GreenWood Investors commentary for the fourth quarter ended December 31, 2020.

Q4 2020 hedge fund letters, conferences and more

Dear GreenWood Investor:

We continue to be encouraged by the progress we made in the fourth quarter. Performance net of all fees and expenses was +16.4% in the Global Micro fund, +9.2% in the Euro-denominated Luxembourg fund, +18.5% in the Global Micro accounts, and +24.2% in the Traditional accounts. This compares to the MSCI ACWI benchmark of +15.8%. We’ve made a deliberate and intentional decision to stay very conservative in this frenzied market which has more daily antics than a Barnum & Bailey circus. Our short positions have taken away some of the momentum that our portfolio has built throughout the Covid-19 recovery. Since inception of the Global Micro Fund in early 2014, which is when we started shorting individual securities as opposed to indices, our short book has only taken away 1.3% per year from absolute performance, but with most of this coming in the fourth quarter.

We continue to be very engaged and active on short-diligence and have built a portfolio of modestly sized positions to ramp up as we gain conviction that reason will once again return to US markets. Furthermore, throughout the year we have consistently trimmed positions to avoid any portfolio leverage. This is not a time to be reaching for returns via aggressive portfolio tactics in our opinion.

Performance in the fourth quarter has restored our long-term, through the cycle, track record nearly back to 7.5% (7.4% actual) compounded annual out-performance, which we view to be a minimum acceptable level rather than a goal. In a year where benchmark earnings shrank, our portfolio on a weighted adjusted basis was able to grow EBITDA considerably. So while the financial performance exceeded even the S&P 500, much of the investment performance was driven by companies graduating to a more favorable market narrative for the growers while the value and turnaround portfolio de-rated despite posting largely resilient performance.

While we remain encouraged by the out-performance, we are very far from satisfied given our full year performance hovered uncomfortably close to the benchmark (+9.3% Global Micro Fund, +26.6% Lux fund, +14.9% Global Micro accounts, +21.3% in Traditional accounts). Because of the numerous funds we now manage, the co-investment, the global micro fund, the traditional separate accounts, and now a Luxembourg fund, all based in different currencies and having slightly different mandates, we’ve added more detailed reporting in our Results page so that you’re going to see the realized performance of your investment rather than a complex table of all the different strategies.

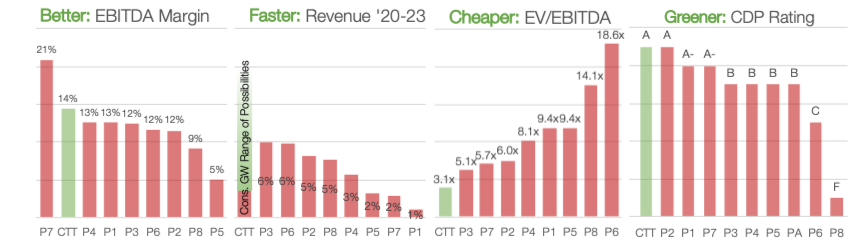

Better, Faster, Cheaper, Greener

“You measure success when your competitors squirm.” -Sir Martin Sorrell

The one area that remains considerably dissatisfying for us is the performance of CTT in the co-investment fund. While it remains frustrating, the sense of urgency remains very high for us to finish the playbook we started out to achieve. We know the reason for this under-performance and understand the market’s concerns. We also have a high degree of conviction that it will not only be rectified in the quarters to come, but that the progress achieved will be considerably surprising. Borrowing the mantra from another portfolio position we have, S4 Capital (SFOR LN), CTT is better, faster, cheaper and greener than its peers. It is cheapest in class based on EBITDA, has the fastest forward-looking revenue and profit growth runway, has the second highest EBITDA margins in the industry, and has the highest environmental rating in its industry, according to the Carbon Disclosure Project climate change rating.

