“… [W]e cannot do everything ourselves; different people are more capable in different matters… [I]n cases where we ourselves cannot be present, the vicarious faith of friends is substituted; and he who impairs that confidence, attacks the common bulwark of all men, and as far as depends on him, disturbs the bonds of society…” – Cicero, 106-43 BC Oration for Sextus Roscius of Ameria

Q3 hedge fund letters, conference, scoops etc

Don Felder stepped center stage. “I grew up in Gainesville, Florida,” he said. “We were dirt poor. When I was 10, I traded cherry bombs for my first guitar and I fell in love with it. I was never after money and fame. In early 1970, I moved to NYC and struggled. I remember scraping together pocket change to buy a 60-cent plate of yellow rice and beans. I moved to Boston, worked in a music studio and soon after I drove cross-country to California. And I got lucky.” And so did we.

On a dark desert highway, cool wind in my hair

Warm smell of colitas, rising up through the air

Up ahead in the distance, I saw a shimmering light

My head grew heavy and my sight grew dim

I had to stop for the night.

There she stood in the doorway;

I heard the mission bell

And I was thinking to myself

‘This could be heaven or this could be Hell’

Then she lit up a candle and she showed me the way

There were voices down the corridor,

I thought I heard them say

Welcome to the Hotel California

Such a lovely place (such a lovely place)

Such a lovely face.

Plenty of room at the Hotel California

Any time of year (any time of year) you can find it here

In Denver this week, our group of 70 had no idea as to what was to come. We were expecting an economist, we got our minds rocked instead. Ladies and gentleman, Don Felder from the Eagles. With his double neck guitar in hand, Felder jammed, the room erupted.

He told stories and sang for several hours. “In early January 1974, Felder was called by the Eagles to add a slide guitar to their song ‘Good Day in Hell’ and some guitar licks to ‘Already Gone.’ Shortly afterwards, he was invited to join the band. The first album that the Eagles released after the lineup change was Hotel California, which became a major international bestseller. Felder submitted ‘16 or 17 tracks’ that resulted in the songs ‘Victim of Love’ and the album’s title track, ‘Hotel California.’” (Source)

I bet somewhere buried deep in your storage area is that old Hotel California album cover.

Last thing I remember, I was

Running for the door

I had to find the passage back to the place I was before

‘Relax’ said the night man,

‘We are programmed to receive.

You can check out any time you like,

But you can never leave!’

Songwriters: Don Felder / Don Henley / Glenn Frey

In great spirits, we returned to the hotel and more than a few of us gathered at the bar. I call it the conference vortex – that late evening pull of attendees to the bar. I’ve lost a few of those battles, regretting it the next morning. No regrets this week.

And it looks, too, like the markets have little regret. As you well know by now, the Democrats won control of the House of Representatives and the Republicans maintained control of the Senate. Expect gridlock.

Grab a coffee and find your favorite chair. When you click through, focus in on the recessionary and non-recessionary bear markets section. Concluding that a likely non-recessionary bear market has begun. I also share a few non-polarizing midterm election thoughts as it relates to the markets and conclude with a few photos in the personal section. You’ll find this week’s piece to be a quick read.

A quick aside: During the week, I often post to Twitter and LinkedIn a news article or chart or piece of research that may make it into On My Radar. What I like about Twitter is that you can follow specific people. My favorites include Ray Dalio, Howard Marks (buy his book), David Rosenberg, John Mauldin, Ian Bremmer, Ned Davis Research and others. Bloomberg’s Lisa Abramowitz is outstanding! Today, I shared a link to Barry Ritholtz’s interview of Ray Dalio.

