This article was inspired by a talk that our friend Adam Sebba at Cookson Adventures gave in Azerbaijan last month. The text and slides are available towards the end of this article. Thank you, Adam, for a highly engaging discussion!

Q1 hedge fund letters, conference, scoops etc

Evolving Social Status

Social status has been one of the primary drivers of human behavior since the earliest days of civilization. Throughout different cultural periods, status has meant different things. In Roman times, it was most honorable to have land and serve in the military, hence the farmer was one of the most exulted roles a Roman could occupy. Then later in the middle ages (for the Western world), as empires disintegrated along with trade routes and geographical mobility, the Catholic church came to be the most desirable institution to penetrate. The church saw this development as a monetization opportunity and sold nearly any role or any degree of forgiveness to the highest bidder. It took its monopoly status so far that it invoked Martin Luther and the Reformation to push back against the overt corruption of the wealthiest in society at the time.

Until the enlightenment movement and the semi-global revolutions against monarchies, status then tended to be determined by one’s family name. Then, with the founding of America, enlightenment ideals were ensconced in a government contract, and society and family heritage went into a multi-century decline in importance. Even in the early days of the United States, when it was just a rag tag group of scrappy colonies, status was partially determined by service to the country, but also importantly, by the wealth of the person. Wealth came to summarize one’s contribution to society and colonial development. To summarize brashly, we tied social status to our spending power, and therefore our social status was determined by where we lived, what we wore and later, what we drove. All personal interactions we had with friends and acquaintances were characterized by what we looked like and perhaps how we got there. Sometimes we would have friends over to our habitat to eat or celebrate, where we could show off more stuff. And that was the extent of our interaction with our social circles. That was the environment by which we formed judgements of our friends.

Then with the invention of social media, all of that changed in the most dramatic sense.

I must caveat that while I was an early adopter of Facebook, when it was still confined to college students, I have shunned social media for the last decade. So I can’t claim to be a social media expert by any measure. But social media changed the window with which we have to judge our friends and acquaintances. For the first time in human history, we continuously interact with people while they are relaxing, while they are on vacation and while they are bored at their job.

The Experiences Economy

Quite rapidly, social status today has morphed from what car we drive and what handbag we have to what we do on a daily basis. Social media can also bring out the vain side of us, and for the ones that excel in this new digitalized interactive world, everyday life is curated, whether its faked or real, and the part that gets shared is often magazine-ready. We laugh when we hear people saying that the Instagram shows someone’s or something’s authenticity, as much of social media is the opposite of authentic. So much human behavior has become what we have been increasingly calling “template behavior.” In most “Save the date” photos or baby announcement photos, even the poses are all the same if you are properly keeping up with the Joneses. Being a Stepford wife used to be shunned, now it is fully embraced.

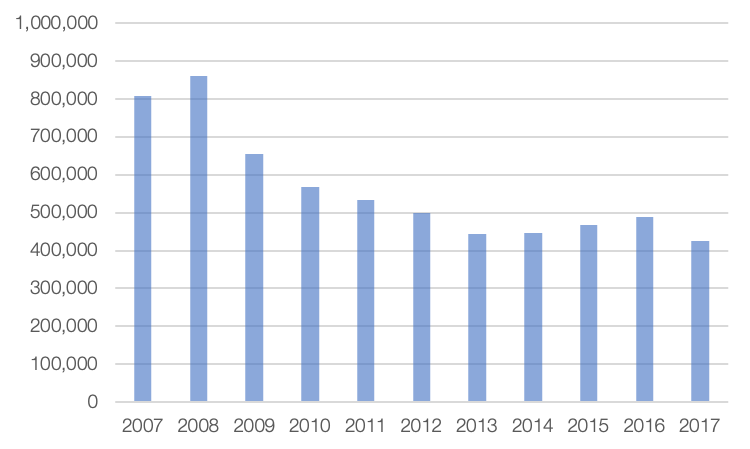

Old stereotypes we would use to judge people have also evaporated. Former negative social signals such as “living in the middle of nowhere and driving an old Subaru” are now the same friends that have organic farms of some sort, their daily lives are picture-perfect while the manhattan sky rains down on the rest of us with bone-chilling temperatures and no camera filter. They are clearly happier than us. And they are absolutely the kings of the new social hierarchy. Perhaps the most self conscious humans on the planet, adolescents, not only no longer care what car they drive to school or around town, they don’t even bother to get their driver’s license anymore. The cool kids of today are no longer the BMW drivers.

