Are you looking for a profitable and debt-free company with attractive key metrics, high insider ownership and strong catalysts? Do you also want it to be off the beaten path? If this is the case, don’t look any further. Welcome Epsilon Energy (EPSN).

Q1 hedge fund letters, conference, scoops etc

I’m not surprised if you have never heard of this company. Epsilon Energy traded on the Toronto board under the ticker EPS until mid-March 2019. But due to extremely low awareness in Canada, it was voluntarily delisted from Toronto a few weeks ago and since mid-March 2019, it has been traded on the Nasdaq in an effort to raise awareness while seeking a wider pool of potential investors.

To get this kind of information and other exclusive articles before regular readers, get on the VIP Mailing List today.

********

Assets Overview

EPSN is a hybrid company because it has a natural gas weighted upstream business (more than 90% of the production is natural gas) and a midstream business.

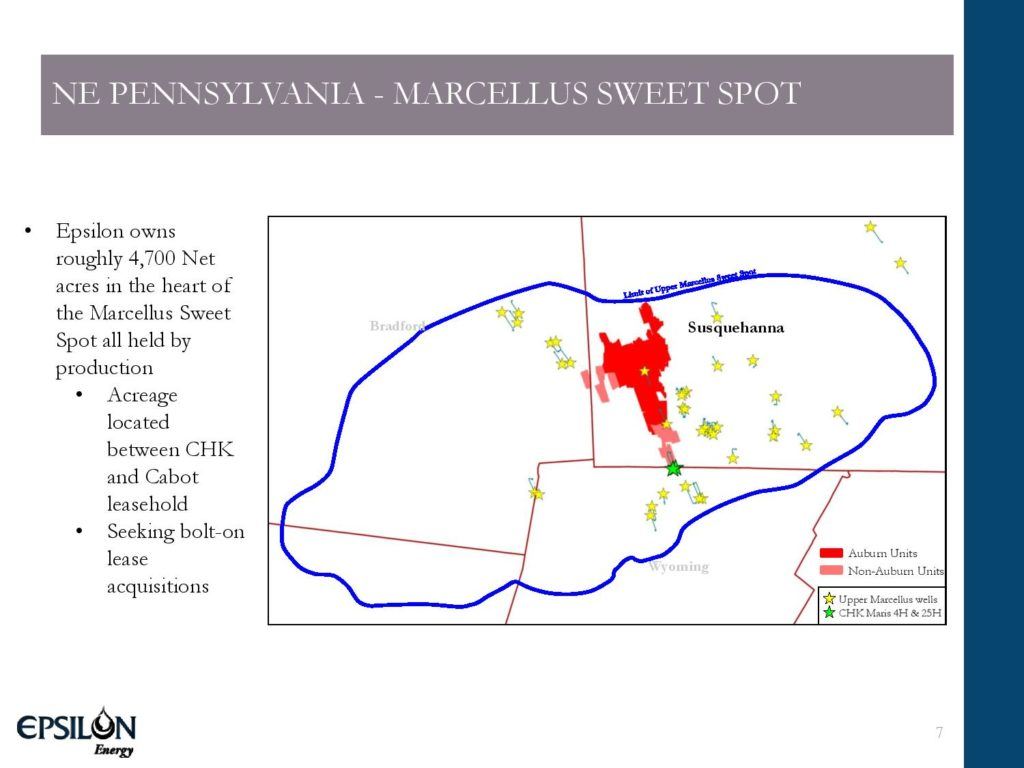

Its upstream segment primarily focuses on the Marcellus shale comprising approximately 4,700 net acres located in the southwest Susquehanna County in Pennsylvania, as illustrated below:

Actually, the company’s acreage is in the sweet spot of the Marcellus shale with offset operators being major energy producers such as Cheasapeake Energy (CHK) and Cabot Oil & Gas (COG).

