Grey Owl Capital Management commentary for the second quarter ended June 30, 2019.

Q2 hedge fund letters, conference, scoops etc

“Disneyland will never be completed. It will continue to grow as long as there is imagination left in the world.” – Walt Disney

Dear Client,

For the most part, the second quarter saw a continuation of the first quarter’s positive performance across many asset classes. This furthered a reversal of the dismal 2018 when every primary asset class was negative: US equities, long-dated US government bonds, gold, and commodities.1 While Q1 2019 was a “risky” asset story with equities and commodities leading the way, during Q2 2019 “haven” assets were strongest. Gold led the way, up 9.2%, and long-dated US Treasury bonds gained 5.7%. It was not all haven assets – the S&P 500 notched a respectable 4.2% increase. Commodities were the sole laggards – down 1.9%.2

While we used the weakness in the fourth quarter of 2018 and early 2019 to increase our equity exposure, this reversed in the second quarter. As markets continued to rally in the April through June period, we were more often sellers, rather than buyers. This was less a reflection of our views on the overall market and more a consequence of “events” and transactions that naturally occur when market sentiment is ebullient.

Four Days in June

During the second quarter we closed four equity positions. Two provided meaningful gains and two were small losses. When we invest in individual securities we want to have more winners than losers, but we also want our winners’ gains to be much larger than our losers’ losses.4 In the small sample defined by the parameter “positions closed in the second quarter of 2019,” we had the same number of winners and losers.5 On the second criteria, we did much better – our winners’ gains were quite a bit larger than our losers’ losses.

Over the course of four business days in late June, significant corporate events had a largely positive impact on four of our portfolio holdings. On June 24, Bristol Myers Squib (BMY) announced that in order to accommodate Federal Trade Commission (FTC) requests, they would have to divest a business line prior to the acquisition of Celgene (CELG). Also on June 24, Eldorado Resorts (ERI) announced the acquisition of Caesars (CZR). The next day, June 25, AbbVie (ABBV) announced plans to acquire Allergan (AGN). Finally, on June 27, Howard Hughes (HHC) announced that it had retained investment bankers to explore “strategic alternatives” for the company. We sold Celgene, Caesars, and Allergan on June 25. We sold Howard Hughes in early July.

We had purchased Celgene in early April just subsequent to both of the principal proxy advisory firms coming out in favor of Bristol Myers Squib’s acquisition of Celgene. We felt that there was close to 6% upside (with optionality related to a contingent right6 included in the deal), and there was a high probability the deal would close and do so within three months. In other words, modest risk but for well better than cash returns – so, a reasonable place to put some idle cash to work. On June 24, Bristol Myers announced that the FTC was requiring that Celgene divest a business line prior to the merger and that the deal would take until at least the end of 2019 and possibly into early 2020 to close. We decided to move on given the elongated period and the likely headline risk drug companies will experience as we move toward another US presidential election. We lost about 0.6% on the position.

Caesars was a recent purchase. We bought the stock in November 2018 (mentioning the purchase in our fourth quarter 2018 letter). After emerging from bankruptcy in a complicated structure, the stock was under pressure until activist investors (Tilman Fertitta and Carl Icahn) started to take an interest. In short order, Icahn acquired a 30% stake in the company and engineered the Eldorado acquisition. The stock had reacted favorably to talk of an acquisition and on the day Eldorado announced the deal it increased 15%. It is not often that you identify a cheap security with multiple catalysts and the situation develops as you would have hoped in a little more than six months. We bought the stock at $8.26 and sold it at $11.57 for a 40% return.

