Key highlights for August:

Q2 2020 hedge fund letters, conferences and more

- Global hedge funds recorded their best five-month performance of 12.85% in August after they suffered from their worst quarterly performance of 8.02% in Q1 2020. In terms of year-to-date return, the Eurekahedge Hedge Fund Index was up 3.79%, with around 22.5% of hedge funds managers posting double-digit returns over the first eight months of the year.

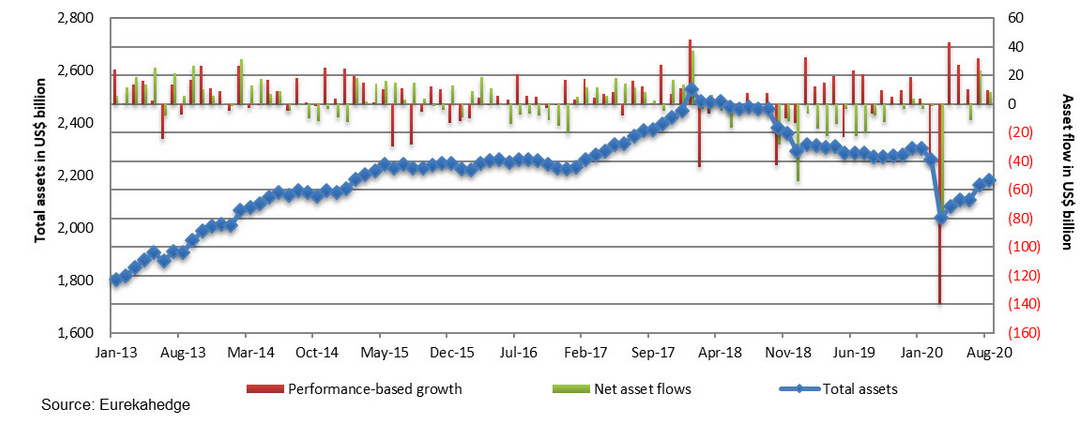

- Assets under management for the global hedge funds industry have rebounded, increasing by US$142.8 billion over the five-month period ending August 2020. This has come from performance driven gains of US$122.5 billion and net investor flows of US$20.3 billion. This marks a sharp recovery following US$264.1 billion asset decline in Q1 2020.

- The Eurekahedge North American Hedge Fund Index was up 2.39% during the month, bringing their five-month trailing return to 15.74% since end-March, which marks the best five-month performance of the index since inception. In contrast, their European counterparts as captured by the Eurekahedge European Hedge Fund Index generated 10.12% return over the five-month period ending month of August.

- The Eurekahedge Greater China Long Short Equities Hedge Fund Index was up 1.94% in August, bringing their five-month performance to 28.33% since end-March. In the same vein, the total AUM of the region also grew by 31.3% since end-March from US$38.5 billion to US$50.5 billion, primarily driven by performance-based growth which accounts for US$11.2 billion from its total increase of US$12.0 billion.

- The Eurekahedge Long Short Equities Hedge Fund Index was up 2.87% in August, bringing its year-to-date return to 4.97%. More than half of its constituents have outperformed the MSCI ACWI (Local) and around 26.7% of them generated a double-digit return over the first eight months of the year.

- The Eurekahedge Macro Hedge Fund Index was up 1.23% in August, bringing its year-to-date return to 6.01%. Macro hedge funds exhibited a strong comeback from their worst quarterly performance in Q1 2020 as seen from their five-month trailing return of 9.72% since end-March, which was their best five-month performance since 2003.

- Hedge funds utilising structured credit strategies were up 2.16% during the month, extending their five-month trailing return to 15.82% since end-March as captured by the Eurekahedge Structured Credit Hedge Fund Index . The Fed adopted a new framework called ‘average inflation targeting’, which is expected to result in keeping its policy rate lower for a longer period that may support the fund manager’s future performance.

- Fund managers focusing in cryptocurrencies were up 8.70% over the month, outperforming Bitcoin’s performance with its 4.84% return. In terms of year-to-date return, the Eurekahedge Crypto-Currency Hedge Fund Index was up 65.88% as of August 2020 compared to the 60.76% of Bitcoin over the same period, while the top three performing funds of the index generated a year-to-date return in excess of 110%.

