The stock investor mantra to “invest in what you know” – popularised by legendary mutual fund manager Peter Lynch – makes sense.

[timeless]

Q2 hedge fund letters, conference, scoops etc

Until, that is, the range of companies that you “know” restricts what you invest in. Sometimes, you need to get to “know” new companies.

That’s particularly true if – like many investors in the U.S. (and elsewhere) – your portfolio suffers from a peculiar form of home country bias.

Do you have home country bias?

We’ve talked a lot about home country bias… which is the tendency of investors to fill their stock portfolio with securities from their home market. It’s why the average investor in the U.S. has almost 80 percent of his portfolio invested in domestic equities – although U.S. stocks account for only about half of global stock market capitalisation (the total value of the world’s stock markets).

It’s more extreme in Japan, which makes up just 7 percent of the world’s stock market. But Japanese investors allocate 55 percent of their portfolio to Japanese securities.

In Singapore, investors have about 39 percent of their portfolio in domestic equities – even though Singapore’s stock market is only 0.4 percent of the world’s market

That’s not diversified. Over the long term, diversification is a critical and important element of portfolio construction that improves returns and reduces risk. (Jim Rogers disagrees.)

“Neighbourhood” bias is a problem too

The evil step-sibling of home country bias is neighbourhood bias. This is when investors are focused not only on their home market – but even on those companies or sectors that are predominant within the region of their home country.

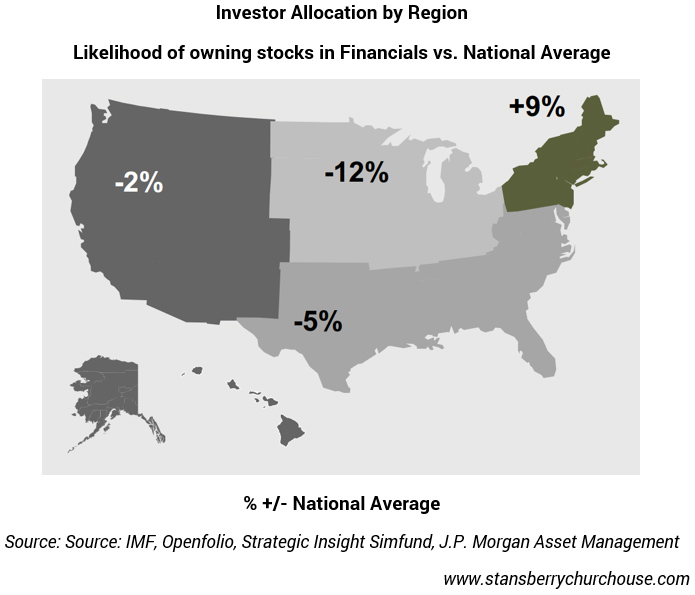

So, if I live in New York, one of the world’s biggest financial centres and home to international financial institutions like Citigroup and American Express… there’s a good chance I’ll be overweight in financial stocks. Many people who invest in the finance sector work in the finance industry, and are familiar with finance companies and their services. So it’s not surprising that they invest in what they know, understand and feel comfortable with.

In fact, investors in the northeastern United States are 9 percent more likely to hold financial sector shares in their portfolio than the average American investor, as the figure below shows.

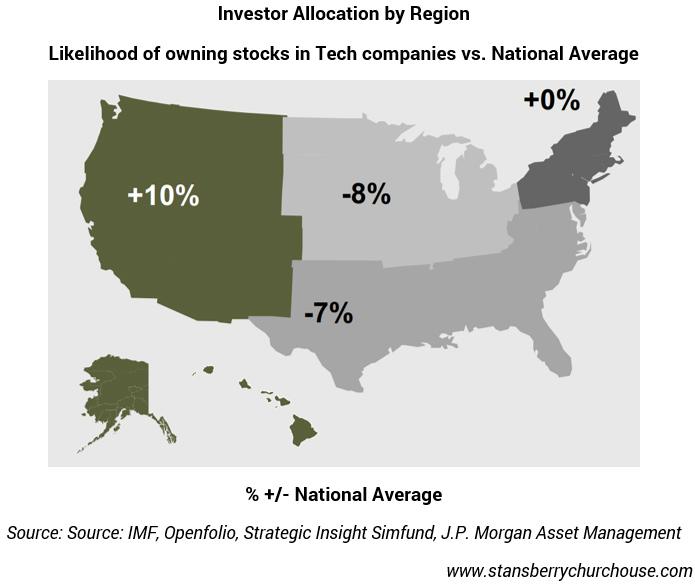

On the west coast of the U.S., investors are a little less likely than the average American investor to hold financial companies – but 10 percent more likely to hold technology stocks. That’s because California is home to Silicon Valley, the global centre of high technology, as well as world’s biggest tech companies, like Apple, Google and Facebook (not to mention thousands of start-up companies, too). Investors in this region are more familiar with tech companies – and their portfolios show it.

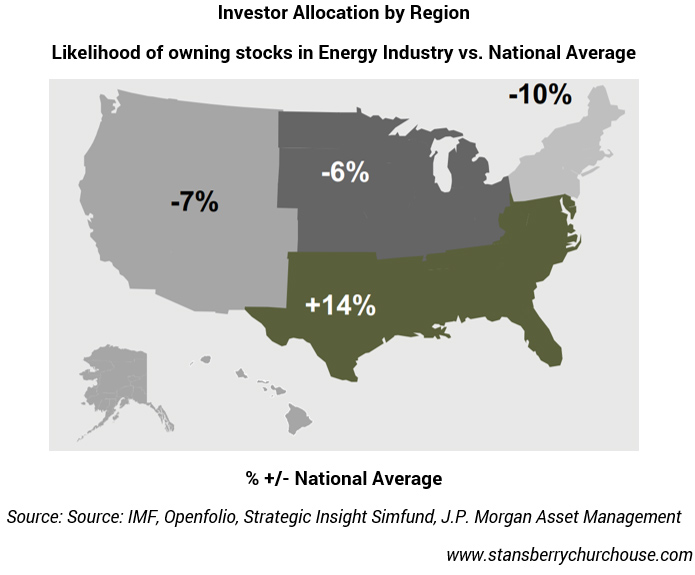

And in the southern U.S., you’re 14 percent more likely to be invested in energy than the average American (see image below). The strong presence of the oil and natural gas companies in the region results in investors loading up their portfolios with these kinds of securities. The neighbourhood bias is further heightened because many people in this area work in the sector – so they’re more familiar with them and, as a result, invest in them. People in the west, though, are a lot less likely than the average to hold energy shares.

Is this true in Asia?

Neighbourhood bias is everywhere. It’s natural to invest at home… and Asia is no different. For example…

- If you live in Singapore, is your portfolio is overweight financials or telecom stocks?

- In Hong Kong, are you over-investing in financials or technology firms?

- In Australia, you might have a higher than average exposure to mining companies.

- Indonesian investors likely are heavily weighted towards agricultural and food producers.

Local benchmark equity indices in Asian countries can be very biased towards a particular sector, too.

Even if your friendly neighbourhood sector has been performing well for a while… it won’t last forever. Sooner or later, mean reversion will come into play. So if you’re overweight in your dominant local sector, it might be time to rebalance your portfolio… to include a heavier weighting of securities from other countries and market sectors.

Good investing,

Kim Iskyan

Publisher, Stansberry Churchouse Research