Q4 hedge fund letters, conference, scoops etc

Welcome to the March 2019 issue of Hidden Value Stocks. As usual, we have two fund interviews in this issue as well as two small-cap stock ideas from each manager.

First up is Mike Melby, CFA, the founder of Gate City Capital Management. Gate manages a concentrated portfolio of deep-value U.S. micro-cap companies, and Mike talks about two of his favorite companies at the moment in the second half of the interview.

Our second interview is with Chris Colvin, the founder of Breach Inlet Capital Management. Founded in 2016, the concept of Breach Inlet is to apply the principles of private equity to an inefficient market (small caps). The firm targets companies in the $50 million to $3 billion market cap range. As well as picking out his two favorite positions, Chris also shares his view on another company we’ve previously profiled in Hidden Value Stocks, LGI Homes.

In addition to the two interviews and four stock ideas, we also have our usual fund updates.

We hope you enjoy this issue of Hidden Value Stocks, and if you have any questions or comments, please feel free to contact us at support@hiddenvaluestocks.com.

Readers can enjoy a big excerpt from this issue – to read the entire 34 page magazine or subscribe on a regular basis please visit

Sincerely,

Rupert Hargreaves & Jacob Wolinsky

Updates From Previous Issues

In the March 2017 issue of Hidden Value Stocks, Steven Kiel of Arquitos Capital highlighted MMA Capital Management LLC as one of his two undervalued small-cap picks. Here’s a snapshot of what he wrote at the time:

“GAAP book value is $21.34 as of the last quarter. Their true book value is at least $7 more because of various off balance sheet assets. I don’t have a price target, but I would feel comfortable buying it somewhere between GAAP book value and $7 above book value.”

Back then, the stock was changing hands at $22.30. It has since surged above $33 per share. Here’s an update on MMA Capital Management from Arquitos Capital’s Q4 2018 investor letter:

“Estimated book value at the end of Q4 2018 is $35.31. Shares are currently around $26 and had ended the year at $25.20. MMAC has simplified their business significantly and is now primarily a niche asset manager focused on short-to intermediate-term lending on renewable energy-related projects. The company has a large co-investment in the space and earns management and performance fees from the portfolios they manage. MMAC also has a huge pile of cash and equivalents relative to their market cap. In addition to trading at 0.7 times book value, they also trade at just 4 times trailing earnings and somewhere between 6 to 8 times estimated 2019 earnings. Finally, they continue to buy back about 10% of their shares each year. For this reason, the fact that shares trade at such a large discount to book value provides a huge benefit to us as shareholders. MMAC negatively affected the Arquitos portfolio in 2018. It is a classic example of the stock price being wholly disconnected from the reality of the company. It is our second largest holding. If I could buy more shares, I would.”

