Over the last week, markets have been moving mainly due to messages of the European Central Bank and the Federal Reserve. However, single decision of one or the other bank regarding interest rates does not really matter. Much more important are plans and announcements for the following months.

Q1 hedge fund letters, conference, scoops etc

ECB or Fed – who will print more?

Recent months show how the Fed plans (the most important central bank in the world) can quickly change. At the beginning of October, its head Jerome Powell claimed that further interest rate hikes are appropriate, so their level would eventually become equal to inflation.

After two months, in December, interest rates were raised, while Powell suddenly announced that the neutral level of interest rates has been virtually reached. Pressure caused by the stock market declines forced the Fed to move away from its policy of hiking rates and balance sheet reduction. As a reminder, the balance sheet reduction means that the Fed gets rid of some assets from the balance sheet, thus decreasing liquidity in the markets. This is crucial, because over the last decade stock prices have been dependent on the size of central banks’ balance sheets – if printing has been carried out, share prices has been increasing. On the other hand, if the Fed has not been printing, share prices have been dropping.

Over this year, the Fed indicated that series of interest rate increases has been temporarily suspended and the balance sheet reduction will be finishing in September. Below you can see how much it has been reduced (compare current levels with those from 2007 – before the first round of printing).

Source: Federal Reserve Bank of St. Louis

To put it simple: it turned out that the U.S. central bank is not able to normalize the policy for a long time. We have also written about it in recent years, while some part of the market was hoping it would be different.

Fed is no exception. The ECB case looks even worse – printing officially finished in December. Economic environment in Eurozone was not good, so the European Central Bank announced in March another round of cheap loans for corporations. This move turned out to be insufficient, so the ECB head Mario Draghi two weeks ago sent a message that interest rate cuts and another round of bonds purchases (using currency created out of thin air) are possible in the future.

We would like to remind you that the main interest rate in Eurozone is 0%, so Draghi has actually declared negative interest rates!

After Draghi’s words, euro began to lose significantly (if the ECB announces printing, it means weakening the European currency).

The ECB’s statement was immediately commented by Donald Trump, who hinted that Draghi strengthens the dollar, which harms American exporters. There is no doubt that ECB moves will be used as an argument for policy easing by the Federal Reserve. It does not matter if the Fed lowers rates now or in a month time. It is simply about finding strong arguments for abandoning rate hikes and bringing their levels below zero.

Rate cuts are not enough

From December 2015 to December 2018, Fed increased interest rates from 0% to 2.5%. It is not much considering the past rate hike cycles, but in current reality this is a significant change because the European Central Bank and the Bank of Japan are not able to raise rates by as much as 0.25%.

Reducing interest rates means that governments, businesses and households can borrow at a lower cost. Theoretically, this is positive information for the stock market. In practice, however, the first long-term reduction in interest rates is a strong message: the economic situation has deteriorated significantly, so we must ease the policy.

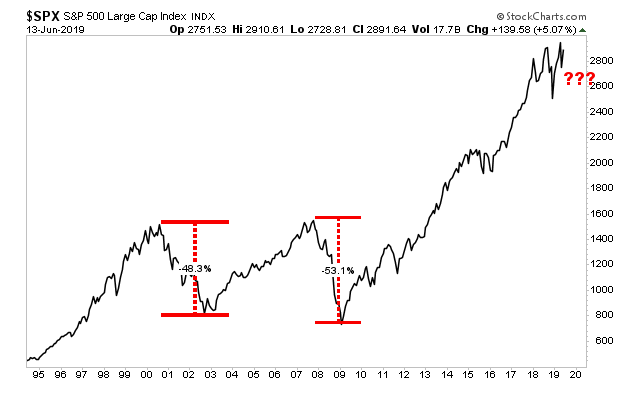

In the 21st century, first rate cut by the Fed (2001 and 2007) meant beginning of a recession in the economy and bear market in the stock market. Main stock indices has fallen then twice by about 50%.

Key question: is it going to be the same this time or maybe the Fed will change the course early enough and in this way will be able to prevent the collapse?