Exhibit 1: New Drivers’ Licenses in Spain

As authentic engagement has declined, our craving for in-person interaction has surged. Witness the fact that us and a record number of fellow investors continue to make the annual pilgrimage to Omaha during the Berkshire meeting, despite the fact we could all watch it online in bed at home without the $300/night LaQuinta Inn experience (bring your shower shoes). We need the interaction with our peers and friends. And we pay quite a price for the experience.

This development is not new, it’s just accelerating. Just a few years after the invention of Facebook, we first heard this movement articulated by Pandora co-founder Tim Westergren in a Wall Street Journal interview called “Pandora’s Radio Head.” Tim noted, “With increasing technology, people will actually go to concerts more than ever. The irony of technology is you become on one hand more connected, on the other hand more disconnected. People are going to yearn for that real, live human engagement.”

That comment thankfully drove us to looking at LiveNation as a potential investment, which was then out of favor, as the concert industry is a late-cycle business and had not yet turned up from the global financial crisis. Tim helped us make quite a nice return from our sub $9 purchase price on the stock. We unfortunately no longer own the global concert monopoly, as favorable returns, a rich valuation and an enthusiastic consensus caused us to sell way too soon.

Yet there is another John Malone-related company we purchased under deeply unpopular conditions, and remains one of our favorite positions today.

TripAdvisor FTW

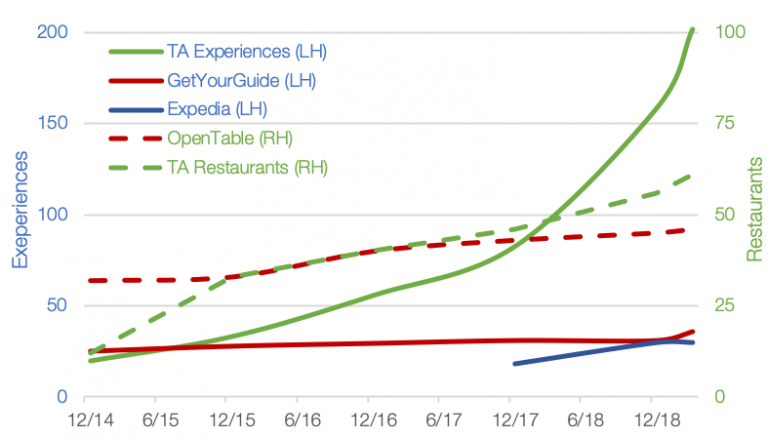

While LiveNation dominates the global concert industry, TripAdivsor is the number one site people use around the world to find travel inspiration, figure out where to go and more importantly, what to do when they get there. In a clever evolution, the company has now allowed its >3 billion users or >400 million monthly active users to see what their friends recommend they do the next time they visit New York, Paris or Thailand. The company has the most data on travelers, by far the largest base of organic traffic and app downloads, the largest dataset on traveler preferences through its 700 million reviews, and increasingly has the largest inventory of bookable experiences and restaurants.

Exhibit 2: Bookable Inventory of Experiences & Restaurants

The company has doubled-down on its massive lead and has accelerated its operating and marketing expenses in this division at a very robust clip. Short-term oriented investors have voted with their feet and traded the stock down, but we believe the company should not focus on profit-maximizing this segment where it has a very significant lead versus peers. It should do exactly what management has been doing, which is value maximize the opportunity. We have the potential to become a global monopoly for in-destination experience discovery and booking, currently a $150 billion market (revenue available for online booking agents being $20-35 billion). While our investment is of course not contingent upon this blue sky scenario coming true, it surely is within grasp while consumer habits and behavior have not yet formed. Only a minuscule few percentage of in-destination experiences are being booked online. This is our market to lose.