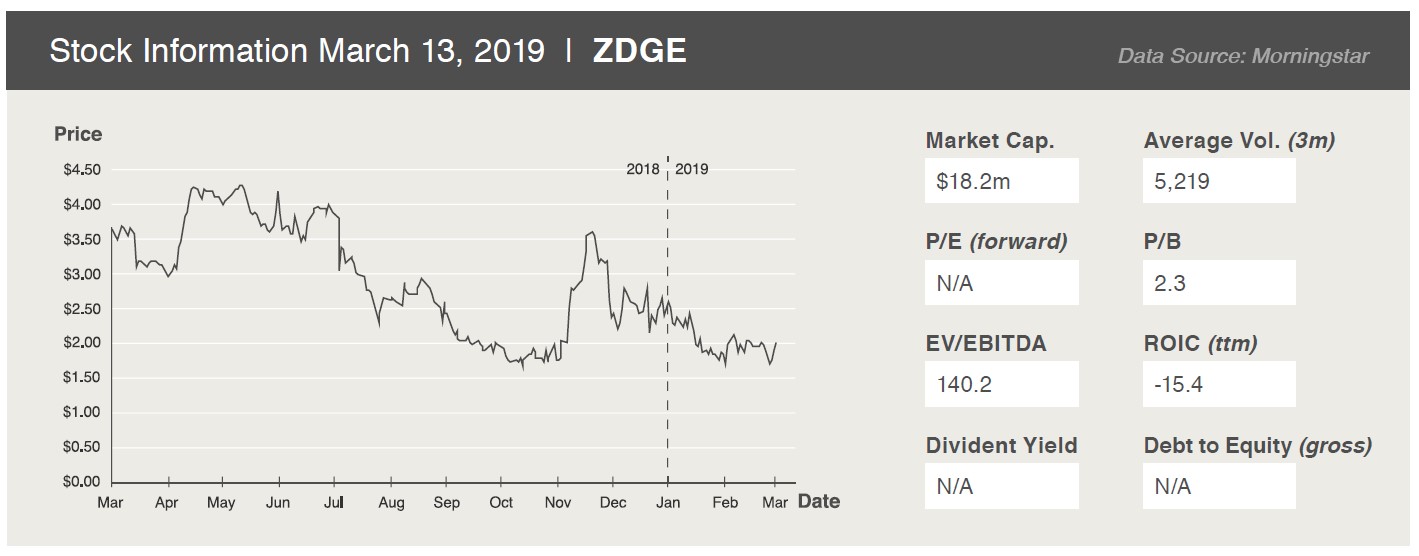

In the March 2017 issue of Hidden Value Stocks, Joseph Boskovich Jr. and the team at Old West Investment Management highlighted Zedge and Carbo Ceramics as their two undervalued small-cap picks. 12 months on and the team is still bullish on these two stocks.

Zedge

We are still very excited about Zedge. Time and time again we are reminded how much longer the incubation period is for early businesses than we originally thought. As you may recall from our original write-up, Zedge was spun off from IDT Corporation in 2016. In the past decade, Howard Jonas’ IDT has spun-off 5 public companies and sold a 6th after which it provided a special dividend to shareholders. CTM Media, now IDW Media, spun-off in 2009, Genie Energy spun-off in 2011, Straight Path Communications spunoff in 2013, Fabrix was sold to Ericson in 2014, Zedge was spun-off in 2016, and most recently, Rafael Holdings was spun-off in 2018. Had you invested in IDT Corporation at the time of its first 2010 spinoff, IDT + SpinCo’s have produced 46.3% annualized returns vs. 10.8% for the S&P 500. We believe that Howard Jonas’ SpinCo’s will continue to generate equally impressive or better returns for the foreseeable future. We own all of the spins, and we think that each has great potential, particularly Zedge and Rafael Holdings.

As you will recall in our original interview, Zedge is an early stage tech company focused on mobile device personalization and the distribution and monetization of digital content. When we first looked at the company, we were surprised to see that the app had a massive and engaged user base with over 36 million monthly active users (“MAU”), which we believed represented meaningful traction that was extremely difficult to replicate. Historically, nearly 100% of Zedge’s $12 million annual revenue was generated from the three major advertising exchanges controlled by Google, Facebook and Twitter.

What first got us excited and made us initiate an investment in Zedge was the November 2017 acquisition of Freeform Development and the retention of its co-founders. We viewed this as a major milestone for the company. In our initial interview, I dedicate a lot of time to discussing Freeform and its founders, and I urge readers to reread that interview. In early 2018, the new Zedge/Freeform team launched Zedge Premium, an exciting virtual marketplace for professional and amateur artists to monetize their content, and for the company to create ways to monetize its existing user base beyond traditional advertising.

At the time of our “Hidden Value Stocks” interview, Zedge Premium had about 100 virtual storefronts for content creators such as photographers, illustrators, designers, brands, music artists, and other types of celebrities. Today, there are about 450 artists, and Zedge Premium’s top artists have been earning more than $1,000 per month. Not bad side money for an artist or photographer!! Several big name artists are on the platform, but I think this platform provides the best value for the millions of amateur and semi-professional artists throughout the world. Now that Zedge has moved beyond invite only and has launched its self-serve artist portal, thousands of creators can launch and manage virtual storefronts of their digital content where they can share, market and sell exclusive content to Zedge’s 36 million MAU universe.