Exhibit 1: CTT Equity Story from Our Perspective

Note: figures use CapIQ 2020 consensus except revenue (our estimates). Peers: POST AT, PNL NL, BPOST BE, DPW GR, RMG LN, PST IM, DSV DK, KNIN SW, Correos

When a company is undergoing a turnaround, we believe the higher up the income statement we go, the more informative. Revenue growth needs to return to the company and this needs to drop down to a more marked improvement in profitability. While the European industry standard is to look at operating income, we believe EBITDA is more informative around the bottom of a turnaround.

Beyond a strong equity story, the company is rebuilding its strategic plan, and I could hardly be more excited to have this finalized and communicated more thoroughly to the market. Under-pinned by considerable leadership actions the company took throughout 2020 to transition commerce in Portugal online for the first time in a meaningful way, we are focused on the company becoming the e-commerce back-end of the country. E-commerce penetration per capita is significantly lower than the levels of other European peers, leaving a long runway of growth ahead. Statistics here are unusually difficult to find, but the parcel figures from 2018 point to a very long road ahead. While many in Portugal have tried shopping online, the frequency of these orders has been significantly lower. Large e-tailers have largely ignored the country up until Covid-19, which is why the company took the leadership position it did.

Exhibit 2: Parcels Per Capita in 2018

As announced with the third quarter results, its joint venture dott.pt had 1,240 merchants selling on its platform. Additionally, the company’s own efforts have been helping a further 1,500 vendors create their online shops while also assisting with the various other stages of the e-commerce journey. A key hire from Amazon fulfillment should help consolidate the 3rd party fulfillment offer and make it more competitive. Fulfillment has direct synergies with idle daytime sorting capacity, and will allow any vendor to shorten the order to delivery time considerably, without paying a higher price for shipping. The company has made various other investments and forged partnerships to help small and medium sized enterprises thrive in an e-commerce world. In doing so, it has not only built a Shopify-like story, but it has taken considerable market share on the Iberian peninsula throughout 2020. The merchants already on its 2 platforms would represent a top 15 Shopify market when population-adjusting the statistics. While these efforts have yet to materialize as new revenue line items for the company, they have acted as a catalyst to accelerate e-commerce growth in the country.

Exhibit 3: Shopify’s Top Markets- Population Adjusted

Now we’re not trying to imply the company has Shopify-like valuation upside, nor a global reach. But the strategic moat is becoming almost just as attractive, and it’s getting harder and harder for competition to compete with the better, faster, cheaper and greener service that mimics the equity story from a fundamental perspective. We look forward to the management team executing and communicating its progress here in the year ahead.

At the beginning of last year, we had thought that CTT would be driving a considerable amount of alpha for the fund as the turnaround took hold. Actions taken in mid 2019 by the new management team led to EBITDA being up 49.7% in the first two months of 2020. Of course, severe logistics challenges for most of its customers led to an air pocket in the second quarter, and the company reported a rough Q2. But it remained committed to delivering revenue growth for the full year. Judging by our global peers’ stock and revenue performance, this means the CTT’s stock under-performed its global peers by at least 30% looking at the Global S&P 1200 by returns and revenue.

Exhibit 4: 2020 Stock Returns by Estimated Revenue Results – S&P Global 1200

Data Source: CapIQ

In contrast to most stocks borrowing performance from the future, we view CTT’s pent up performance as the opposite. We have unwillingly traded trailing performance for future performance. It’s inherently unpredictable when the market will catch up with reality precisely, but we know that it will eventually. The board and management team have been investing significant time to refining & executing on a strategic priority list that we believe will resonate very well with the market. The narrative inflection point in CTT, in addition to the improving fundamental performance, we believe, will drive material alpha in the quarters ahead.