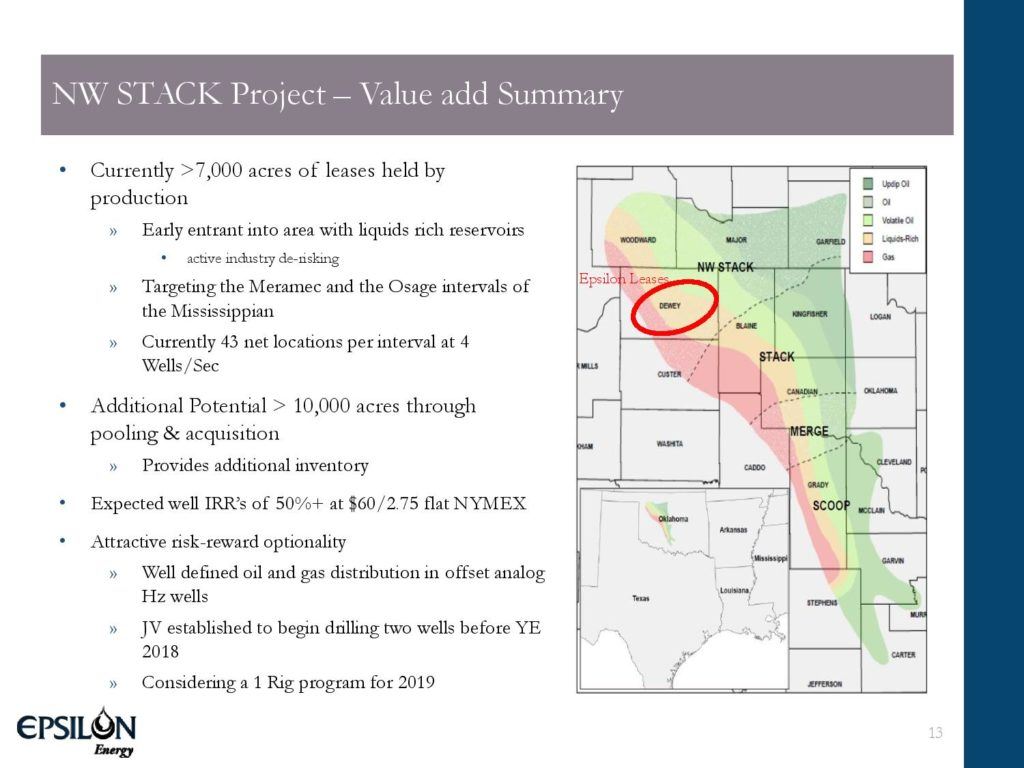

Also, in the first quarter of 2017, EPSN expanded its upstream business by acquiring a strategic position in the Anadarko Basin of Oklahoma. During 2017, it closed multiple acquisitions in the Basin which include varying interests in over 88 sections of land, all held by minor production from shallower intervals, including operations covering 21 sections. The leasehold position includes rights to the prospective and deeper Meramec, Osage and Woodford formations. This position covers a wide footprint encompassing oil, condensate and liquids rich gas prone areas in the over-pressured window of the Basin.

Currently, it holds more than 7,000 net acres in the Anadarko Basin with offset operators being Encana Corporation (ECA), Continental Resources (CLR) and Devon Energy (DVN), as illustrated below:

and below:

When it comes to the midstream business, EPSN owns a 35% interest in the Auburn Gas Gathering System (GGS) with partners Appalachia Midstream Services, LLC (43.875%), a subsidiary of Williams (WMB), and Statoil Pipelines, LLC (21.125%), a subsidiary of Equinor (EQNR).

The Auburn GGS consists of 43.9 miles of gathering pipelines, a small auxiliary compression facility and a main compression facility with three dehydration units and three Caterpillar 3612 compression units. Design capacity of the Auburn compression facility is approximately 360,000 thousand cubic feet, or Mcf, per day.

All of the company’s production from its Pennsylvania acreage is dedicated to the Auburn GGS located in Susquehanna County, Pennsylvania for a 15 year term expiring in 2026 under an operating agreement whereby the Auburn GGS owners receive a fixed percentage rate of return on the total capital invested in the construction of the system. That said, 100.1 Bcf (or 274 MMcf/d) were gathered and delivered in 2018 through the Auburn System which represents approximately 83% of designed throughput capacity.