If you’d like to follow me, simply click below:

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- Various Thoughts: Midterm Elections, Expansions Since 1949 and 2019 Earnings Slowdown

- What to Watch: A Non-Recessionary Bear Market has Likely Begun

- Hotel California: It’s About the Fed… It’s Always About the Fed

- Trade Signals – Equity Trend Rolls; Fixed Income Stalled in a Sell; Don’t Fight the Tape Moves to Neutral Signal

- Personal Note – Pride and Joy

- Various Thoughts: Midterm Elections, Expansions Since 1949 and 2019 Earnings Slowdown

- What to Watch: A Non-Recession Bear Market Has Likely Begun

- Hotel California - It’s About the Fed… It’s Always about the Fed

- Trade Signals - Equity Trend Rolls; Fixed Income Stalled in a Sell; Don’t Fight the Tape Moves to Neutral Signal

- Personal Note - Pride and Joy

Various Thoughts: Midterm Elections, Expansions Since 1949 and 2019 Earnings Slowdown

On the Midterm Elections – Gridlock

Tax-Cut Roadblock – from Bloomberg News via good friend, Bill Watkinson:

- The Democrats’ control of the House will almost certainly prevent another round of tax cuts on the heels of those enacted in December. Deeper tax cuts, if large enough, could have pushed the Federal Reserve to raise interest rates more aggressively to keep the pace of economic growth from causing inflation to accelerate.

Gavekal analysts, Will Denyer and Tan Kai Xian, think the positive attitudes will probably persist as divided government reduces the risk of some problematic policy changes.

Summary – via Mauldin Economics:

- Historically, legislative gridlock has been modestly positive for U.S. stocks.

- A static regulatory environment lets businesses focus on business instead of sometimes arbitrary government policy changes.

- The already-passed tax cuts will remain in force and additional cuts that now won’t happen might have driven interest rates higher.

- Rather than a minimum wage hike, Congress may now increase earned income tax credits – a more efficient way to help low-income workers.

- The chief market risks now are new trade barriers, higher labor costs and rising interest rates.

- Bottom Line: The election clarified some economic issues and left one giant uncertainty, which is trade policy. It’s uncertain because the President can make big changes on his own authority and the Democratic House will have little ability to stop him. The next marker will be Trump’s meeting with Chinese leader Xi Jinping at the G20 Summit later this month. A positive outcome – or at least the appearance of one – might spark a year-end rally. Stay tuned.

Cumberland Advisors – John R. Mousseau, CFA:

- Divided government, with different parties in control of the House and Senate, has sometimes led to gridlock. It also tends to keep spurious legislation from being passed; and so overall, markets are OK with this outcome.

- From a spending standpoint, the divided Congress will most likely keep the President’s spending in check and this may slow the current rise in the deficit (a good thing from our perspective).

- We’re still checking final results, but we know that California voters rejected almost $9 billion in bonds for water projects and Colorado rejected over $3 billion in a transportation bond.

- If state income taxes and local property taxes are no longer deductible, anything that raises the level of spending and potentially higher taxes is likely to get a cold shoulder, as people’s EFFECTIVE taxes will rise in any case with SALT provisions.

- We do believe that with the current low unemployment level, a national infrastructure program with federal subsidies is not needed and is now more unlikely with divided government.

And finally, a more aggressive view from Martin Armstrong:

- Expect nothing but obstruction. Running the government is no longer a priority. This is just going to be a grudge match from here on out and that is what the model has been projecting.

- Nothing but panic cycles and directional changes in politics and our models on third party activity will rise into 2024 as more and more people begin to see that the political situation has become hopeless.

My Thoughts

“… [W]e cannot do everything ourselves; different people are more capable in different matters…

[I]n cases where we ourselves cannot be present, the vicarious faith of friends is substituted;

and he who impairs that confidence, attacks the common bulwark of all men,

and as far as depends on him, disturbs the bonds of society…”

– Cicero, 106-43 BC Oration for Sextus Roscius of Ameria

We are losing or have lost confidence in leadership. Not just in the White House; it is broader than just that, it’s everywhere. The right becomes more right and the left becomes more left. Perhaps it’s as challenging as Neil Howe’s Fourth Turning says it will be. He identifies it as the crisis stage. An era in which America’s institutional life is torn down and rebuilt from the ground up—always in response to a perceived threat to the nation’s very survival. In every instance, Fourth Turnings have eventually become new “founding moments” in America’s history, refreshing and redefining the national identity. Maybe? We are seeing the stresses in the U.S. and globally. History shows us we have been here before. Today, we sit in a period of time similar to the mid 1930’s… debt, protectionism, etc. An unacceptable gap between the haves and have nots.