Allergan is a different story. We initially purchased shares in Allergan in July 2016. We added to the position in early 2018 and then made a third and final purchase in November 2018. When we first purchased Allergan in 2016 the stock was already down over 30% from its late 2015 high and the price to earnings ratio was at a reasonable level for a strong, diversified franchise – 17x. Earnings grew about 24% between 2016 and 2018. However, the majority of the earnings growth occurred between 2015 and 2016. Since then earnings have gone mainly sideways. During that period, the stock performed poorly and the multiple shrunk significantly. AbbVie’s acquisition is at a price to earnings ratio of approximately 10x. We maintain Allergan holds several terrific franchises and AbbVie is getting them for a song. Our average cost was $179.75 and we sold the stock at $163.95 after AbbVie announced the acquisition and the stock popped 25% on the day. Our overall loss was just under 9%.

Howard Hughes is a real estate development company with significant assets in New York City, Columbia Maryland, Las Vegas, and Hawaii. We originally purchased Howard Hughes in 2011 for $61/share. There were a few buys and sells over the years that led to an average cost basis of $86/share7. While the company has demonstrated value over the years by converting raw land into valuable property, the majority of value remains undeveloped (and, in our opinion, unrecognized until the stock price’s recent move higher). There are no publicly traded comparable companies and most public-market real estate investors focus on real estate investment trusts (REITs) that are fully developed (“stabilized” in the industry vernacular) and provide yield income in the form of a dividend. Thus, from our point of view (and clearly management and the board or directors too), the stock price has been perpetually undervalued. This new action by the company to seek “strategic alternatives” had an impact – the stock jumped over 40% on the news (clearly investors who follow the name see value, but were unclear on a timeline for realization). While we believe ~$130/share is the low-end of the range for the company’s net asset value, we think it is a fair price at this point. If nothing significant develops from the review the stock could easily fall back below $100/share. Our gain from our current cost basis was 51%.

Disney – Successful Investing Often Requires Patience

For three of the four positions that we closed last quarter (detailed above), the price when we sold was meaningfully higher than it was the week before. Various corporate events led to significant price increases. Investment returns almost never occur in a straight-line fashion. Sometimes the catalyst is obvious (e.g. an acquisition). Other times, it is not exactly clear what will cause the broader investment community to reassess how it values a company. It often makes sense to hold a position for a long time (perhaps years) if one’s assessment of the underlying business quality remains intact.

After years in this business, it can still be amazing to witness what exact information serves to shift investor sentiment. In the case of Disney (DIS), it was the price of its new over-the-top (OTT) product. On April 11, Disney announced that Disney+ would be available in November 2019 for $6.99. The stock price, which had been trading in a range between $90-$110/share for four years immediately shot up above $130/share and now trades above $145/share. To make our point, it is important to emphasize that the only new information was the exact date of launch and the price. Did investors really think Bob Iger was going to screw up the pricing on this new product?

When we purchased Disney in May 2016 for $99/share there was significant concern regarding Disney’s most profitable enterprise, ESPN. Investors were worried about Disney’s ability to navigate the simultaneous move from cable to over-the-top distribution and the increased value extraction by sports rights owners (e.g. the NBA demanding more money for their contract with ESPN). There was also concern that original OTT players like Netflix would damage the value of Disney’s non-sports entertainment catalogue. While we did not know exactly how Disney would navigate that challenge, we were confident in a few things.

