The Fed is in focus this week, and for very good reason. But if you look further afield you’ll see that a clear global monetary policy pivot is already underway. One good example worth a closer look is emerging markets, where the policy pivot is particularly notable.

Q1 hedge fund letters, conference, scoops etc

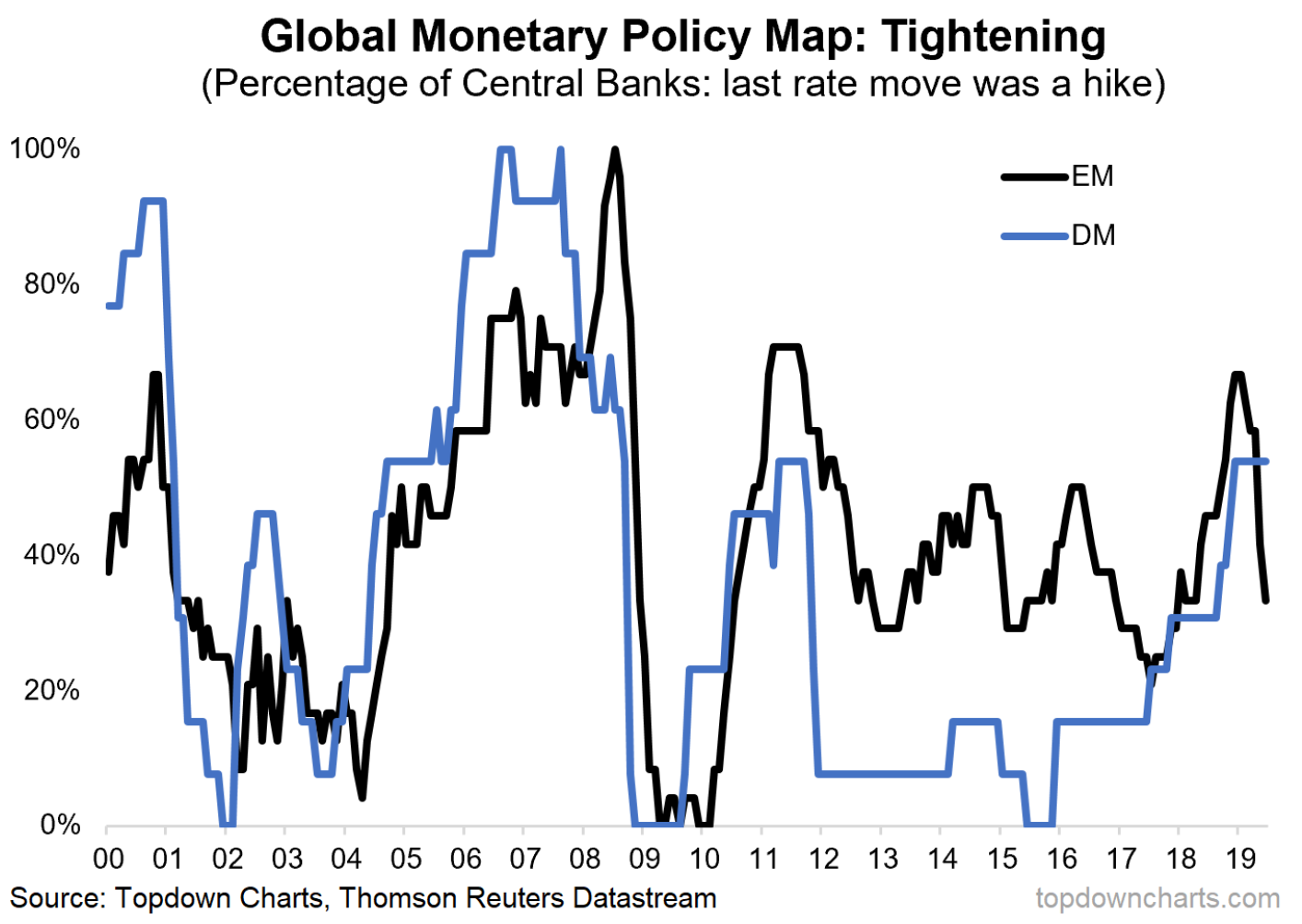

Today’s chart comes from a report on emerging market equities where I outlined the improving policy and macro backdrop (which along side cheaper valuations and bearish sentiment helps the overall picture).

The chart of the day shows the proportion of central banks whose last interest rate move was a hike (increase).

Clearly if all central banks were tightening policy it would be at 100%, and if all central banks were cutting rates, it would be at 0%. I have split it out for EM (emerging markets) and DM (developed markets), which yields a couple of interesting insights.

Through 2017/18 more and more central banks were tightening monetary policy as the global growth/inflation picture looked the best in years.

But at about the turn of the year the softening data pulse, heightened market volatility, and then later the trade war escalation helped bring about a shift. And this global monetary policy pivot is probably only going to spread further from here.

The Fed may well join the policy pivot party later this week with a rate cut (or at least eventually), but already there has been a pivot in the tone and a wind-down of quantitative tightening.

As for the investment implications, generally speaking easier monetary policy is better for risk assets, and for emerging markets, the economic pulse has begun to stabilize on some metrics. Against a backdrop of cheaper valuations and bearish sentiment, the outlook for EM equities is arguably improving (though not without risks!).

—

This article originally appeared as a submission at See It Market

Article by Top Down Charts