All successful teams have exceptional leadership on the field. It’s healthy to have a different view. It’s healthy to have our views challenged. We grow. We have leadership that creates divisiveness. Unfortunately, I don’t see it changing in the next two to four years. Expect gridlock. We are better than this.

Here is the link to the Ritholtz-Dalio interview I shared today on Twitter: https://www.bloomberg.com/news/audio/2018-11-08/ray-dalio-discusses-major-financial-crises-podcast-jo96qfgi. Put your headphones in and take a 55-minute walk. It is good.

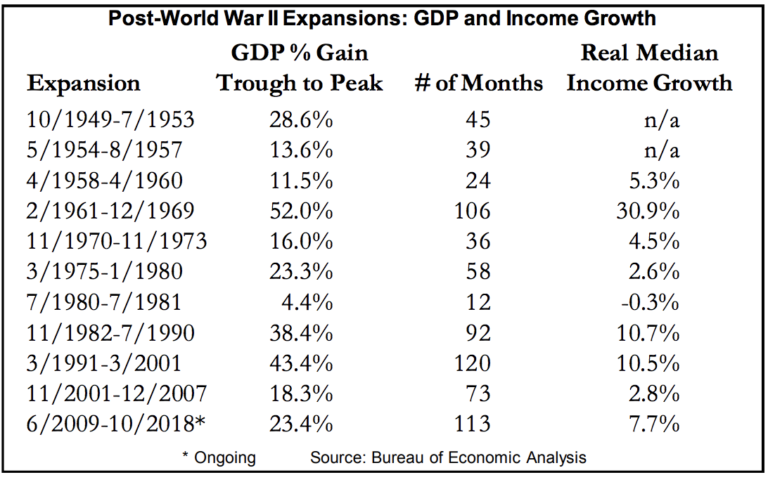

Economic Expansions since 1949

At 113 months, the current expansion is the second longest. I believe it is likely to challenge the 120-month expansion from 1991-2001.

Bottom line: We are late in the business cycle. Recessions follow expansions. Probable recession in 2019.

Source: Gary Shilling’s INSIGHT

Expect 2019 Earnings Slowdown

Earnings growth will slow in 2019. Much of 2018’s earnings growth is coming from Trump’s tax cuts and the repatriation of cash that led to a surge in share buybacks. That’s behind us. The coming year-over-year comparisons will be tough. Wage growth and rising interest rates will also pressure margins. Earnings deceleration is a common characteristic in the late stage of economic expansion. We are clearly late stage. Historically the stock market has struggled when earnings growth has been significantly slower than the year prior. It’s been bumpy and likely to remain bumpy through 2019.

What to Watch: A Non-Recession Bear Market Has Likely Begun

If evidence emerges that the U.S. economy is slowing, a non-recession, cyclical bear market would be the most likely outcome. That’s my base case.

Since 1946, non-recession bears have had a median decline of around 23% lasting about six months. With recession, the median decline is 37% lasting an average of 17 months.

NDR did a study looking at data back to 1946. They found there have been 16 corrections of at least 10% within what they define as cyclical bull markets. There are secular (or long-term) bull and bear market cycles (we are currently in a long-term secular bull) and shorter-term cyclical bull and bear market cycles. Of the 16 minus 10% cases, eight were followed by breadth thrusts. Breadth thrusts are defined as a high percentage of stocks moving up together – an indicator of market strength. Healthy markets see the majority of stocks accelerating vs. just a few carrying the market higher as was the case in 1999 and perhaps Facebook, Amazon, Apple, Netflix and Google in the current cycle. Recall that in September, just 10 stocks accounted for more than 100% of the 9% gain in the S&P 500 Index. A great example of the lack of broad-based stock participation or non-breadth thrust.

