There are just two energy stocks on the list of Dividend Aristocrats. One of them, Exxon Mobil (XOM), is the largest oil company in the U.S.

The Dividend Aristocrats are a group of 53 stocks in the S&P 500 Index, with 25+ years of consecutive dividend increases.

Q3 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Oil and gas production can be a “boom-and-bust” industry. Profits are highly dependent upon commodity prices, which can fluctuate wildly in any given year.

But Exxon Mobil is different. It has been remarkably stable, even through various downturns in the oil and gas industry. The company traces its roots to Standard Oil, which was founded by John D. Rockefeller all the way back in 1870. With an operating history over 100 years, and a 4.6% dividend yield, Exxon Mobil is on our list of “blue-chip” stocks. You can see the full list of blue chip stocks here.

Despite the company’s eye-popping yield, Exxon Mobil’s dividend is quite safe. You can watch a video analysis on Exxon Mobil’s dividend safety below:

This article will provide an in-depth look at the founder of Big Oil, Exxon Mobil.

Business Overview

In its early days, Standard Oil came to dominate the U.S. oil and gas industry. It did this with a laser-like focus on drilling innovation, production growth, and limiting costs.

Standard Oil was almost too successful—it grew at such a rapid pace that in 1911, it was dissolved by the U.S. Supreme Court on antitrust grounds. Standard Oil was broken up into 33 smaller companies, many of which became giants on their own, such as Chevron (CVX).

Many of the same business practices used by Standard Oil, are still used today by Exxon Mobil. Specifically, the company focuses on high-return projects that allow for profitable growth.

The company generates a high return on invested capital, a key measure of a management team’s ability to effectively deploy capital. Exxon Mobil has consistently generated industry-leading returns on capital employed.

The company operates three large business segments. The Upstream segment includes oil and gas exploration and production. Downstream activities include refining and marketing. Manufactured chemicals include olefins, aromatics, polyethylene, and polypropylene plastics.

Growth Prospects

The climate for oil and gas majors remains challenged because oil prices are still down by roughly half from the peak levels of 2014.

Fortunately, Exxon Mobil is an integrated company. Its upstream and downstream businesses complement each other well and help insulate it from swings in the prices of commodities. Indeed, when oil and gas prices decline, upstream profits fall. But, downstream tends to benefit from sharp fluctuations in oil prices.

This helps Exxon Mobil’s profits hold up relatively well compared with other oil and gas majors. Earnings-per-share have risen by 30% in the first three quarters of 2018 now that oil prices have stabilized in the area of $50.

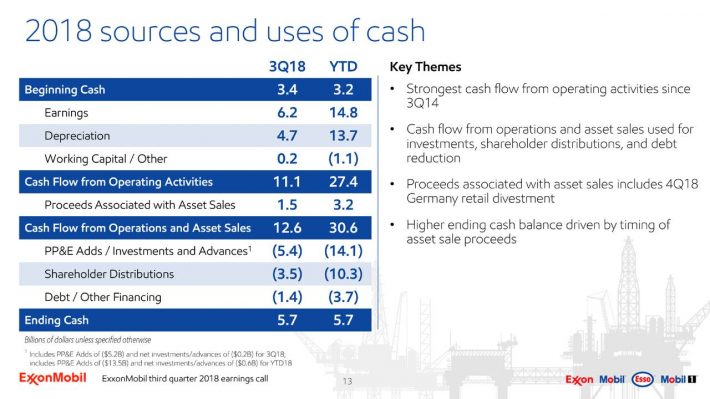

Source: Earnings Presentation, page 13

The fact that ExxonMobil can operate so profitably in an environment of $40 to $50 speaks to how efficient it is.

Exxon Mobil has also boosted cash flow, thanks to its focus on cost discipline. After years of cutting capital expenditures when oil prices were the lowest, ExxonMobil has begun the process of rebuilding its spending. Capital expenditures are up 28% in the first three quarters of the year but are still quite low by historical standards. Capital spending during the peak oil days was still another ~50% higher than today’s levels, so ExxonMobil hasn’t lost its sense of discipline by any means.

Despite unfavorable oil pricing, ExxonMobil generated $12.6 billion in free cash flow in the first three quarters of the year. Keep in mind this is despite a nearly 30% increase in capital spending, which reduces free cash flow. This terrific result highlights how strong ExxonMobil’s operating model is, even when oil prices don’t necessarily cooperate.

This is more than enough to continue paying the dividend, which has cost about $10 billion over the first three quarters of the year.