In our opinion, we have reached the point where interest rate cuts are not enough to save the situation. We know that a lot of people pay attention to the stock market, which is close to their all time high. Unfortunately, it is the currency and bond markets that respond faster to events.

In case of the currency market, despite the announcement of loosening monetary policy, the dollar still looks quite strong, which means that capital flies into currency considered as safe:

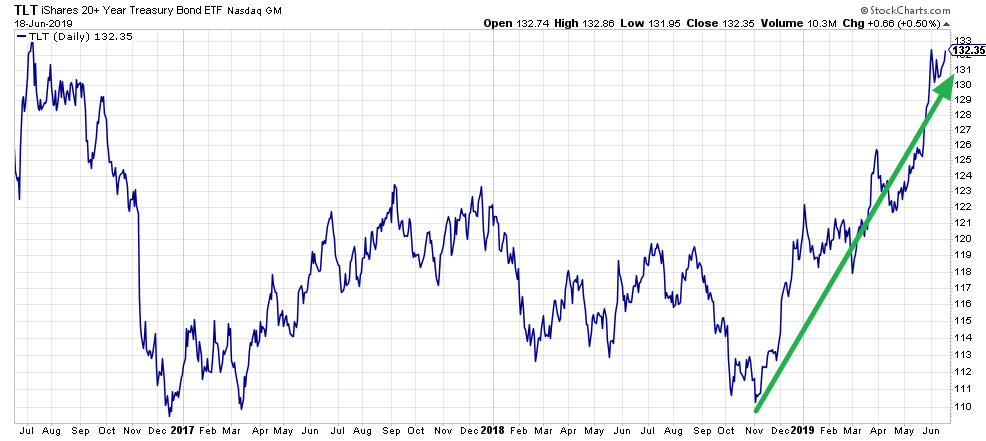

Bonds, on the other hand, are the assets to which investors escape when anxiety prevails and when inflation expectations decrease (which is typical of the final stage of the economic cycle which we currently have). Below chart shows long-term U.S. bonds (strong rally over recent months):

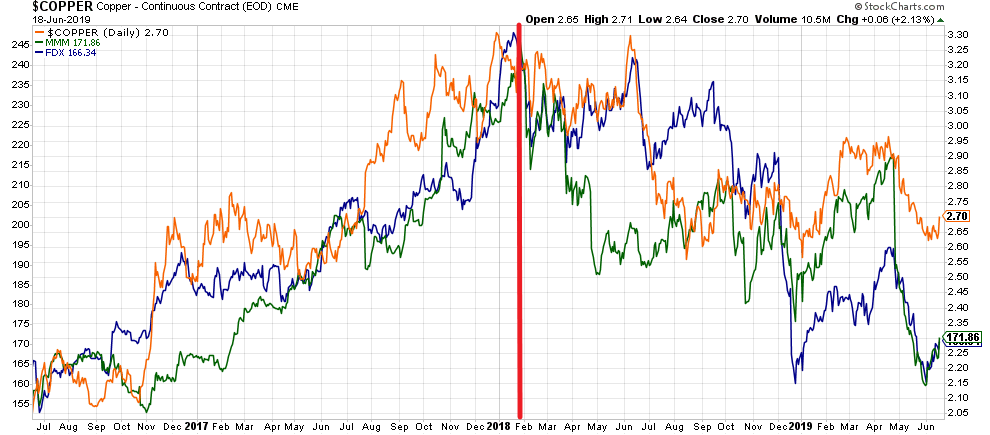

On the next chart you can see several interesting measures that reflect the economic situation. Copper price (orange), FedEx share prices (blue), 3M (producer of 55 thousand different products) share prices (green). The last two companies well reflect the state of the economy.

As you can see, in almost all of these reference points, change in the trend occurred at the beginning of 2018 (the peak of the economic situation).

All of the above charts indicate strong economic slowdown. Of course, the same is indicated by data from Europe, South America and Asia – we have referenced them a lot recently, so we will not repeat ourselves.

What will the FED do?

At the moment market assumes that by March 2020, Fed will cut interest rates 3 or 4 times. Those cuts are already included in asset prices on the stock market, so in the event of strong recession in the U.S. (as many points indicate that) rates reduction will be not enough.