New Framework, Old Process

“Sometimes you have to play a long time to be able to play like yourself.” -Miles Davis

In last quarter’s letter, I detailed how we actively look to diversify our behavioral exposures in the market. We have also further refined how we rank investments behaviorally. This framework rhymes with a mental model I have used since 2005, when I started on the buy-side as the last guy on the totem pole of a great group of special situations investors. We were always looking for catalysts to unlock the transformations that we saw happening, rather than wait on fundamental performance to generate all the returns.

But then as I articulated a few years ago, catalyst investing no longer works as it did in the early 2000s. But the core of what we do hasn’t changed. We have always looked for assets that had the potential to materially inflect their business trajectories. But that fundamental inflection needs to be reflected by the market for the returns to equal that fundamental development over time. Our new behavioral framework has helped us to express the special situations framework in a systematic way, anchored by probabilities and possibilities to help us ensure we will prioritize companies that can transcend the behavioral steps.

We’re not scared of investing in companies that aren’t growing revenue double-digits, as long as we believe there to be a very strong chance of this performance accelerating over our holding period. Such shifts, particularly in top-line growth, help drive these narrative inflection points that help generate considerable performance.

Exhibit 5: Long Portfolio Market Narrative Evolution in 2020

Key: Upgrades in Green, Downgrades in Red. Exits struck out

While it wasn’t the positions that we would have guessed in the beginning of the year, almost half of our long investments graduated to a more favorable narrative over the past year. Rolls-Royce was the only one that deteriorated, and it deteriorated markedly at exactly the worst possible moment.

In the quarter, we exited Rolls-Royce due to significant concerns over corporate governance, and it was by far the worst-performing investment for us during the year. This resulted from strategic and capital allocation mistakes the board forced upon the management team, which we continue to respect. Looking back at both this mistake, and others I have made over the past decade, we believe there needs to be a higher threshold for skin in the game as it relates to investments in “turnarounds”. This skin in the game can be relative to executives’ own net worths, or it can be absolute in most cases. Or in the case of CTT, it means where we have direct and considerable influence. The vast majority of our portfolio, and nearly all net exposure, has management teams or boards owning a significant amount of the shares outstanding. This keeps the managers or guardians of these businesses very closely aligned with us on a long-term basis.

Throughout 2020 nearly half of our investments were better appreciated by the market and this drove most of our performance during the year. While we have taken capital away from some of these graduates to reinvest in companies we believe are closer to further inflection points, we remain committed to and invested in our higher quality narrative investments. Our four investments in the “compounder” narrative group should drive revenue growth of close to 100% per year for the foreseeable future. In this context, we still find the current stock valuations attractive and they remain top-ranked names in our ranking framework that balances value, quality and behavioral considerations.

The growth at a reasonable price (GARP) companies are starting to grow revenue at a decent rate, but profitability at a meaningfully higher rate. All three companies are at very early stages of transforming their businesses into faster growing and significantly higher margin companies.

The majority of the companies in our portfolio maintained their value or turnaround narratives, particularly those ex-US, while Covid has also delayed some transformative developments at these companies. Most of our “value” names are indirect beneficiaries of the global pandemic. Examples here include CTT, BOL FP, CCJ, and a new UK position.

In a period in which many are throwing in the towel on value, we are remaining true to our roots. But at the same time, a few friends have questioned whether or not we are still “value investors.” Some others have mentioned they’re not sure what our style is anymore. Such confusion is understandable, particularly after looking at exhibit 5. Since we’re always trying to anticipate names that will no longer be penalized by the market with a very low valuation, when looking at a static snapshot of the portfolio, it will at times look like a portfolio that isn’t entirely value. But the process remains exactly the same, we start nearly all investments as value investments, creating a hopefully favorable entry point in a company that is higher quality and faster growing than a value trap. No one wants a value trap, and we don’t want investments that stay around for years in the “value,” territory.