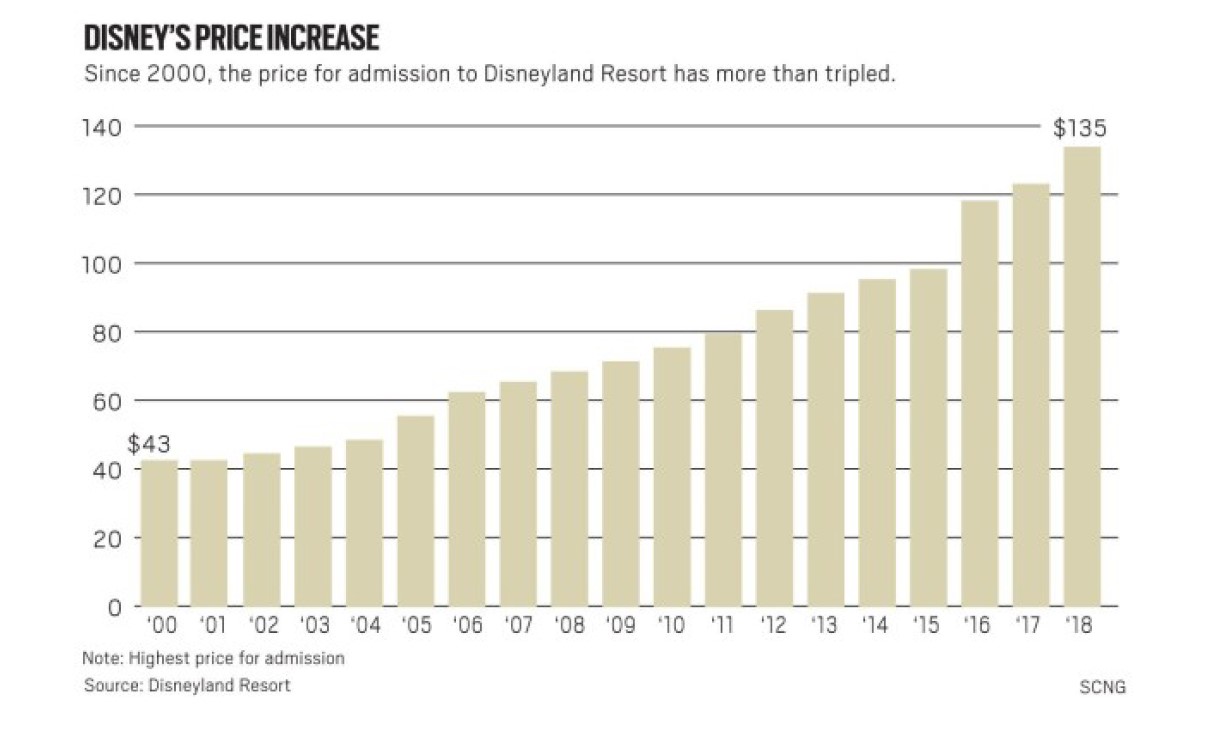

Disney’s assets are its catalogue and the multiple platforms it has to monetize its content – media, parks, and merchandise. While distribution is in flux, it is not as important. Here is what we believed when we bought Disney and what we continue to believe today. First, Disney has the broadest catalogue of entertainment assets, many of which are evergreen. Second, Bob Iger has proven masterful at adding to them by acquiring Pixar, Marvel, and Lucasfilm. As CNBC recently highlighted, Marvel titles have grossed $18B since Disney paid $4B for the franchise in 2009.8 The Fox deal further reinforces this point. Third, Disney is incredibly skilled at taking content and leveraging it across its multiple platforms. None of this has changed and we did not and still do not think it will. Yet, what made the stock “work” recently is the market now knows Bob Iger will not screw up pricing Disney+. The price is going to be low enough to drive subscriptions and market share. Years of price increases will come later. Just look at the parks.

*****

As of late-July 2019, credit spreads, gold, and other measures of broad market sentiment indicate a slightly risk-averse investment environment – more risk-averse than when we last wrote in late April. Given the equity market rally (and position specific events), we have sold several positions and hold more cash today than we did three months ago. With some of our sale proceeds we increased our exposure to gold. We also added an initial position in AGNC Investment Corp. (AGNC). Both of these positions function as “haven” assets – they would likely work well if investor risk-aversion continues to increase. In addition, we still maintain exposure to long-dated US Treasury bonds – another haven asset. While markets are at a new high, we are monitoring closely the increasing signs of risk-aversion. We will continue to adjust the portfolio as conditions change and opportunities present themselves. Disneyland will never be completed.

As always, if you have any thoughts regarding the above ideas or your specific portfolio that you would like to discuss, please feel free to call us at 1-888-GREY-OWL.

Sincerely,

Grey Owl Capital Management, LLC