Already, we are generating 14x the revenue from Experiences than AirBNB is, despite the unicorn dumping a tremendous level of resources and attention into growing this segment. There are a lot of Softbank-funded startups that are trying to make a dent in the industry, and while we welcome their awareness-building, they are all giving up on trying to compete on inventory, as we are pulling away from the pack with at least a 5x advantage. Ubiquity of inventory has been a key “killer app” for all online e-commerce businesses, so a mass market business like GetYourGuide trying to focus on “unique,” experiences looks set for failure. If someone has waited a year to travel to Hawaii, they will want to make sure they book the best snorkeling tour available, not just the only one available on a fringe platform. The only way to eliminate the FOMO risk is to book with the partner that has everything. We believe tour operators will either need to focus on highly tailored unique experiences or will need to offer all mass market options, and there is little room for the bookers in the middle.

If you don’t believe Malone or Masa about the opportunity here as consumption converts from things to experiences, just look at where the chairman of LVMH, Bernard Arnaud, the third wealthiest man in the world and the king of “selling status” is spending his capital.

Selling Status

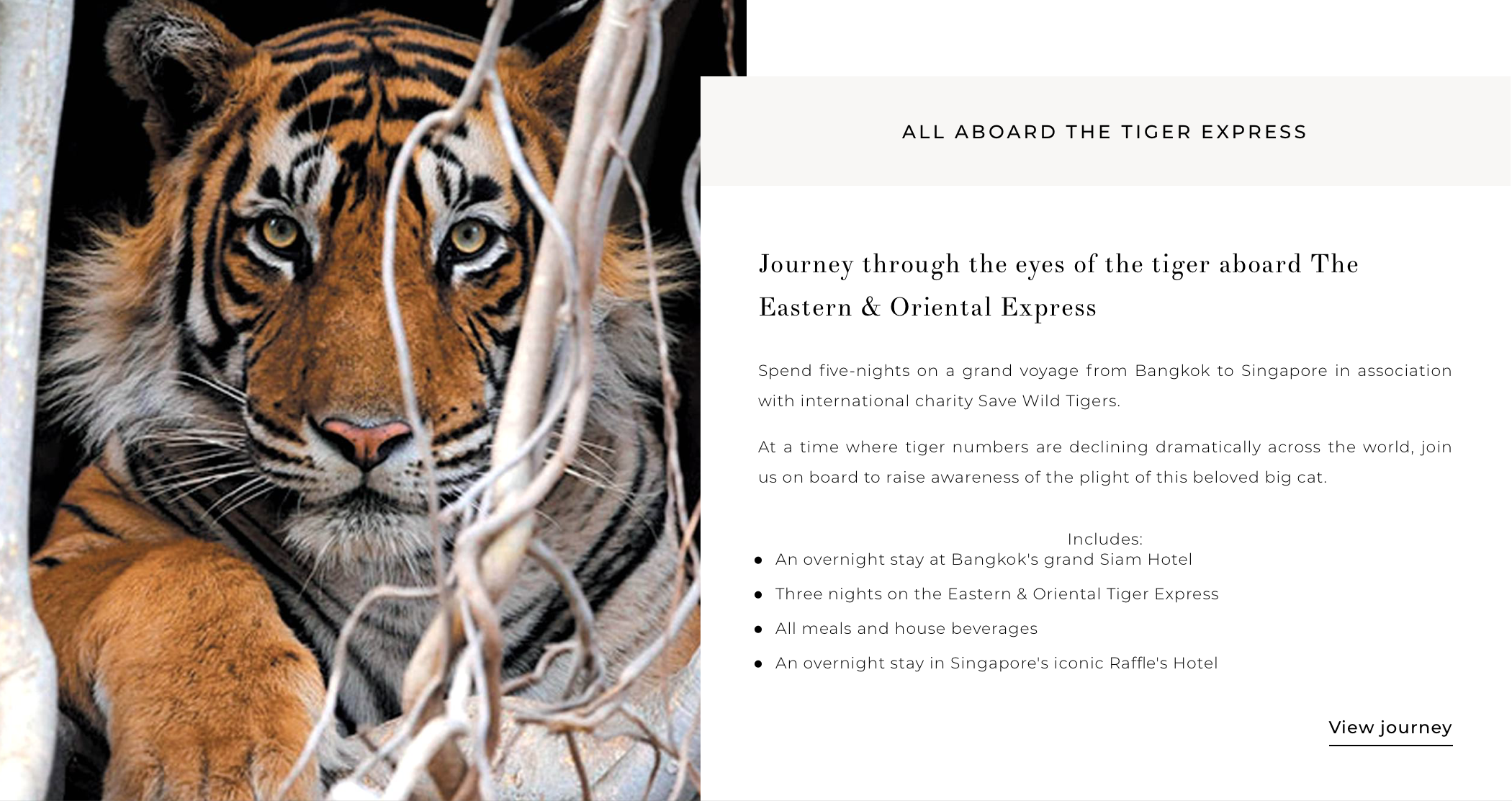

LVMH has masterfully built an irreplaceable collection of brands that sell products to elevate their customers’ lifestyles and social status. Yet, as social status moves towards what you do, not what you have, the economy of “stuff” is giving way to the Experiences economy. Perhaps the best validation of this is LVMH’s large and high-valued purchase of Belmond Resorts. Belmond is just as much an Experiences curator as it is a high-end resort. While travelers can book just a few nights at one of its hotels, the company tries to package experiences throughout its collection of assets, whether it be a luxury train ride through jungles or mountains, or curated photo excursions with Leica-sponsored world class photographers. This is perhaps the best scaled luxury tour operator of one-of-a-kind experiences, sunsets on the Serengeti or moonrises over the Mediterranean.

Exhibit 3: Just one of Belmond’s Experiences

Another of our investments, Ferrari, has built its entire ecosystem on offering unique and world-class bespoke experiences to its highly loyal Ferraristi. Because its clients are buying a full ecosystem and year-round invitation-only events, while the monetization may occur, like Apple’s, through hardware, the hardware is really just one of the many reasons why its clients remain highly loyal.