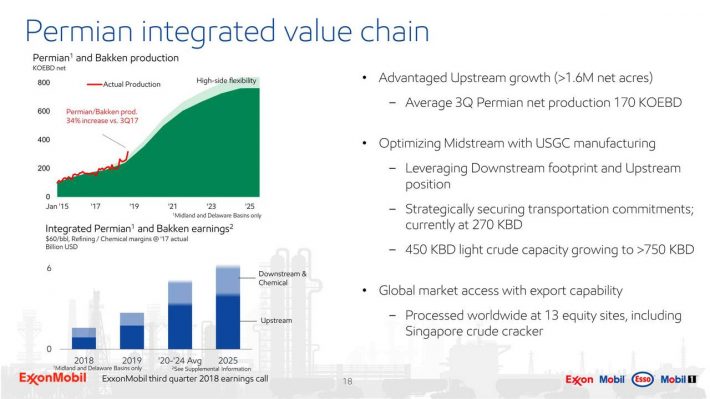

Going forward, future earnings growth would be accelerated with higher oil and gas prices. But growth will also come organically from the company’s long list of new projects. The Permian Basin is one of the strongest oil fields in the U.S., and is an area of high investment for Exxon Mobil.

Source: Earnings Presentation, page 18

Exxon Mobil has a massive project pipeline, consisting of more than 100 new projects. In addition to the Permian Basin, Exxon Mobil has significant international projects located in offshore Guyana, and Angola.

Production increases have been somewhat spotty in recent quarters as Exxon Mobil is now feeling the impact of lower capital expenditures in past years. However, production is set to rise in the coming years as its legacy projects contribute more and as some of its larger growth projects come online. Thanks to these factors, we expect a low single digit tailwind to production volumes in the coming years.

Competitive Advantages & Recession Performance

Exxon Mobil enjoys several competitive advantages, primarily its tremendous scale, which provides the ability to cut costs when times are tough.

It also has the financial strength to invest heavily in new growth opportunities. The company has allocated tens of billions of dollars in the past few years to capital expenditures to support future growth:

- 2014 capital expenditures of $33.0 billion

- 2015 capital expenditures of $26.5 billion

- 2016 capital expenditures of $16.2 billion

- 2017 capital expenditures of $15.4 billion

Another competitive advantage is Exxon Mobil’s industry-leading balance sheet. It has a credit rating of AA+, which helps it keep a low cost of capital.

Exxon Mobil’s integrated business model allows the company to remain profitable, even during recessions and periods of low commodity prices. The company saw volatility during the Great Recession, but still remained profitable:

- 2007 earnings-per-share of $7.26

- 2008 earnings-per-share of $8.66 (19% increase)

- 2009 earnings-per-share of $3.98 (54% decline)

- 2010 earnings-per-share of $6.22 (56% increase)

Continuing to generate steady profits allowed Exxon Mobil to keep raising its dividend each year.

Valuation & Expected Returns

Exxon Mobil appears to be somewhat overvalued today. We estimate earnings-per-share of $4.50 for 2018, implying a current price-to-earnings multiple of 16. That compares somewhat unfavorably to our fair value estimate of 13 times earnings. However, keep in mind that the company’s earnings haven’t yet recovered from the decline that began in 2015 as oil prices remain low by historical standards.

Thus, even modest increases in the prices of natural gas and oil could see Exxon Mobil produce sizable earnings growth. Indeed, we expect the company to produce nearly $8 per share in earnings by 2023, so the opportunity for growth is sizable. Given this, the somewhat high valuation probably makes sense.

Much of this depends on the direction of oil and gas prices, which are difficult to predict. To account for this uncertainty, investors may want to err on the side of caution when forecasting future earnings growth.

With that in mind, a potential breakdown of long-term returns is as follows:

- 11% annual earnings growth

- 4.6% dividend yield

- -4% valuation change

Exxon Mobil’s operating earnings could reasonably increase by at least 8% each year. Adding in share repurchases could elevate total earnings growth to 11%. In this scenario, total returns would reach approximately 12% annually after accounting for the high current valuation, which we expect will moderate over time.

Of course, earnings growth is not likely to be this smooth, and is subject to change depending on oil and gas prices. Still, it appears that Exxon Mobil stock is poised to deliver strong returns to shareholders in the coming years.

Final Thoughts

Exxon Mobil has had a difficult past few years demonstrating that it is susceptible to falling oil and gas prices. However, it has performed better than most other energy stocks in this time frame.

And, Exxon Mobil has a bright future. The company has many promising new projects nearing completion, and it generates more than enough cash to continue raising the dividend.

As a result, Exxon Mobil stock appears attractive based on earnings growth and dividend growth potential.

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.

Article by by Josh Arnold, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.