What can be the next Federal Reserve moves? Most likely, we will see again bonds purchases with the currency created out of thin air (the so-called QE). It is quite likely because such plans have been recently announced by the ECB. It is possible then, that in the media we will be observing theater in which the ECB will increase printing, and the Americans will accuse Europe of unfair currency weakening. Therefore, the Fed will have an excuse to return to printing as well. However, it will only be a scene presented for the crowd, and in fact both sides will be able to justify what they need – which is printing, printing and once again printing.

The problem is that keeping artificially low interest rates and putting additional capital on the market helps to calm the situation on the stock market, but is not always able to heal the economy. Why? The reason is simple. If we have a terminal phase of the cycle, where the debt at each level is horrendously high, what difference is supposed to bring lowering credit costs?

If one have just eaten three dinners, it will be very difficult for him to eat the fourth, even if the restaurant manager says that the meal is free.

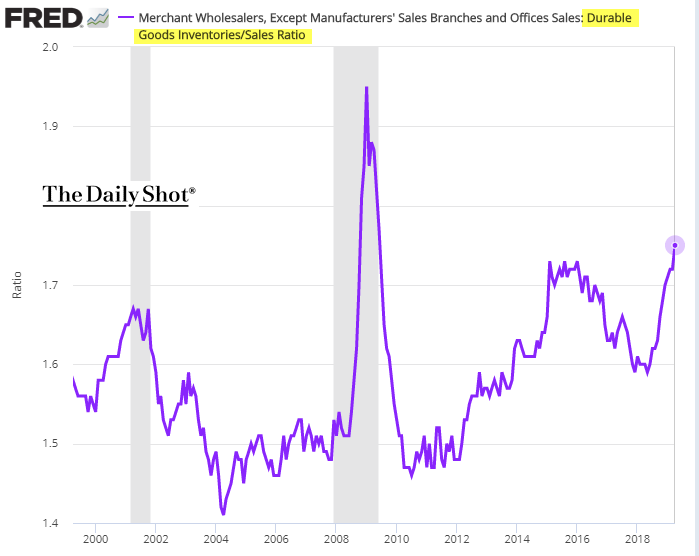

Yes, based on cheaper credit, some enterprises can exist and further operate. What if demand for their goods and services will decrease? This is manifested, for example, by an increase in inventories, because goods are not found by buyers (chart below shows durable goods inventories e.g., cars, furniture to sales ratio).

source: Wall Street Journal

We must not forget that the situation in the economy will be exacerbated by tariffs. While for Donald Trump they are the good argument for elections campaign, then for Americans they simply mean higher prices of products. This in turn means that U.S. citizens will buy less goods, e.g., from Asia. This will translate into lower earnings of Asian companies that will have to lay off some employees. In this way, political decisions will spread around the global economy.

As you can see, tariffs will certainly not support the situation.

In the end, Fed will have to use more radical measures. Few months ago, one of the Fed representatives has admitted that they are ready to use tools which during the previous crisis were considered as too extreme (!).

In our view it going to happen.

Summary

We can certainly say that central banks are preparing to fight for higher inflation, which can help them reduce the value of debt. After the ECB and FED messages we already know that the first tool will be interest rate cuts. Then, the second one, assets purchases using the currency straight from the printer. Change will be based on the fact that printing will become regular tool for central banks, not just the last resort.

As we mentioned earlier, all this may not be enough to improve the economic situation (stock prices or bonds are the separate matter). The Fed will be forced to use extreme tools. At some point, the current deflationary tendency (we do not say that inflation is low, but that it is temporarily falling in many economies) will reverse by 180 degrees. Then, dollar will start losing and commodity related currencies will strengthen.

For investors, the key question still is: will we see the stock market sell-off, or will the investors shed on assets before the central banks confirm introduction of ultra loose monetary policy? In our view, we will see significant declines this year, because central banks’ reaction will prove to be too late and too weak.

Finally, it is worth adding that the inflationary breakdown, which will occur should not be associated with economic development. It will be a period of stagflation, or economic stagnation combined with high inflation. All those things will remind you the events from the 70’s.

Article by Independent Trader