Last month in Azerbaijan, our friend Adam Sebba, who is the CEO of Cookson Adventures, delivered a highly thoughtful and engaging discussion about the experiences economy from his birds’ eye view. Cookson makes Belmond look like a Marriott. It has offered its clients opportunities to discover ship-wrecked cases of champagne from the 1700s (still drinkable), discover entirely new species of sea life, and routinely gets exclusive access to UNESCO heritage sites, closed to all but its clients. Adam generously allowed us to share his thought-provoking presentation, and because most of it is images (we would expect nothing less), we’ve included the script of his speech. Should any readers be craving the experience of a lifetime, we highly encourage getting in touch with Adam. He will win the top end of the experiences economy, as, with any luck, we win the mass market >$20B opportunity.

“The impulse to travel is one of the hopeful symptoms of life.”-Agnes Repplier

Investors can find our two research notes from this month and our overhauled model on TripAdvisor, as well as take our newest survey on our TripAdvisor page here.

Adam Sebba’s Speech for ValueX Caspian – slides here.

You are a caveman, and your life revolves around subsistence hunting for your meat as opposed to selecting it for same day delivery, (from Ocado, of course Isaac!) so of course your spear has superior value to watching the sunset outside your cave.

As our culture has evolved away from subsistence, experience for experience’s sake has naturally and gradually increased it’s importance over the physical, the convenient, or the vital and I believe today we stand at a tipping point where experience is overtaking the importance of product in our culture.

So perhaps we can all agree that we are on a trend, that experience is becoming increasingly more valued and valuable. So, I am going to look at 2 things: 1. Will that trend become sharper or shallower? 2. Might it even reverse? And does it mean that when making investment decisions one should diligence how a company gets their customers to experience and emote with products just as much as you diligence the quality of the product…

Firstly – sharper or shallower?

Taking the example of Neanderthal man. 8000 BCE – the first evidence of farmed animals. No need to hunt. Driver; efficiency, survival.

- The ready meal released to market. Driver; convenience, efficiency.

2019 – Hello Fresh, Simply Cook, Gousto. I could go on. Packets of ingredients for you to cook at home. Less convenient, less efficient. Driver: experience.

I think this is an interesting example of a signpost that shows the curve is sharpening and we are at a tipping point. The trend is becoming more pronounced. In postmodern design, efficiency is subordinate to function; in postmodern world, everything is increasingly subordinate to experience.

The beautifully gift wrapped packages Net-a-Porter sent by same day delivery are another perfect example. The experience of receiving the gift or – self gift – is almost more important than the content.

