Cincinnati Financial has increased its dividend for an amazing 58 years in a row. It is a Dividend Aristocrat, a group of stocks in the S&P 500 Index, with 25+ consecutive years of dividend increases.

Q3 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Not only that, but Cincinnati Financial is also a member of the Dividend Kings, an even more exclusive group than the Dividend Aristocrats. Dividend Kings have increased their dividends for 50+ consecutive years. There are just 25 Dividend Kings.

Cincinnati Financial’s dividend track record is legendary. And yet, the stock does not appear to be an attractive buy right now. The reason is because its valuation has expanded considerably in the past few years, above its underlying earnings growth rate.

Business Overview

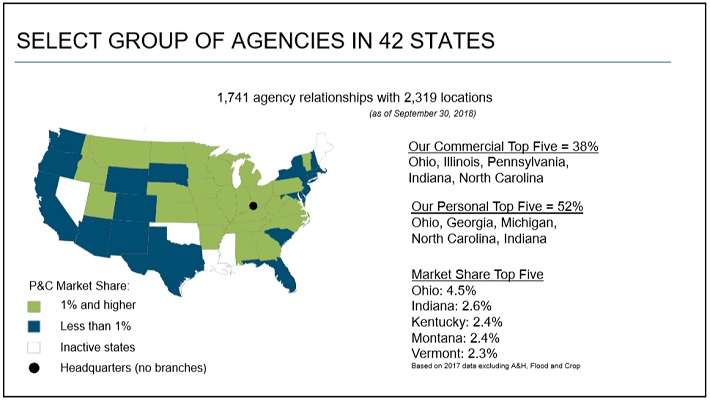

Cincinnati Financial is an insurance company, founded in 1950. It offers business, home, and auto insurance, as well as financial products including life insurance, annuities, and property and casualty insurance. Revenue is derived from five sources, with agencies across 42 states.

Source: Investor Handout, page 4

The company has a profitable business model. Instead of focusing solely on high-margin products, Cincinnati Financial is willing to write lower-margin policies. It earns a high level of profit by issuing high volumes and taking market share.

In addition, as an insurance company, Cincinnati Financial makes money in two ways. It earns income from premiums on policies written, and also by investing its float, the large sum of premium income not paid out in claims.

This has led to steady growth over many years, and there should be room for continued growth up ahead.

Growth Prospects

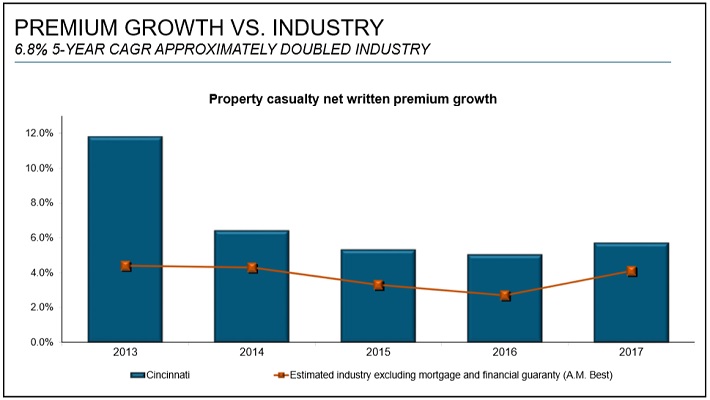

Cincinnati Financial has a positive growth outlook moving forward. Growth should continue to come from new policies written. The company has a successful history of growing profits through new policies written.

Source: Investor Handout, page 13

Price increases helped the company grow revenue from premiums over the past year. Rising interest rates will also give the company a boost. Interest rates have risen over the past year, which will help Cincinnati Financial earn higher income from its investment portfolio.

Cincinnati Financial’s strong performance continued in 2018. The company released strong results for the third quarter. Total revenue increased 36% for the quarter, to $1.91 billion. Earned premiums increased 4% to $1.3 billion. Adjusted earnings-per-share of $0.84 beat by $0.11 per share, up 45% year-over-year. The high growth rate was due largely to a $355 million investment gain, as well as earned premiums growth. Book value per share increased 1.8% to a record high for the quarter.

The company also acquired MSP Underwriting Limited, a global specialty underwriter from Munich Re for approximately $131 million. The acquisition of MSP will boost its international growth.

Cincinnati Financial’s earnings-per-share will grow considerably for 2018, but much of this growth will be due to non-recurring items, such as the 2017 damages from Hurricane Harvey and tax reform. Over the long-term, the company’s growth prospects are more modest, due to the mature nature of the industry. We see a 5% annual earnings growth rate as a reasonable projection for the next five years.

Competitive Advantages & Recession Performance

There are not many identifiable competitive advantages in the insurance industry, other than brand recognition. There are not very high barriers to entry in insurance, which leads to fierce competition.

Fortunately, Cincinnati Financial has decades of experience, and has built a close relationship with its customers.

Insurance companies are not immune from economic downturns. Cincinnati Financial does not have a highly recession-resistant business model. Earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $3.54

- 2008 earnings-per-share of $2.10 (41% decline)

- 2009 earnings-per-share of $1.32 (37% decline)

- 2010 earnings-per-share of $1.68 (27% increase)

As you can see, earnings declined significantly from 2008-2010. Insurers like Cincinnati Financial typically sell fewer policies during recessions, along with poor performance of their investment portfolios when markets decline.

That said, the company did remain profitable during the recession, which allowed it to continue increasing dividends each year. And, the company enjoyed a strong recovery in 2010 and thereafter, once the recession ended.

Valuation & Expected Returns

Cincinnati Financial stock has outperformed the broader S&P 500 Index over the past 30 years. The share price has continued to rise in recent years. The combination of weak growth and a rising share price means the stock now trades for a relatively high valuation.

Based on 2018 earnings-per-share forecasts, Cincinnati Financial stock trades for a price-to-earnings ratio of approximately 23.1. In the past 10 years, Cincinnati Financial stock held an average price-to-earnings ratio of 20.5, although the valuation is skewed by an elevated price-to-earnings ratio in 2011.

Based on comparable valuations in the insurance industry, our fair value estimate is a price-to-earnings ratio of 14. Cincinnati Financial is a high-quality company with a long dividend history, but insurance companies typically do not hold price-to-earnings ratios in the high-teens. For example, insurance industry peer and fellow Dividend Aristocrat Aflac (AFL) has a fairly low price-to-earnings ratio of 11.2.

As a result, we view Cincinnati Financial stock as overvalued. If the shares revert to their fair value price-to-earnings ratio, future returns would be reduced by 9% per year.

Earnings growth and dividends will help offset the decline. However, the company has fairly modest growth expectations. We forecast 5% annual earnings growth for Cincinnati Financial. In addition, the stock has a current dividend yield of 2.7%. Cincinnati Financial’s dividend is highly secure, and a projected payout ratio of 66% leaves room for future dividend increases.

Still, the stock is expected to produce negative total returns of 1.3% per year over the next five years.

Final Thoughts

Cincinnati Financial is a steady company with a consistent dividend payout, and the ability to raise the dividend modestly each year. The dividend payout is highly secure.

While the company has a strong business model and is solidly profitable, it does not seem to be a particularly attractive stock from a valuation standpoint. Overall, investors interested in buying this stock should wait for a lower valuation and higher dividend yield.

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.

Article by Bob Ciura, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.