Investors in corporate bonds are bracing for more trouble after getting hammered by rampant inflation and rising yields in the first quarter.

Q4 2021 hedge fund letters, conferences and more

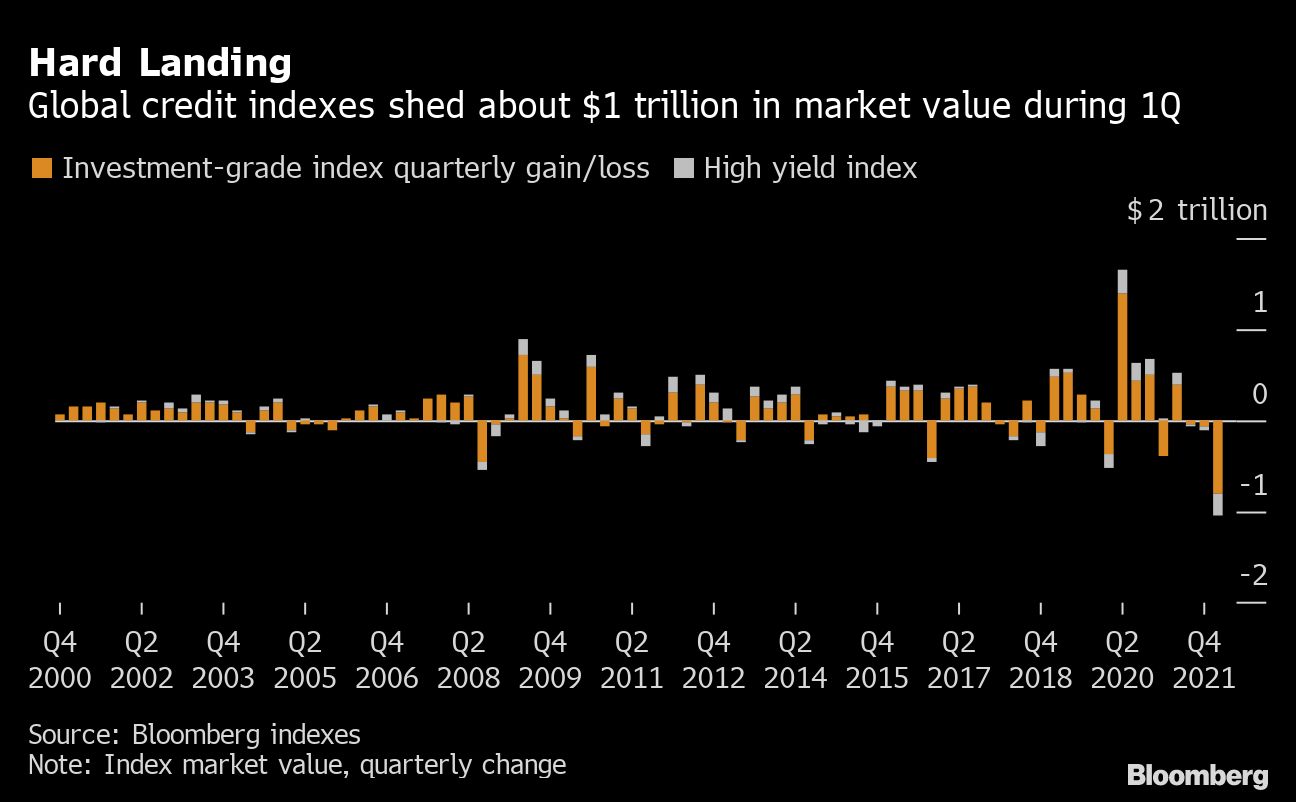

The worldwide pool of the safest corporate debt has shrunk by $805 billion this year, while the global junk market lost $236 billion, according to data compiled by Bloomberg. That’s the biggest dollar decline since records began over 20 years ago, following a borrowing binge propelled by record-low funding costs.

The slump marked the biggest total return loss for high-grade bonds since Lehman Brothers’ collapse, and the worst junk performance since the start of the pandemic. The U.S. investment grade market alone saw about $440 billion in market value erased and is on track for the biggest three-month slump since 1980.