As with so many trends, it is Asia driving the momentum. In China, the demographic segment of ‘little emperors’; Children, now adult consumers, who have grown up under one child policy from 79-2015 with a 4-2-1 family structure; 4 grandparents, 2 parents and 6 wallets and sets of attention focussed on them are demanding next level ultra-personalised and bespoke experiences. And across Asia, the trend that sees almost 80% of Koreans under 35 living with their parents (no rental or car ownership) which results in disposable incomes disproportionately higher than salaries, driving out of home expenditure on luxury experiences.

Bain and Co’s luxury Study also records a huge increase in client’s expenditure on intangibles such as holidays and experiences – a 10% CAGR over the last 7 years – a trend that is particularly pronounced in China, with the 2019 version of the Shanghai company’s annual Chinese Luxury Consumer also pointing to increased expenditure in non-physical assets.

On a recent experiential trip we organised, one of our clients justified the purchase of a $3m state of the art 400m capable 7 person glass submarine. ‘it’s beautiful and more useful than a sculpture’. When compared against expenditure in asset classes of wine, art, real estate and cars, our business is noticing that the new class of having fun and creating memories – including sharing deep sea exploration with your whole family is increasingly winning higher share of wallet. Sharper and sharper.

Second data point; something I’ve realised from our employees – House prices have so outstripped average earnings, that a London house is now 15x mean earnings. And assuming 5-10% of salary saved annually, it would take 15-30 years to save for a deposit; consequently, Millennials and Gen Y – my entire workforce – have little chance of purchasing a home and so we have a rootless ‘generation rent’ who view all income as ‘disposable’ and so prefer to consume experiences rather than assets. This trend is not reversing any time this generation’s lifetime (unless we see a substantial correction in house prices).

Disruptive business models have further exacerbated the trend. Companies challenging traditional ownership models; in clothes, Rent the Runway and my wardrobe.com have led consumers to borrow, not own their clothes – Netflix have effected the disappearance of once ubiquitous shelves of DVDs from thousands of households, transitioning them to rental of media. This increases consumers’ comfort with non-ownership models of even bigger assets, with Zipcar shifting traditional asset ownership of cars to experience-led club, sharing or rental models. The data supports expansion of this rental market.

It is not just the under 40’s, or even the super-wealthy. The desire to consume more experience runs across all age groups – at the other end of the age spectrum, Baby Boomers are SKI-ing (spending kids inheritance) and ticking off their increasingly expensive bucket lists, desert safaris, immersive travel and even Antarctica cruises.

In 2019 – 13 new cruise ships were launched (including 7 explorer vessels) adding capacity of 33,000 a week or up to 1.7m annually to the cruising market. And ships are being better utilised, with up to 2.7m more passengers expected in the next 2 years.

Even with physical purchases, the data show that consumers make purchasing choices based on emotion and prefer the experiences that accompany ownership, to the ownership itself.

Panerai watches , the luxury watch marque owned by Richemont, a month or so ago released three new limited editions. But this is nothing unusual for the innovative Swiss watch market, who regularly release special commissions.

The remarkable aspect of these releases is they each come with an experience, exclusively available to the new owners of these timepieces, and an integral part of the purchase. The Carbotech, a camouflaged military watch, comes with a day serving with the Italian Special Forces and their specialist diving team; The Submersible a visit to French Polynesia to free dive with the world free diving champion. And the Submersible Mike Horn edition; a polar expedition with the eponymous adventurer, Mike Horn.

All are unique experiences, the sort that the highest-level travel companies, such as Cookson Adventures, have been organising for years. But what is fascinating for the travel industry is the realisation that we are now living in an age where experience is paramount, almost ranking above product and assets. The travel industry trade in experiences and memories, intangibles. However, the hard luxury companies are realising now that they must play catch up to capitalise on this trend!

And so my conclusions from our worm’s eye view: Short – companies making DVD racks, insurance companies selling personal auto insurance, mortgages, beach holidays; long personal submarine manufacturers, rental; of everything;

Short Spears; long sunsets.

When looking at companies to invest in, my perspective indicates that the ones that will outperform their peers understand and have already evolved to orientate themselves around a new normal of consumer expectation in order to serve people like the 20 something candidate interviewing for a new role with our business who, when asked about his 5 year plan simply responded…. “A passport full of stamps rather than a house full of c**p”.

Article by GreenWood Investors