But the evolution of how manic depressive Mr. Market will react is inherently unpredictable and is not a science. It is not often driven by a distinct binary catalyst. A great example of this is MicroStrategy, which we were fortunate enough to buy in October. The company was trading at the same revenue-based valuation as IBM despite showing an inflection in both revenue and profitability throughout the year. Significant improvements made to its core software offering in 2019 and 2020 are now being unleashed at highly disruptive price points for the software industry it operates in. At the same time, the company was unable to return its excess cash on the balance sheet to investors as a result of the low participation of the share tender it conducted last year. So over the summer, the company put this cash reserve into Bitcoin (BTC) to protect the value of its treasury from the unabated central bank printing presses.

Exhibit 6: M2 Money Stock (savings deposits, time deposits, and money market funds)

We view MicroStrategy as the safest and most accretive way to gain exposure to BTC. We’re not going into our entire thesis of BTC here, given the thousands of pages written on it by our peers, both positively and negatively skewed. But suffice it to say, given a heavier-weighting to value-oriented positions in our portfolio, we are slightly leveraged to higher interest rates. Our one major worry about these fundamentals and valuations is the possibility that central banks will artificially hold interest rates below inflation for a very long period of time. While we’ve made a conscientious decision to reduce our portfolio’s net exposure to the Nasdaq, this is the primary performance risk we have as the Nasdaq’s excess returns correlate at -54% to the 10Y bond yield over the past few months, down from -69% at the beginning of January.

MicroStrategy and BTC are our hedge against such destructive monetary policy continuing to hurt value stocks and higher-interest-rate biased companies. While we intend to maintain exposure to BTC for the foreseeable future, we are actively managing this position in the fund.

Exhibit 7: Excess Nasdaq Returns to 10Y Yield

It’s A Barnum & Bailey World

“This is not a time when you should take a lot of lessons from the market.” -Bill Carey

Almost every time I wake up to check news lately, Nat King Cole’s voice rings in my head singing, “it’s a Barnum & Bailey world, just as phony as it can be. But it wouldn’t be make believe if you believed in me.” As it happens, I am fortunate to count Bill Carey as a close friend, who was also very close to the Cole family. When having a conversation in November about some of the lessons learned over the past year, Bill interrupted me by advising that it’s not a great time to be taking big investing lessons to the bank.

I can’t stop thinking about what he said. It’s a time to stay very humble and not draw permanent lessons from what is largely a once-in-a-paper-moon market. It’s a market of haves and have-nots, with no rational ceiling for those that just “have it.” As mentioned in the beginning of the letter, we have been staying conservative despite having a very robust opportunity set. It’s been tough keeping gross long exposure under 100% given the number of attractive opportunities in front of us, but we are determined to not use leverage. Chris started our firms’ regular monitoring of our portfolio securities correlations and we’ve worked hard to eliminate our correlated exposure to the high-fliers,Nasdaq, and small cap exposure. Wally Carucci’s voice constantly reminds me to “feed the birdies,” here.

While most investors are drawing confident conclusions about how the world will behave post Covid-19, a few are even using straight lines when projecting new-economy growth rates from 2020 forward. 2020 was a remarkable year for so many reasons and what happened in 2020 will almost surely not continue at the same rate in any category.

Human nature is inherently difficult to change over long periods of time. We are more aligned with executives and managers that are taking advantage of the current situation to invest where others are cutting, to unapologetically think physical while everyone else is thinking digitally, and are getting prepared for a vaccinated world and a global population yearning to break free from confined living. We have continued re-directing capital to “re-opening stocks” in the fourth and first quarters.

We’re going to continue to work hard on maintaining a very timely portfolio of investments that have material upside as the behavioral market narrative begins to match the underlying fundamental narrative. Most of our time outside of constructivist efforts continue to be dedicated to short opportunities, where we’ve had to replace most of our exposure over the past year as Boeing, Volkswagen and the real estate shorts largely played out. And we are working very hard to ensure the fundamentals of CTT will support a considerably more favorable market narrative. We look forward to many portfolios companies graduating in the year ahead.

Committed to deliver,

Steven Wood, CFA