Profits And Free Cash Flow In 2018

The Marcellus production averaged 22 MMcf/d for the fourth quarter of 2018 and 23 MMcf/d for 2018 while the production in Oklahoma has been below 1 MMcf/d. Clearly, EPSN is a junior energy producer with approximately 4,000 boepd (barrels of oil equivalents per day). But size doesn’t matter when it comes to investing.

EPSN has been running a profitable business over the last years and this is what matters at the end of the day. Specifically, it realized net income of $6.7 million during 2018 as compared to net income of $7.4 million for 2017 and 2018 adjusted EBITDA was $15.6 million. And the good news don’t end here.

Profits aside, EPSN was free cash flow positive last year given that it generated $10.1 million while development capital expenditures were approximately $1.3 million. Specifically, a total of $1.0 million was spent drilling four wells in Pennsylvania and $0.2 million was allocated to the construction and maintenance of the Auburn Gas Gathering system. $0.1 million was spent participating with minor interests in the drilling & completing of two wells in Oklahoma. Remaining capital expenditures were related to lease acquisition as well as seismic data for portions of the company’s Oklahoma property.

Production Growth, Low Key Metrics And Zero Debt In 2019

EPSN is for debt-averse investors. As of December 31, 2018, EPSN is debt-free, holds approximately $14.4 million in cash & cash equivalents and has $23 million available on its revolver. More importantly, the company will remain debt-free by year end while generating 30% YoY production growth.

On that front, the company announced last February that:

“…. it approved a $20 to $25 million capital budget for 2019, which is expected to be fully funded from operational cash flow. The Company forecasts this capital program to generate 30% growth in production. The Company has liquidity of $35 million and does not anticipate utilizing funds from its undrawn credit facility.”

To protect its cash flows in 2019, EPSN has hedged 4.8 Bcf (billions of cubic feet) of its expected natural gas volumes for the year (approximately 10 Bcfe) at an average NYMEX price of $2.83 and realized price of $2.30 net of basis.

Since it expects to fully fund its 2019 CapEx from operational cash flow, it’s safe to assume that it expects to generate at least $23 million operating cash flow this year. Based on $23 million operational cash flow in 2019, I project that 2019 adjusted EBITDA will be at least $25 million.

Given also that the Enterprise value is approximately $100 million at the current price of $4 per share, EPSN currently trades just 4 times the 2019 adjusted EBITDA.

Key Metrics: RLI And ARO

When it comes to the energy producers, it’s always prudent to check out two additional key metrics. I’m talking about the Reserve Life Index (RLI) and the decommissioning liabilities or asset retirement obligations (ARO).

Just as it sounds, RLI shows how long reserves will last at the current production rate with no additions to reserves. As of December 31, 2018, Epsilon’s total estimated net proved reserves were 119.1 billion cubic feet (Bcf) of natural gas reserves and 30,502 barrels of oil and other liquids. Given also that EPSN’s total 2018 production was 7.7 Bcf, RLI is above 15 years.

The decommissioning liabilities indicate the estimated cost of abandonment discounted to its net present value. The energy producers have to spend a portion of their operating cash flow every year to meet these obligations and return their wells to their unobstructed pre-lease condition. Typically, the required amount annually is a single-digit percentage of the decommissioning liabilities. As such, the higher the decommissioning liabilities are, the more cash is taken out of the operational cash flow every year.

That said, EPSN’s decommissioning liabilities are very low based on the daily production of approximately 4,000 boepd, as shown below:

| Decommissioning Liabilities |

|

| Balance beginning of period (December 31, 2017) | $1,646,601 |

| Liabilities from drilling of new wells | $1,590 |

| Change in estimates | $(137,490) |

| Accretion | $114,453 |

| Balance end of period (December 31, 2018) | $1,625,154 |

Buyback Program And High Insider Ownership

According to the latest annual report, EPSN bought back 143,618 shares at an average price of CAD$2.54 from March through August 2018 and continues to buy back. Proforma the recent share consolidation, this buyback price translates into approximately $3.90 per share.

