Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Q3 hedge fund letters, conference, scoops etc

Advisors routinely assume the benefits from diversifying across equity asset sub-classes and between equities and bonds. But they ignore the even greater benefit from diversifying among categories of bonds.

Always clever, Brian Portnoy, recently wrote Diversification Means Always Having To Say You’re Sorry.

Ben Hunt doubled down with:

- It is a fact that value has waaay underperformed the S&P 500.

- It is a fact that trend has waaay underperformed the S&P 500.

- It is a fact that quality has waaay underperformed the S&P 500.

- It is a fact that emerging markets have waaay underperformed the S&P 500.

- It is a fact that real assets have waaay underperformed the S&P 500.

- It is a fact that hedge funds have waaay underperformed the S&P 500.

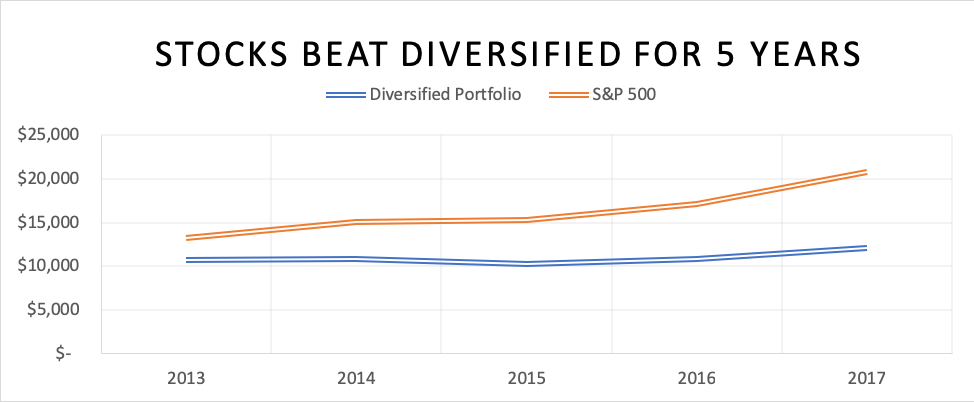

Everything has underperformed the S&P 500. Hence diversification has been a multi-year fail. Expressed in one graph, the S&P 500 versus an equal-weighting of all the major asset classes: U.S. and non-U.S. stocks, U.S. and non-U.S. bonds, real-estate, commodities, and cash.1

After five years of this advisors are tired of talking about it and investors are tired of listening. One could build a strong case for a diversification rally. But for now, diversification hasn’t worked.

Except for bonds.

Since President Trump signed the $1.5 trillion tax-cut package December 21, 2017, 10-year Treasury yields have climbed roughly 70 basis points.

10-Year Treasury Constant Maturity Rate (DGS10) Federal Reserve Bank of St. Louis

This has pushed bond prices and returns down. Year-to-date, every conventional bond category is down in total-return, except for high-yields. I exclude non-conventional categories (agencies, senior loans, preferreds, convertibles, emerging markets, TIPS, and high-yields), which advisors generally shun. Instead, they own the usual categories of U.S. and non-U.S. governments and corporates – the staples of the Barclays Aggregate and Global Aggregate indices.

As evidence, in the last two years2, 92 fixed-income ETFs have been issued, yet only 11 are diversified into multiple categories and none of these own all the 12 taxable fixed-income categories3 in material weights.

This is a shame, since if they were widely-diversified, outcomes could improve. Advisors need to add more non-conventional bonds. However, as most income investors are risk averse and protective of not just their buying power, but their principal, advisors should resist the urge to boost returns with riskier high-dividend stocks, MLPs and REITs.

In other words, diversification works for bonds, just as it does for stocks. The simplest way to illustrate this is to compare the variation of returns among stock categories to the variation of returns among bond categories. Simple returns barometers are below.

Read the full article by Andy Martin, Advisor Perspectives