In Zedge’s most recent quarter, Zedge Premium had more than 5.7 million monetizable platform transactions and $117,000 in gross transaction value (total sales volume transacting through the platform). This was about 3x Zedge’s Q1 GTV, which we believe is impressive. However, the majority of monetizable transactions relate to watching rewarded videos, a low revenue per item mechanism. Management is heavily focused on pushing existing higher priced items like print-on-demand and Zedge’s virtual currency, and introducing new monetization into the mix like sticker packs in order to boost revenue and artist payouts.

Although we are excited about this progress, the company ultimately needs to show revenue growth and growth in revenue per monthly active user. Both metrics have been relatively flat since the spin-off of Zedge, but metrics give us confidence that the company is trending in the right direction.

Zedge just recently started to aggressively test its first foray into subscription-based revenue. Specifically, Zedge started offering its U.S. users the ability of removing unsolicited ads from the app for a fee. We are encouraged by early results as management has indicated that a decent segment of its app users are willing to subscribe and pay a fee to remove the advertising from the app. The subscription model should provide Zedge recurring revenue and with time and with more data, the subscription model should create the opportunity to start investing in paid user acquisition campaigns that yield a positive ROI, similar to what mobile gaming publishers do. Another exciting near term development will be the convergence of Zedge’s Core and Premium channels together into one unified offering. Zedge Premium was launched as its own vertical within the app product to minimize potential risk to its base offerings, allow for quick feature iteration and to efficiently develop its ecosystem. With Zedge Premium fully launched and tested, the company is ready for this next milestone.

Carbo Ceramics

Carbo has shown strong growth in their industrial and environmental segments as they continue their diversification away from pure commodity exposure in their energy business. Yet the oil price decline in Q4 2018 weighed heavily on the stock as a substantial portion of their revenue is still derived from energy-related products.

E&P operators have responded to the low commodity price environment by cutting capex budgets and renewing their focus on costs, a difficult situation for the company as they benefit from increased activity levels and operators paying more for improved performance.

While we believe the company’s diversification efforts will ultimately prove successful, the shift in price environment has extended the timeline for the overall business improvement as the legacy energy segment is still a large contributor to their financial results.

They will remain sensitive to fluctuations in energy prices (and should benefit from any positive news on that front) until which time the transformation to a more balanced company plays out and the strength of the other business lines can shine through.

Interview One: Michael Melby Of Gate City Capital Management

Michael is the Founder and Portfolio Manager of Gate City Capital Management. Before founding Gate City Capital, Michael worked as a research analyst at Crystal Rock Capital Management where he covered the consumer, restaurant, retail, and gaming sectors. Michael previously worked as an Investment Associate at the Notre Dame Investment Office where he focused on natural resources, fixed income, and risk management and as an Associate at Deutsche Bank Securities in their Debt Capital Markets group. Michael earned an MBA from the University of Chicago Booth School of Business where he graduated with honors and a BBA in Finance from the University of Notre Dame where he graduated Summa Cum Laude. Michael is a CFA Charterholder and has earned the Financial Risk Manager designation.

To start, could you give us some insight into your background and Gate’s investment philosophy?

I was born and raised in Glendive, Montana, a small town in Eastern Montana. Glendive was nicknamed the “Gate City” and the name and logo of the firm pay tribute to my hometown. As an undergrad, I attended the University of Notre Dame where I majored in finance. After my studies, I worked in fixed income at Deutsche Bank on Wall Street and then returned to Notre Dame to work for the Notre Dame Investment Office. I earned my MBA from the University of Chicago in 2011 and worked as a research analyst at Crystal Rock Capital after business school. I left Crystal Rock Capital in June of 2014 to launch Gate City Capital Management to outside investors.