Additionally, insider ownership is high with the board members owning approximately 32% of the outstanding shares and therefore, insiders’ interests are aligned with shareholders’, as illustrated below:

On that front, Mr. Lovoi, the company’s Chairman, is the Managing Partner of JVL Advisors, LLC (a private oil and gas investment advisor) and owns 20.15% of the common shares. He is also a Director of Helix Energy Solutions Group (HLX), an operator of offshore oil and gas properties and production facilities, the Chairman of Dril-Quip, Inc. (DRQ), a provider of subsea, surface and offshore rig equipment, and a Director of Roan Resources, Inc (ROAN), an Anadarko Basin-focused exploration and production company.

Strong Catalysts In The Next Quarters

Given that EPSN is new on the Nasdaq, awareness still remains low and therefore, the stock is thinly traded. However, I expect the awareness to rise in the next quarters positively affecting the stock price. Additional catalysts in 2019 include:

1) EPSN has already de-risked its Upper Marcellus interval where the well returns are approximately 70% based on $2.75 per mmbtu (millions of BTUs) flat NYMEX and therefore, it has built significant inventory for development in the next years that can meaningfully increase its current reserve value.

On that front, the company stated in the annual report:

“As we guided in February 2019, we recently turned four wells (2,600 net lateral feet to Epsilon’s interests) to sales in Pennsylvania which are currently contributing more than 5 MMcf/d net to our working interest. We anticipate exiting the first quarter of 2019 with 27 MMcf/d of natural gas production in Pennsylvania net to our working interest. Based on recent communications with the operator, we expect to spud an additional four wells (9,300 net lateral feet to Epsilon’s interests) this summer and turn the wells to sales in the fourth quarter.”

In other words, production growth from the Marcellus assets is coming soon and EPSN forecasts its capital program to generate 30% growth in production this year, as quoted above.

