Senior Investment Strategist Steve Lipper shows how a slow economy, an accommodative Fed, and the calendar add up to positive prospects for small-cap stocks.

Q3 2019 hedge fund letters, conferences and more

Our recent research has uncovered some interesting historical patterns that offer a sizable measure of encouragement to small-cap investors. When economic, monetary, and market conditions have looked similar to today’s, small-caps have enjoyed subsequent returns nearly twice their historical average while avoiding losses the vast majority of the time. This three-ingredient cocktail is near-term weak economic growth, an accommodative Fed, and positive seasonality.

Most investors are aware that small-caps are more subject to cyclicality than their large-cap siblings and that small-caps typically do well when the economy is expanding. However, many investors may not be aware that the weaker the current economy, the stronger subsequent small-cap returns tend to be.

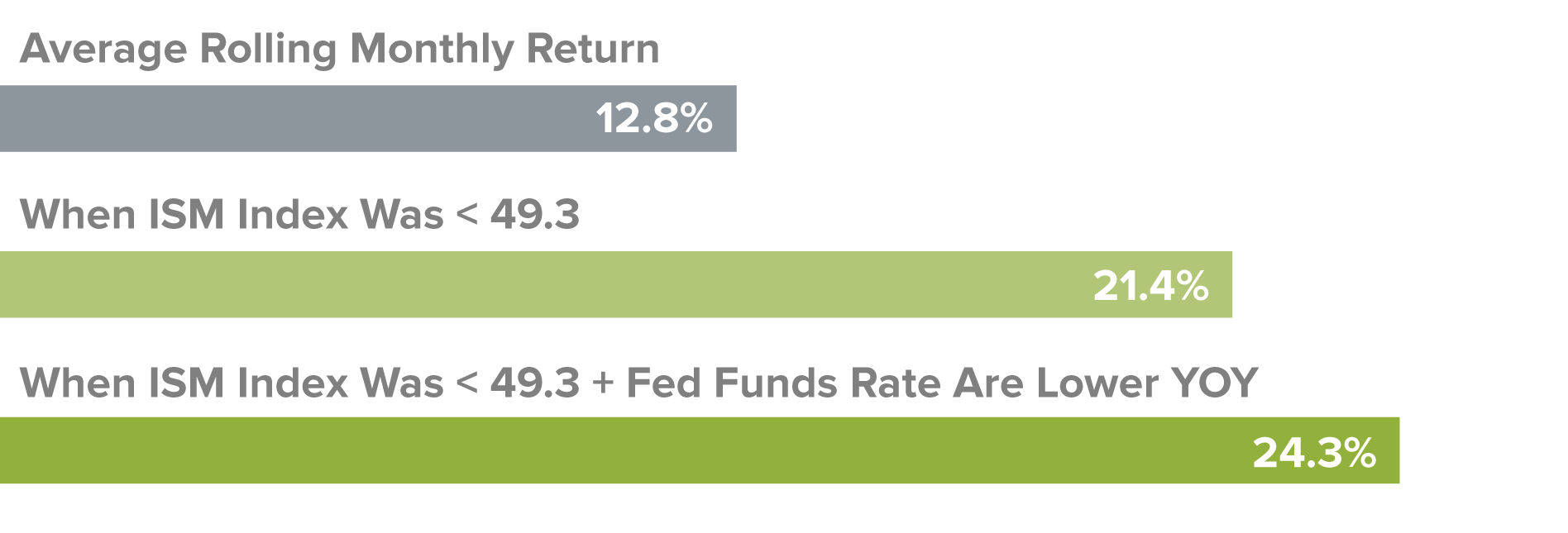

Our analysis began by taking an investment start date during months when the ISM Manufacturing Index was in the bottom 25% of its historical readings—that is, less than 49.3—since 1978. From those low points, the subsequent average 12-month return for the Russell 2000 Index was 21.4% compared with 12.8% for all 12-month periods since the small-cap index’s 1978 inception.

Most investors also know that an accommodative Fed has been good for equity returns regardless of cap size. If we add environments when the Fed Funds rate was lower than it was 12 months prior with those periods of low ISM Manufacturing Index readings, the subsequent small-cap results were even stronger, with an average subsequent 12-month return under these dual conditions of 24.3%.

