakthroughs bring.

To justify its valuation of ~$131/share, TLRY must earn 40% NOPAT margins – equivalent to a biotech company like Amgen (AMGN) – and grow revenue by 70% compounded annually for the next 9 years. See the math behind this dynamic DCF scenario.

We think a more reasonable estimate for TLRY’s NOPAT margins is closer to 6%, near the average earned by the nine agricultural/farming companies under our coverage. If we assume it can earn slightly higher margins than other agricultural companies, ~10%, and grow revenue by 50% compounded annually for the next decade, the stock is worth just ~$13/share today, a 90% downside. See the math behind this dynamic DCF scenario.

The unrealistic assumptions embedded in TLRY’s stock price, combined with the wild daily swings, make it impossible to argue that the stock is trading on any rational assessment of its projected future cash flows.

Consequences of Noise Traders on Overall Market Efficiency

In the case of TLRY, it’s easy to view noise traders as an isolated and unimportant phenomenon. Intelligent investors can easily see how absurd the valuation is, so they know to leave the stock alone and let day traders and speculators have their fun.

For the rest of the market, however, the influence of noise traders can be subtler and more dangerous. They produce daily volatility and raise the risk (and therefore cost) for informed investors. What’s the use in putting in the work to understand fundamentals if stocks are going to move on hype anyway (e.g. TSLA and NFLX)?

When noise traders grow too influential, informed investors can either follow the hype or lose assets, which is what happened in the late 90’s. Many asset managers understood that tech stocks were in a bubble, but they also knew that if they avoided these stocks and underperformed, they could lose their jobs. The same thing happened in 2007, when Citigroup (C) CEO Chuck Prince told the Financial Times:

“As long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

When informed investors give up on making markets efficient, you get bubbles, misallocation of capital, and economic instability. While we don’t believe the market as a whole is currently in a bubble, noise traders have definitely created “micro-bubbles” in a handful of tech stocks. Note that micro bubbles precede macro bubbles. If the market continues its current trajectory, we could be in a macro bubble soon. Even if we’re not headed for a bubble, no one can argue that a greater focus on fundamentals is a bad thing.

Why Noise Traders Pose a Problem to Markets

Most people don’t have the time or expertise to analyze fundamentals. It’s much easier to get research from Mad Money!

Analyzing 200+ page quarterly and annual filings is not exactly fun. It’s dull and difficult, so we’re not surprised that so many investors rely on shortcuts to bypass this important diligence.

The real problem, however, is that most of the short cuts on which investors rely to avoid doing real diligence is designed to exploit less informed investors. The most popular research is often highly conflicted. Even sophisticated and dedicated investors must incur significant costs in terms of both time and resources to identify and verify fundamental mispricing.

However, this work is necessary to get an honest read on fundamentals. And, knowing the truth about a company’s fundamentals grows increasingly important as this bull market continues to mature.

How to Solve the Problem

The best way to combat the impact of noise traders is to reduce the cost of being a “dedicated” or informed investor. In other words, we must reduce the cost of analyzing financial reports, and we think technology needs to emerge to meet this need.

As Charles Lee and Eric So write in “Alphanomics: The Informational Underpinning of Market Efficiency”:

“Real-world arbitrage is an information game that involves a constantly improving technology. Asset managers face substantial uncertainty and risk whenever they try to identify/verify, finance/fund, and execute/implement an active strategy. At every stage of this process, they need better (more precise; more reliable) information.”

Certain[3] technologies can solve this problem by automating much of the grunt work of fundamental research. For example, the Robo-Analyst technology leverages thousands of expert-annotated financial filings to power machine learning and natural language processing technologies that analyze 200+ page 10-Ks and 10-Qs in seconds. This technology also identifies key data points hidden in the footnotes that other databases do not capture.

Investors deserve unfettered access to rigorous fundamental data. Making high-integrity fundamental research accessible to everyone would only improve the efficiency of the capital markets. We’ll never get rid of noise traders entirely, but making it easier for investors to understand the relative fundamental risks of every trade will help those that care about risk.

This article originally published on October 1, 2018.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] See the 1987 NBER paper “The Economic Consequences of Noise Traders” by De Long, Shleifer, Summers, and Waldmann.

[2] Securities, Commodity Contracts, and Other Financial Investments and Funds, Trusts, and Other Financial Vehicles

[3] Harvard Business School features the powerful impact of research automation in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

Article by New Constructs