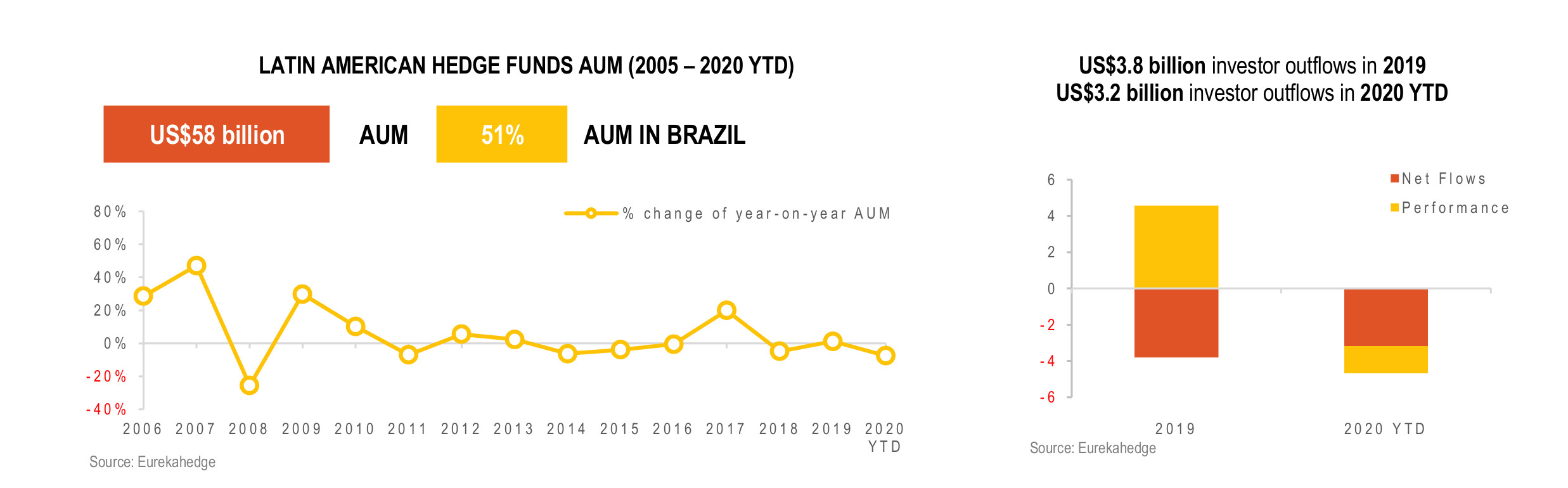

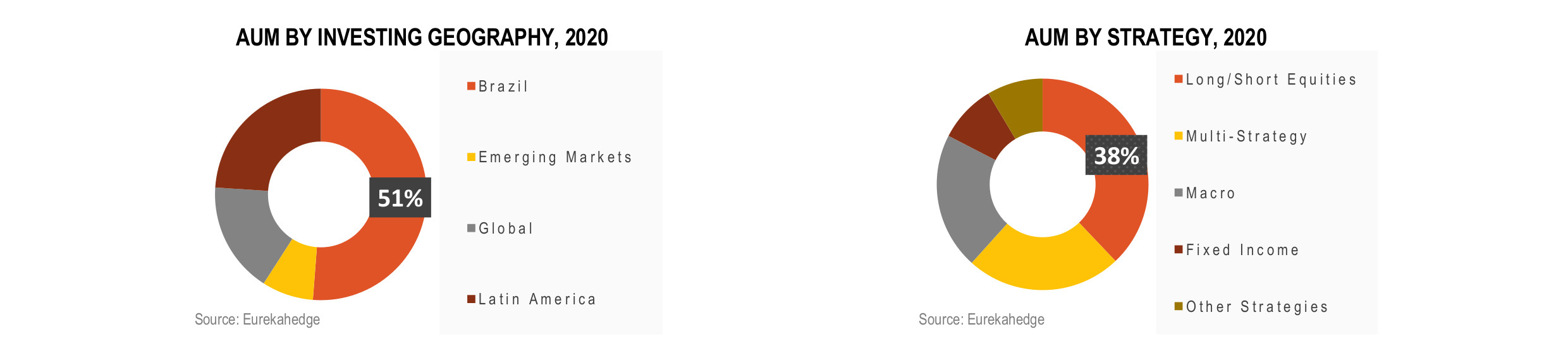

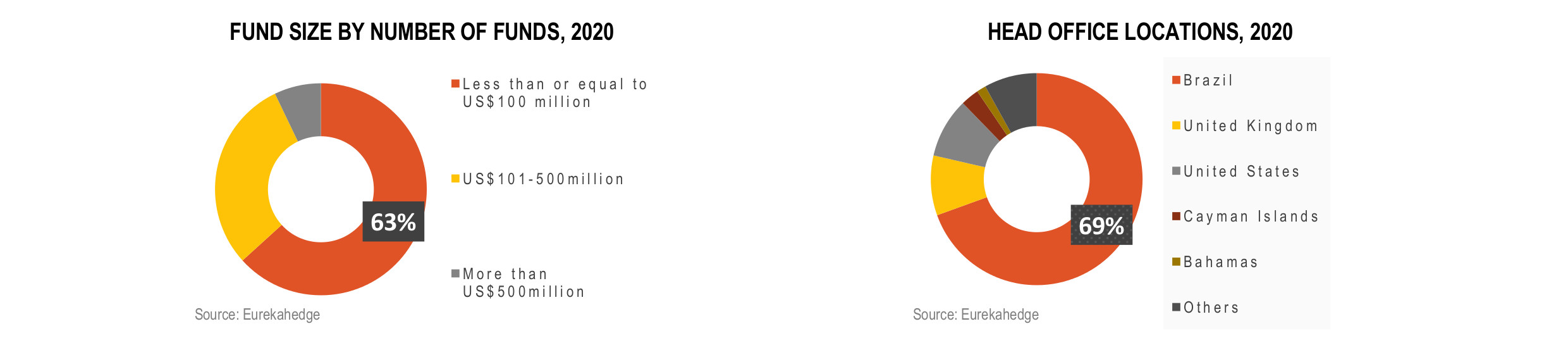

Key Trends in Latin American Hedge Funds

The Eurekahedge Hedge Fund Index was up 1.85% in August, bringing its year-to-date return to 3.79% and its five-month trailing return to 12.85% since end-March. The robust performance of the global equity markets on the back of the encouraging development of the COVID-19 vaccine and improving macroeconomic data supported hedge fund managers’ performance. In the US, the declining daily COVID-19 cases on top of the Fed’s new inflation targeting framework boosted the region’s equity market. The tech-heavy NASDAQ recorded the strongest return of 9.59%, while the S&P 500 was up 7.20% in August. The Fed shifted its approach to inflation to ‘average inflation target’ aiming to achieve an average inflation rate of two percent over time, which were expected to result in keeping the interest rates lower for an extended period. In the same vein, European equities were also up, with DAX and CAC 40 up 5.13% and 3.42% return throughout the month respectively. Over in Asia, despite PM Shinzo Abe’s resignation that sent the market lower, the Nikkei 225 ended the month up 6.59%. The drop in stock prices was short-lived as investors expected that the next administration would continue the current economic policies. Returns were positive across geographic mandates in August with fund managers focusing on Japan up 4.28%, outperforming their Asia ex-Japan and North American peers who were up 3.15% and 2.39%, respectively. Across strategies, long/short equities, event driven and relative value fund managers were up 2.87%, 2.36% and 1.96% respectively throughout the month.

Roughly 74.1% of the underlying constituents of the Eurekahedge Hedge Fund Index posted positive returns in August, and 22.5% of the hedge fund managers in the database were able to maintain double-digit returns over the first eight months of 2020.

