FORECASTS & TRENDS E-LETTER

by Gary D. Halbert

January 22, 2019

Q3 hedge fund letters, conference, scoops etc

IN THIS ISSUE:

- Overview & A Great Free Offer

- Gloom & Doom Abounds, But Facts Don’t Support It

- On Jobs, Wages & Worker Productivity

- On Housing, Inflation & the Fed Funds Rate

- Conclusions: Slower But Solid Growth in 2019

Overview & A Great Free Offer

Today, I’m going to introduce you to an economist I have read for years. His name is Richard F. Moody. He is the Chief Economist at Regions Financial Corporation (Regions Bank) headquartered in Birmingham, Alabama. Regions is the largest bank in the South with almost 1,500 branches spread across the southeastern US and the Midwest. It has over $125 billion in assets and employs over 21,000 people, with Richard and his economics team among them.

I enjoy Richard’s work, not only because he’s a good economist, but also because he doesn’t write like one. His reports are easy to read and he gets to the point quickly. What I like best is the fact that he and his team track all of the important economic reports that are released each week, and they send a brief e-mail summary just after the reports come out with their analysis.

Periodically throughout the year, they send out timely special reports covering whatever they deem important at the time. And each January, they send out a detailed and specific forecast for the New Year. I’m going to summarize their latest 2019 economic outlook below.

I also like the fact that Richard and his team are not “perma-bulls” or “perma-bears” – they just call it as they see it. I should add that while Richard and his fellow economists are good at what they do, they are not always right – no economist is – and when they’re wrong, they are quick to admit it and tell you why.

The good news is, I have arranged for my clients and subscribers to receive Richard’s public analysis and forecasts free of charge! All you have to do is send Richard an email at richard.moody@regions.com and mention my name. You’ll then start receiving their emails on the important economic reports each week and their periodic special reports.

By the way, Richard and his team won’t sell you anything and won’t share your email address with anyone. In case you’re wondering, I don’t make a penny off of this. So, if you’re interested, give it a try. If you don’t find it useful, you can opt out at any time.

Now let’s get on to my summary of their latest economic outlook which is entitled: “2019 Economic Outlook: Gloom, Despair, Agony… And Above-Trend Growth.” It’s way too long to reprint, but I’ll give you the highlights below.

Gloom & Doom Abounds, But Facts Don’t Support It

Richard begins by pointing out the obvious, that the investment public has fallen into a very sour and worried state given the very volatile sharp retreat in stocks in the 4Q. This, plus fears of a trade war with China, higher interest rates and the hyper-negative media have left most investors wondering if there really will be another financial crisis and recession this year.

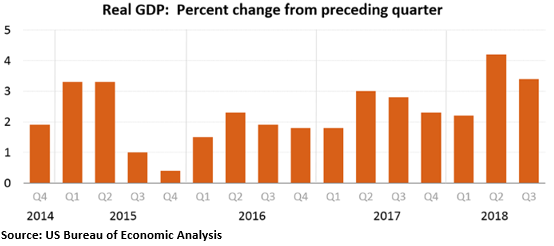

The irony, Richard points out, is the likelihood that 2018 will go down as the best year of economic growth in the current recovery, now in its tenth year; if it endures until July, it will be the longest economic recovery on record. While we don’t have the first 4Q GDP estimate yet, Richard is looking for a number around 3.0% on January 30.

If that is the case, then GDP growth in 2018 will have been 2.9% (subject to upcoming revisions in February and March). That compares to Richard’s original GDP estimate of 2.8% at the beginning of last year. If 2018 does end as Richard & Co. expect with growth of 2.9%, that would put average annual real GDP growth over the life of this expansion at 2.25%.

As for 2019, Richard’s team believes the recovery will continue but not quite as fast as in 2018. Their estimate for GDP growth this year is 2.6%. They expect the economy will continue to be driven by strong consumer spending, business investment and government spending, while residential investment will remain on the weak side. On the odds of a recession this year:

“Simply put, an awful lot would have to go wrong for the U.S. to slip into recession in 2019, and while the probability of recession rises once we get to 2020, that is not a foregone conclusion.

In other words, 2019 should prove to be another year of solid growth for the U.S. economy. While there are clearly downside risks, it helps to consider all that the economy has going for it as we start out the new year. The pace of job growth accelerated in 2018, pulling the jobless rate below 4.0 percent and pushing wage growth to a cycle-high, which helps account for consumer confidence hovering near an almost two-decade high.

Though having slowed in late-2018, business investment spending is still in a good place and, while margins will be slimmer in 2019, corporate profits aren’t going to simply evaporate.