Gate City Capital Management manages a concentrated portfolio of deep-value U.S. microcap companies. We look for companies that are trading at a sharp discount to their intrinsic value and that provide investors with a meaningful margin of safety through the ownership of real assets such as land, buildings, and equipment. In addition, we look for companies with clean balance sheets, understandable business models, and sustainable competitive advantages.

We complete a full due diligence process on every company before making any investment. This includes visiting with management teams and touring company facilities. We focus intently on the price paid and only look to purchase stock at a price that represents an attractive price to purchase the entire business. We have a long-term time horizon for every investment and

expect to hold each company for a minimum of two years. Finally, the Fund has a concentrated portfolio and targets between 12 and 15 total positions. This creates a portfolio of best ideas, necessitates a full due diligence process, and makes each position meaningful to the overall portfolio.

The fund has outperformed the Russell Micro-cap index by a wide margin since inception. In your opinion, what are the most prominent factors that have helped Gate achieve this outperformance?

We attribute the attractive absolute returns provided to our investors thus far to our adherence to our investment philosophy. We think by constructing a concentrated portfolio of well-researched companies with a focus on margin of safety and downside risk provides us with a unique opportunity to generate attractive returns for our investors over the long-term.

We are also committed to keeping the portfolio concentrated and restrict the size of our asset base so we can continue to enact our investment process well into the future.

Could you give our readers some insight into how you go about finding small and micro-cap ideas?

Our initial search process always starts with companies we have previously researched. We have a database of over 250 micro-cap

companies where we have completed financial models and have had an initial conversation with the management.

Rather than assigning a “buy” or a “sell” rating to a company after completing our due diligence process, we usually think the best decision is to “wait” until the company’s market valuation suggests we have limited downside risk and attractive appreciation. We continue to monitor the price and financial performance of companies we have previously researched to see if the company has now become more attractive.

In addition to monitoring prior companies, we also conduct three valuation screens on a weekly basis. We also find new companies to research while researching competitors and customers of target companies. We also attend several micro-cap conferences each year and also have built a network of like-minded investors we correspond with for idea generation.

What are you looking for in the perfect small-cap? What makes you say “yes” to a particular idea?

We look for companies with clean balance sheets, owned assets, and understandable business models. We utilize a discounted cash flow analysis to generate a target intrinsic value for each company we research.

We also complete a floor value analysis to approximate what the business would be worth in a liquidation-type scenario. We look for companies with little (or no) downside to our floor value with at least 50% upside to our target value.

And what about management? What qualities are you looking for in managers?

We look for intelligence, integrity, and work ethic when evaluating management teams. We find that in-person meetings are very helpful in assessing these characteristics in our management teams. We also look for an alignment of interests with shareholders through insider share ownership.

Are there any particular red flags you are looking for when evaluating a company?

We attempt to avoid companies where there is a lack of alignment with shareholders. We also generally avoid companies with levered balance sheets. If a company does have debt, we want the company to have both the ability and willingness to pay down the debt with free cash flow.

Moving back to portfolio management. You said Gate City’s portfolio tends to be relatively concentrate so how do you get comfortable owning just a few key positions and how do you go about minimizing risk?

We think risk starts at the position level. We attempt to not lose money on any investment by investing only in companies that have a significant margin of safety from having both a clean balance sheet and a portfolio of owned assets. While this does not eliminate risk from our portfolio, we believe building a portfolio from companies with little downside risks helps reduce risk for the overall portfolio.

Do you have an example of a company that initially looked attractive, but later turned out to be a poor fit for your portfolio?

Without discussing specific companies, in our diligence we have found situations that have caused us to question the quality of a portfolio company’s management team. In these cases, we will look to exit our position in the company.

Furthermore, are there any particular sectors or industries you avoid outright in the small-cap space?

We tend to avoid tech and biotech companies due to the lack of owned assets and our lack of tech expertise. We also generally avoid financial companies due to the leverage they utilize and the trouble we have in understanding their asset base.

Read more right here

This article ends above