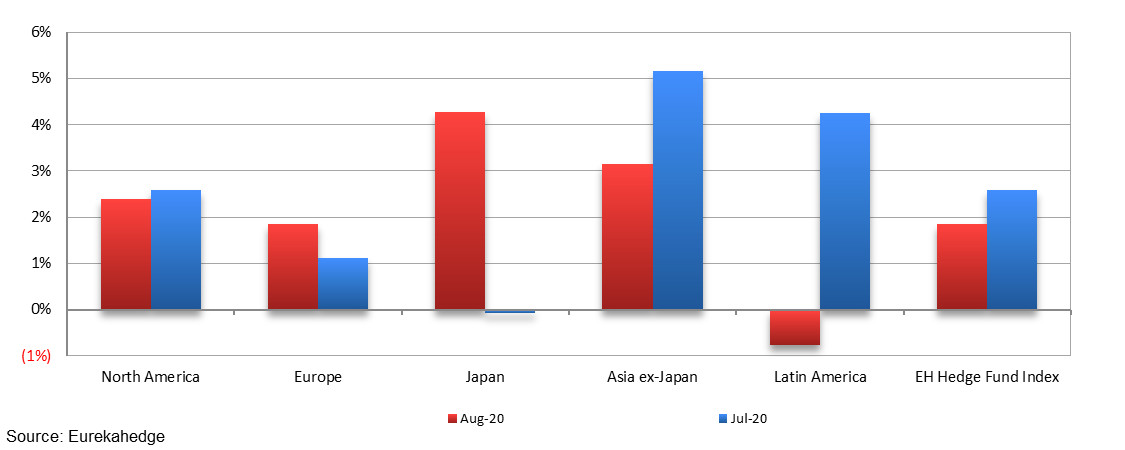

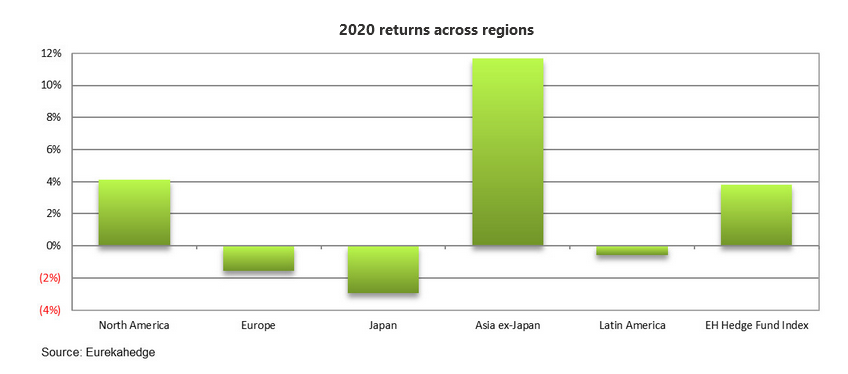

Figure 2 illustrates the 2020 performance of hedge fund managers across regions. Most regions were still down over the first eight months of the year, attributed to the spread of COVID-19 which resulted in the massive sell-off in risk assets in the earlier months of the year. Supported by the strong performance of Chinese equities, Asia ex-Japan hedge funds led the pack with their 11.69% return – followed by North American hedge funds who were up 4.13% as of August 2020. On the other hand, Japanese and European hedge funds underperformed the group as they were down 2.96% and 1.54% respectively.

2020 returns across regions

Eurekahedge Asset Weighted Index

The Eurekahedge Asset Weighted Index – USD was up 1.59% during the month, reducing its year-to-date loss to 0.55% over the first eight months of 2020. The strong performance of the equity market and weak USD dollar supported the index performance. It should also be noted that the Eurekahedge Asset Weighted Index is US dollar denominated, and during months of strong US dollar gains, the index results include the currency conversion loss for funds that are denominated in other currencies.

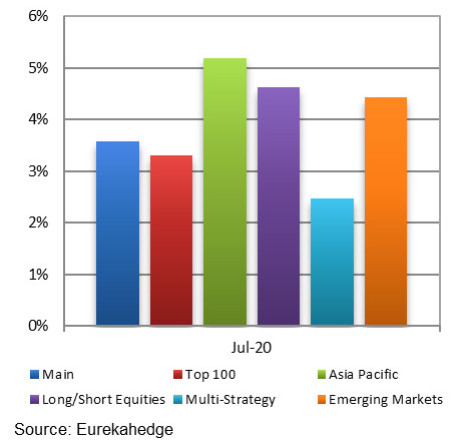

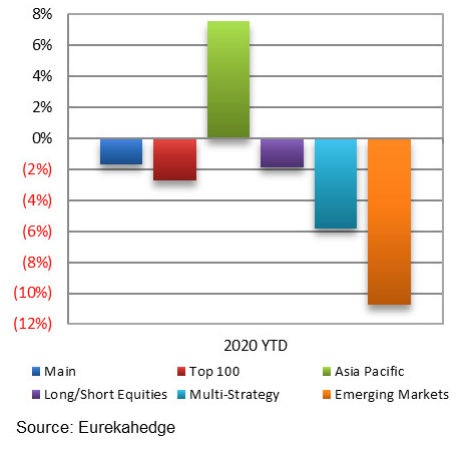

All of the Eurekahedge asset-weighted indices were mostly up in August, with the Eurekahedge Long Short Equities Asset Weighted Index posting the strongest return of 3.26% driven by the strong performance of the global equity market throughout the month. The underlying Asia Pacific Index was also up 1.66% in August. In terms of year-to-date return, Asia Pacific mandate was up 9.27% outperforming its asset weighted peers over the first eight months of 2020.