Finally, there is still a high degree of fiscal stimulus in the pipeline in the form of higher federal government spending. So, even if real GDP growth falls short of our forecast (2.6%), it should still be above potential (2.0%) in 2019.”

As for the outlook for 2020, Richard & Co. expect the economy will be losing momentum in the last half of this year, and will continue into 2020. The question is, by a little or a lot? The answer to that question lies, they believe, in how many major uncertainties get worked out this year.

“We think that by Q4 2019, fading fiscal stimulus and the cumulative effects of tightening financial conditions will begin to weigh on real GDP growth, and if we are correct on this point it sets up a marked deceleration in growth in 2020.

Given how much uncertainty looms over trade policy, monetary policy, inflation, and the political landscape, and given how quickly things can change, 2020 seems a long way off. For now, though, we continue to expect another solid year of economic growth in 2019.”

From this point on, I will very briefly discuss the other high points in Region’s 2019 Outlook.

On Jobs, Wages & Worker Productivity

The US economy produced a whopping 2.6 million net new nonfarm jobs last year, the most since 2015. Richard’s team expects job growth to slow somewhat this year, especially in the second half. They forecast the economy will produce just over 2.0 million jobs in 2019. Despite the December blowout jobs report, which showed 312,000 new jobs last month, Richard & Co. look for monthly job creation to drop off this year for a variety of reasons I may go into in an upcoming E-Letter.

Wages, or average hourly earnings, rose 3.2% (annual rate) in the 4Q, the best rate in years. Richard’s team expects this trend to continue in 2019, but not nearly as much as many other forecasters. Instead, they see the growth rate stabilizing below 3.5% in second half 2019.

Another important factor in the jobs market is the nonfarm labor productivity rate. While the data for December is not available yet, it looks like growth in productivity rose 1.3% last year. That’s an improvement over 2017 but is still an anemic number. Richard & Co. forecast productivity to rise to 1.6% this year but remind us that is still a weak reading.

On Housing, Inflation & the Fed Funds Rate

The sluggish US housing market was probably the biggest surprise of 2018. Through November, housing starts were down to an annualized rate of 1.264 million units. Richard’s team believes the housing market will not do any better this year. They cite the usual culprits for the weakness: higher mortgage rates and house price appreciation.

For measuring inflation, Richard prefers the Core Personal Consumption Expenditures Index (PCE). Through November, the core PCE increased 1.9% last year and was trending higher. Richard & Co. believe that number will rise to 2.2% or a little higher by year-end. While this increase is not by itself alarming, it will certainly get the Fed’s attention.

The Fed hiked rates four times last year with the Fed Funds range at 2.25-2.50% at year-end. As I discussed last week, the Fed has indicated it may only be looking at 1-2 rate hikes this year. Richard & Co. believe there is a good chance the Fed will not raise rates in the first half of 2019. With the Fed’s latest “wait and watch” language, I don’t disagree.

Conclusions: Slower But Solid Growth in 2019

While Richard & Co. expect the economy to slow down more this year, they still expect GDP growth of 2.6% in 2019. They believe the growth in net new jobs will slow this year to around 2 million. They expect wage growth to continue to rise but to cap-out below 3.5%. They believe the housing market will remain soft this year and housing starts will do well to match year.

The summary above hardly scratches the surface of Region’s latest 2019 Economic Outlook. There are so many facts and analysis I could not go into. That’s why I encourage you to sign up to receive all of Richard’s analysis and forecasts free of charge at richard.moody@regions.com. Just send him an e-mail and mention my name.

Alpha Advantage Webinar Recording Available

On January 17 we had the opportunity to visit with Paul Montgomery, the Trading Manager for the HWM Alpha Advantage strategy. Paul explained how Alpha Advantage works and showed its impressive performance results. A recorded version of this webinar is now available on our website for you to watch at your convenience.

The beauty of Alpha Advantage is that it can make money whether the markets go up or down because the strategy invests both long and short. No matter what happens going forward, you have the potential to make money, even if the markets tank.

I definitely think you should give Alpha Advantage a serious look, especially if you are searching for a program that can do well no matter whether the markets are going up or down. The minimum investment is only $50,000 and all accounts are held at Guggenheim.

Call us today at 800-348-3601 with any questions, or if you would like more information. Our experienced Investment Consultants can help you determine if this investment or our other actively managed and non-correlated investments are a fit for your portfolio and investment goals.

Wishing you profits,

Gary D. Halbert

SPECIAL ARTICLES

IMF Cuts World Economic Growth Forecast

Richard Moody: Existing Home Sales Weak, A Sorry End to a Down Year

Trump Flips Tables on Pelosi – Now She Owns Govt. Shutdown

Gary’s Between the Lines Blog: Despite Negative Media, There’s Much to Be Optimistic About