Small-Cap Results in Two Scenarios vs. Long-Term Rolling Average

Russell 2000 Monthly Rolling 1-Year Returns by Starting ISM Level

From 12/31/78 through 9/30/19

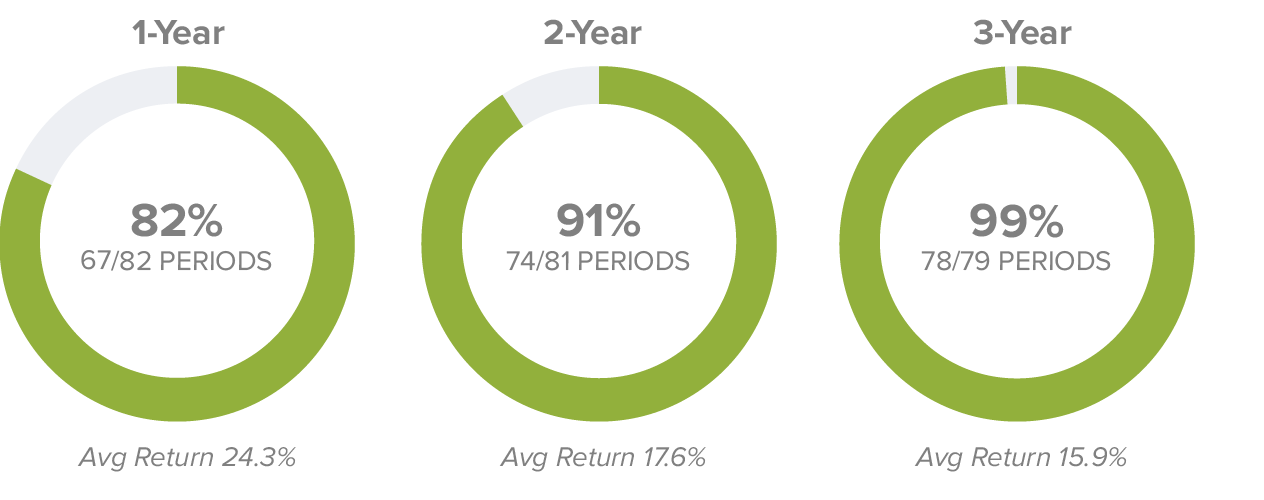

The percentage of periods in which investors avoided a loss in these environments was also striking—and are especially relevant for cautious investors concerned about preserving capital and avoiding losses. In periods with both low economic readings and an accommodative Fed, small-cap returns were positive in 82% of all one-year periods, 91% of two-year periods, and 99% of three-year periods.

Percentage of Periods with Positive Russell 2000 Returns*

*In Periods With Near-Term Weak Economic Growth and an Accommodative Fed

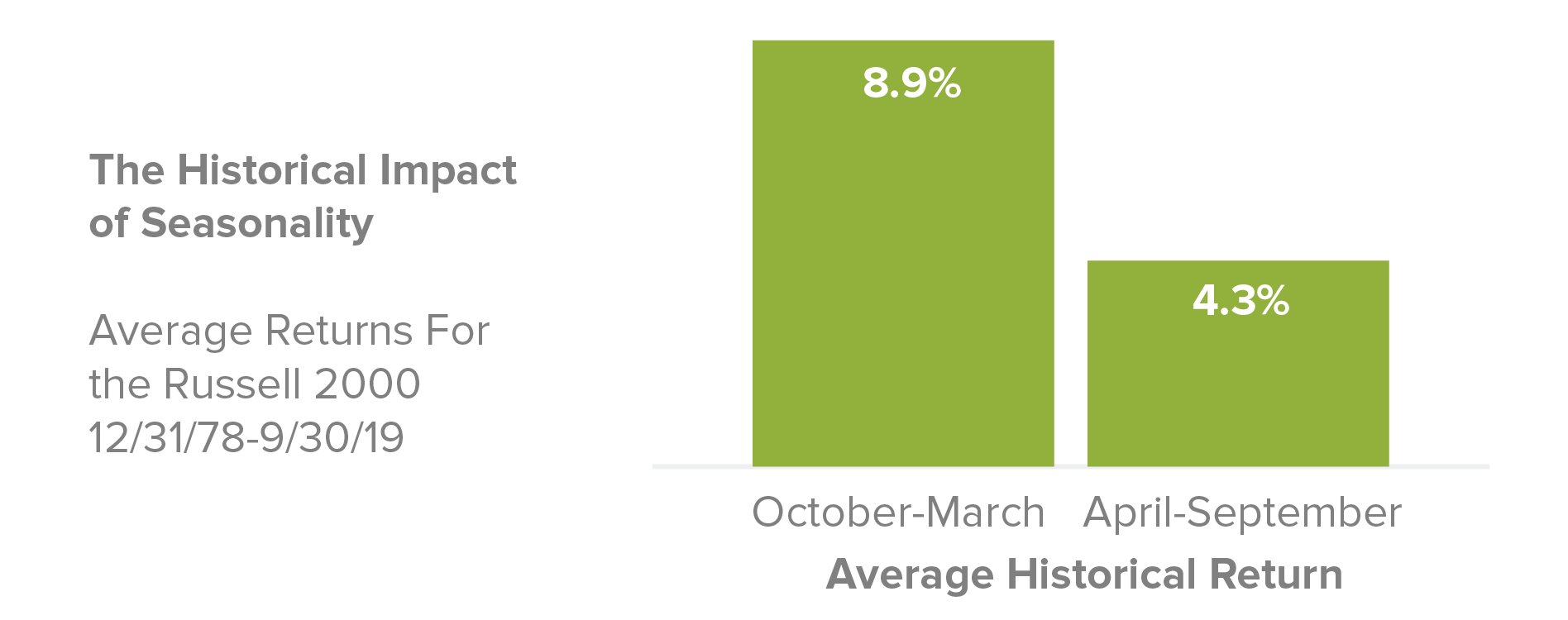

The final component to this bright outlook for small-cap performance is seasonality. Across the globe, equities as a whole have enjoyed higher historical median returns from October through March than they have from April through September. Explanations vary as to the cause of this pattern, but regardless of the reasons, we think it’s important that investors know about it. For the Russell 2000, the historical average return for the six-month period from October through April was 8.9%, while it was only 4.3% for the April through September period.

With all three of these positive conditions currently present—low ISM Manufacturing Index readings, an accommodative Fed, and positive seasonality—we think it’s a very attractive time for investors to consider additional investments in small-caps.

Article by The Royce Funds