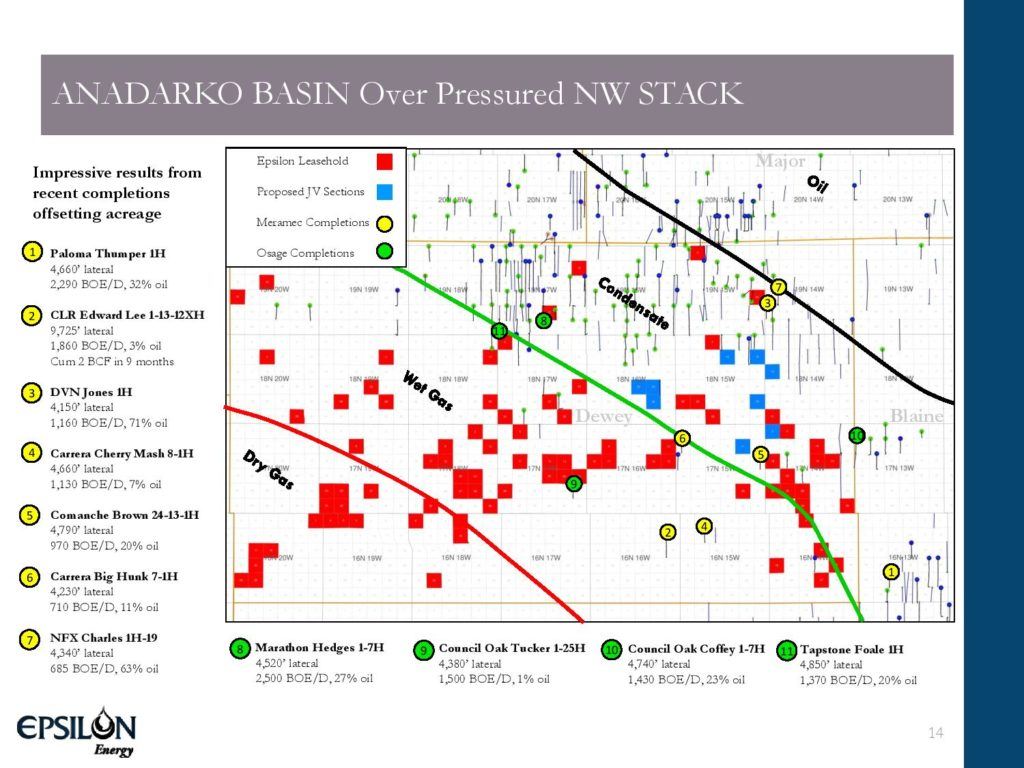

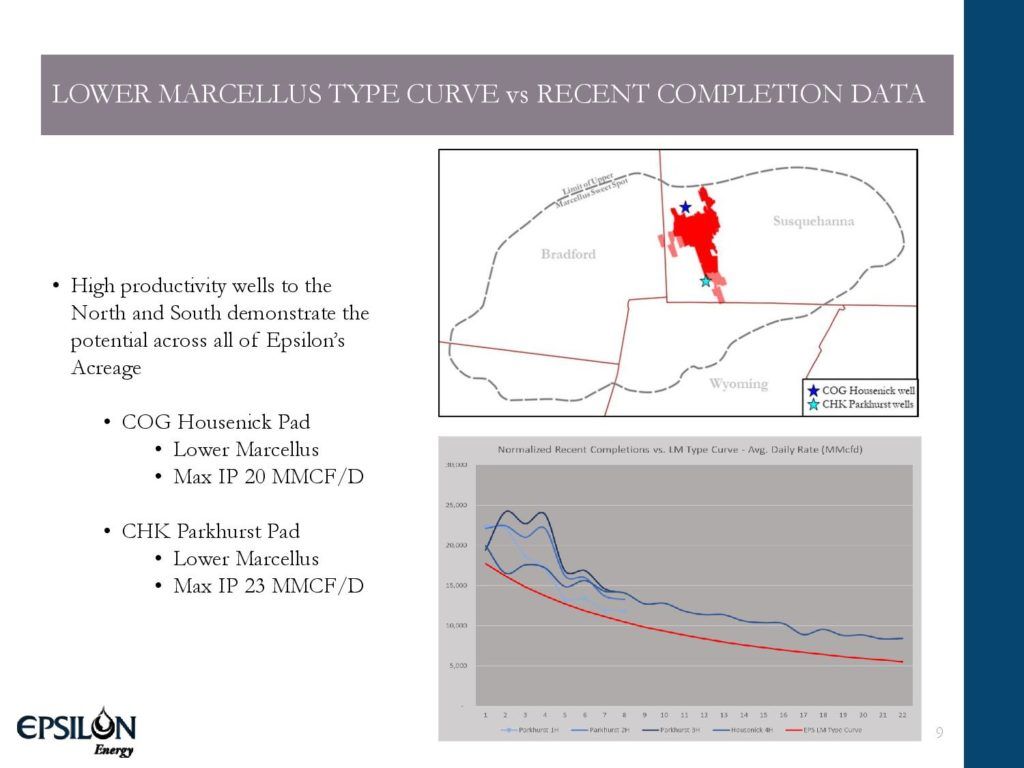

2) To-date, the company’s production has been coming solely from its Upper Marcellus wells. The Upper Marcellus wells aside, high productivity Lower Marcellus wells to the North and South demonstrate the potential across all of Epsilon’s acreage in Susquehanna County, as illustrated below:

3) EPSN noted in the recent press releases and the annual report:

“In the NW Stack, an appraisal program of three single mile laterals (5,740 net lateral feet to Epsilon’s interests) is planned to test the Meramec interval during 2019. The first well is expected to spud during Q1 2019. Following an assessment of the early performance of this group of wells, the Company will determine the feasibility of a continuous one rig drilling program throughout the remainder of 2019.”

and:

“In the NW Stack in Oklahoma, EPSN recently began drilling the first well of a three well appraisal program to test its lands for the Meramec formation.”