| Eurekahedge Asset Weighted Indices August 2020 returns  |

Eurekahedge Asset Weighted Indices 2020 returns  |

CBOE Eurekahedge Volatility Indexes

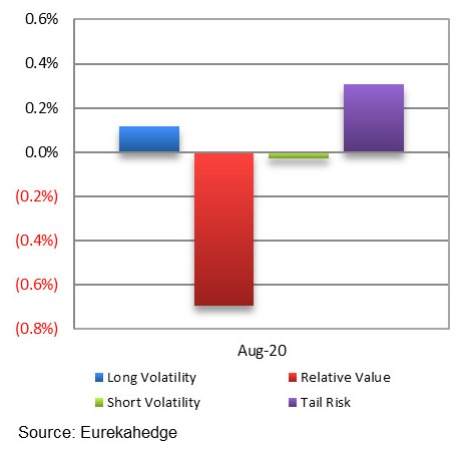

The CBOE Eurekahedge Volatility Indexes comprise four equally-weighted volatility indices – long volatility, short volatility, relative value and tail risk. The CBOE Eurekahedge Long Volatility Index is designed to track the performance of underlying hedge fund managers who take a net long view on implied volatility with a goal of positive absolute return. In contrast, the CBOE Eurekahedge Short Volatility Index tracks the performance of underlying hedge fund managers who take a net short view on implied volatility with a goal of positive absolute return. This strategy often involves the selling of options to take advantage of the discrepancies in current implied volatility versus expectations of subsequent implied or realised volatility. The CBOE Eurekahedge Relative Value Volatility Index on the other hand measures the performance of underlying hedge fund managers that trade relative value or opportunistic volatility strategies. Managers utilising this strategy can pursue long, short or neutral views on volatility with a goal of positive absolute return. Meanwhile, the CBOE Eurekahedge Tail Risk Index tracks the performance of underlying hedge fund managers that specifically seek to achieve capital appreciation during periods of extreme market stress..

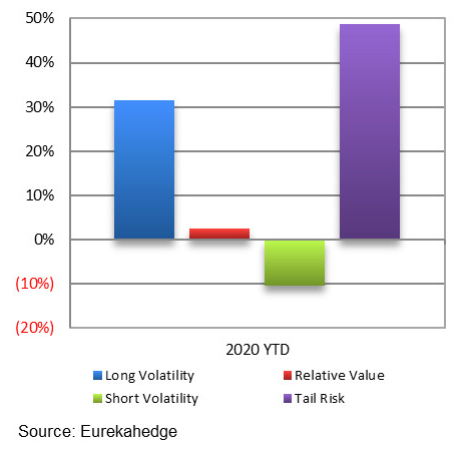

The CBOE Eurekahedge Volatility Indexes ended the month of August with mixed returns, with tail risk hedge funds gaining 0.31% and relative value volatility hedge funds losing 0.69% throughout the month. On the other hand, long and short volatility finished the month in flat. In terms of year-to-date returns, the CBOE Eurekahedge Tail Risk Volatility Hedge Fund Index topped the chart with its 48.63% return, while the CBOE Eurekahedge Short Volatility Hedge Fund Index was down 10.47%, placing them last among the four volatility strategy categories.

| CBOE Eurekahedge Volatility Indexes August 2020 returns  |

CBOE Eurekahedge Volatility Indexes 2020 returns  |

Summary monthly asset flow data since January 2013

Launched in 2001, Eurekahedge has a proven track record spanning over 16 years as the world’s largest independent data provider and alternative research firm specialising in global hedge fund databases and research. The global expertise of our research team constantly adapts to industry changes and needs, allowing Eurekahedge to develop and offer a wide array of products and services coveted by institutional investors, family offices, accredited investors, qualified purchasers, financial institutions and media sources. In addition to market-leading hedge fund databases, Eurekahedge’s other business functions include hedge fund research publications, due diligence services, investor services, analytical platforms and risk management tools.