Credit remains under pressure from inflation, which is pushing central banks to boost rates, in turn risking an economic slowdown. That’s causing plenty of angst for investors.

“We are far enough from the inflation picture being clear that you can’t help but think that volatility will persist,” said Brad Rogoff, head of global FICC research at Barclays Plc, in an interview.

Meanwhile, Russia’s invasion of Ukraine has increased concerns about Europe’s ability to fulfill its energy needs and is further disrupting already struggling supply chains around the world.

“We’ve really got a lot of things we have to contend with,” said April Larusse, head of investment specialists at Insight Investments, which oversees 867 billion pounds ($1.14 trillion). Given that “there can be endless talk and quite little progress” between Russian and Ukrainian negotiators, “it’s probably unwise to put a large directional bet.”

As losses racked up, retail investors yanked cash from bond funds. Outflows are likely to intensify, as they tend to lag returns by about a month, Bank of America Corp. strategists wrote in a note Tuesday.

A recent BofA survey found that inflation is the number one concern among credit investors right now, followed by geopolitical risk. Investors “remain bearish,” BofA credit strategist Yuri Seliger wrote.

Ukraine Outlook

Skeptical NATO allies are evaluating whether Russia’s promise to scale back military operations in Ukraine marks a turning point in the conflict or simply a tactical shift. Hopes for progress in negotiations helped bring spreads in global high-grade debt below levels last seen before Russia’s invasion of Ukraine on Feb. 24. Morgan Stanley’s U.S. and European credit strategy chief warned this could prove a blip as focus shifts to central bank hawkishness.

Losses have been coming from all sides, especially in the high-grade market, which is more exposed to the global rise in government bond yields as central banks tighten policy. This is due to their higher duration, bond parlance for price sensitivity to changes in interest rates.

Yields on 10-year U.S. Treasury and German government bonds have surged to their highest levels since 2019 and 2018 respectively. U.S. two-year yields briefly exceeded the 10-year level on Tuesday for the first time since 2019, signaling that rate increases by the Federal Reserve could trigger a recession.

Meanwhile, corporate bonds’ risk premium above supposedly safe debt has also jumped this year. While spreads reversed some of their widening in recent weeks, analysts expect pressure to resume.

In Europe, bonds indicated at a discount to face value now account for two-thirds of the euro high-grade market from about a quarter at the end of 2021, based on data compiled by Bloomberg.

Persisting Risks

Still, what looks cheap now can get even cheaper later, especially as the risks that have driven first-quarter losses look set to persist.

“Twelve-month forward excess return expectations from current levels are historically good,” said Greg Venizelos, a credit strategist at Axa Investment Managers, which oversees 887 billion euros. “This doesn’t mean there is no further downside — it’s a good entry point but could get even better in the weeks ahead. It’s prudent to stay a bit cautious.”

To be sure, sharp price drops have allowed some investors to scoop up what they regard as bargains at spread levels not seen since the start of the coronavirus pandemic.

“We view investment-grade in dollars as a strong buying opportunity, probably the best opportunity in the current environment if we think in terms of risk-adjusted expected returns,” said Eric Vanraes, a portfolio manager at Eric Sturdza Investments, which oversees $1.7 billion.

“The widening of spreads has been amplified by poor liquidity,” Vanraes said. “It will improve when people like us seize the opportunity and become buyers of the asset class.”

Elsewhere in credit markets:

Americas

Four issuers are selling new U.S. high-grade bonds, including Workday Inc. and DT Midstream Inc.

- Churchill Downs Inc., owner and operator of the racetrack that hosts the annual Kentucky Derby, is tapping the U.S. high-yield bond market for $900 million to help finance its asset purchase of Hard Rock Sioux City-owner Peninsula Pacific Entertainment LLC

- Russian default fears ebbed further as the government’s latest interest payment started to show up in some bond investors’ accounts

- For deal updates, click here for the New Issue Monitor

- For more, click here for the Credit Daybook Americas

Read the full article here by Tasos Vossos, Hannah Benjamin, Jack Pitcher, Advisor Perspectives.