In other words, the first drilling results from the new land base in the Stack formation in Oklahoma are expected by the end of Q2 2019. Based on the offset analog Hz wells from DVN, CLR, ECA and privately-held energy producers, EPSN is optimistic about its first drilling results in the Anadarko Basin, stating in the latest presentation that:

“Expected well IRR’s of 50%+ at $60/bbl WTI and $2.75 per mmbtu flat NYMEX”.

4) The company’s strategy is twofold. First, it seeks to maximize the value of its Marcellus and Anadarko assets. Second, it evaluates investment opportunities in non-Marcellus petroleum basins with attractive economics at the current commodity strip.

Actually, thanks to its pristine balance sheet, EPSN is currently evaluating several projects that allow for early stage acreage acquisition at reasonable cost with meaningful development upside, as quoted below:

“Epsilon’s technical team continues to evaluate additional leasehold interests in our existing area of interest as well as attractive projects in other areas.”

and:

“The company is actively seeking bolt-on lease acquisitions”

5) The rise in natural gas production in the U.S. has significantly outpaced the development of the infrastructure necessary to transport the gas to downstream markets. This phenomenon has resulted in local natural gas prices with abnormally large differentials to the benchmark NYMEX Henry Hub. And this was the case with the Marcellus shale until 2018.

Currently, Henry Hub stands at about $2.55 per mmbtu and realized natural gas prices in the Marcellus shale have improved significantly over the last months narrowing the natural gas price differential to Henry Hub as Northeast Pennsylvania has increased transportation capacity out of the basin thanks to the recent commissioning of significant pipeline projects including Access South, Adair Southwest, Leach Xpress, Rover Phase II, and Atlantic Sunrise. These pipelines, coupled with the Cove Point LNG export facility, represent over 6 Bcf per day of incremental demand for Marcellus-Utica production.

Although natural gas prices are very volatile and will continue to largely depend on the weather, I project that natural gas price in the U.S. has limited downside and significant upside from the current price level thanks to a handful of structural factors such as the relatively low natural gas inventories as of April 26, 2019 (1,462 Bcf), the storage deficit of 316 Bcf versus the 5-year average, the growing number of LNG plants (i.e. Sabine Pass, Corpus Christi, Cove Point and Sempra Energy’s Cameron LNG, the latest milestone in the Gulf Coast’s emergence as global hub of LNG exports) and the ongoing coal-to-gas plant conversions.

Therefore, I project that rising natural gas prices in the coming months will push EPSN above the current price of $4 per share.

6) I’m a firm believer that EPSN could be a takeover target given that it holds a significant midstream asset that is resilient to natural gas price volatility and provides operational stability, while its Marcellus and Anadarko assets are adjacent to the properties of a bunch of energy producers.

Takeaway

I believe that EPSN’s current enterprise value at $4 per share grossly understates its pristine balance sheet, its operational stability and its growth prospects. Frankly speaking, my proprietary database shows that this company has the strongest balance sheet with the most attractive key metrics in the peer group with the other natural gas-weighted energy producers in North America. As such, value investors with a long-term investment horizon would be wide to consider adding it to their energy portfolio.

Disclaimer: The opinions expressed here are solely my opinion and should not be construed in any way, shape, or form as a formal investment recommendation. Value Digger does not accept any liability for any loss or damage whatsoever caused in reliance upon such information. Investors are advised that the material contained herein should be used solely for informational purposes. Investors are reminded that before making any securities and/or derivatives transaction, you should perform your own due diligence. Investors should also consider consulting with their broker and/or a financial adviser before making any investment decisions.

What is Old School Value?

Old School Value is a suite of value investing tools designed to fatten your portfolio by identifying what stocks to buy and sell.

It is a stock grader, value screener, and valuation tools for the busy investor designed to help you pick stocks 4x faster.

Check out the live preview of AMZN, MSFT, BAC, AAPL and FB.

Article by Jae Jun, Old School Value