- In the eight cases where there was positive broad participation, the cyclical bull lasted another 22 months and the S&P 500 Index gained an additional 56.3% (median percent change) before reaching a peak.

- In the eight non-breadth thrust cases, the cyclical bull lasted another six months and the S&P 500 Index gained an additional 21.3% (median percent change) before reaching a peak.

- Bottom line: The S&P 500 gained 13.6% over seven months from the February 8 low to the September 20 high. Looking at the non-breadth thrust data (1946 to present), odds favor the short-term cyclical bull market top is in. Absent recession, downside risk is 23%. Lighten up or hedge that equity exposure on rallies and buy the 20% dip.

The S&P 500 tested its February low and held. It is currently sitting just above its 200-day moving average line. A 20% correction from the September 20, 2018 high of 2,931 is roughly -600 points. Vegas odds favor a better buying opportunity below 2,400. We’ll see.

Hotel California – It’s About the Fed… It’s Always about the Fed

‘Relax’ said the night man,

‘We are programmed to receive.

Ultimately, I still believe the Fed will be called to the rescue and do extraordinary things. Just not yet. The conference vortex has them belly up to the bar. On the sidelines. Giving the markets room to breathe.

You can check out any time you like,

But you can never leave!’

They have checked into Hotel California but can never leave. Debt is a mess. Especially in the corporate space. QE will be back in the coming default crisis. We are late cycle. The good news is there is no current sign of recession. Best guess is mid-2019. Data dependent, as they say.

Keep your recession watch lights on. As the great Art Cashin says, “Don’t lower your guard just yet. Stay alert and very, very nimble.”

Trade Signals – Equity Trend Rolls; Fixed Income Stalled in a Sell; Don’t Fight the Tape Moves to Neutral Signal

November 7, 2018

S&P 500 Index — 2,774

Equity market trend remains in an uptrend. The Ned Davis Research CMG U.S. Large Cap Long/Flat Index and 13/34-week EMA on the S&P 500 Index both signal bullish.

High yield and high-quality fixed income signals remain in a sell.

This week, the Don’t Fight the Tape or the Fed has moved to a neutral “0” reading. You’ll see when you view the data (below) that it is when the reading reaches -2 that we should become most concerned.

Click here for this week’s Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note – Pride and Joy

I’m in Atlanta on Sunday and Monday for some golf with friends. Really looking forward to that. John Mauldin and I are hosting a dinner in NYC on Wednesday with several advisor meetings to follow on Thursday. John will present his thoughts around the Great Reset, we’ll discuss portfolio strategy and share a few ideas.

John’s from Dallas and a Cowboys fan and, of course, I dig deep into my Philadelphia roots. The Philadelphia Eagles and Cowboys face off Sunday night. We’ll be watching the game together… I see a fun wager and hopefully an Eagles “W” in my near future.

Susan’s been in Kansas City this week advancing her coaching career. U.S. Soccer has launched a grassroots program in an effort to ultimately lift our national team’s competitiveness on the global stage. Not making the last World Cup was likely a good motivator. The thinking, as best I understand it, is to get it right from the ground up. The program is long and intense with the goal to teach the accredited coaches how to coach the grassroots coaches.

Gone are the days when the moms and dads stepped in. The graduates will be coaching the U.S. “D” license; something that I believe all soccer clubs will require of their coaches. She is one of approximately 30 who have now gone through their program and the thinking is that if they can get 500 or so coaches teaching coaches, we will build a better culture of advanced learning. Like a stone thrown into a pond, it’s a ripple effect that will expand and help U.S. soccer achieve at the highest level.

I’ve been learning a great deal about management… There is an abundant amount of self-reflection built into the process. The coaches are mic’ed up, videotaped and assessed while giving a PowerPoint presentation of the curriculum in front of their teachers and their peers. Broken down, analyzed, wash-rinse-repeat. Frankly, I’m learning a lot from her and find I really need to do a better job with my team. Record yourself, record your team… she keeps telling me. You’ll learn so much. Agreed!

Late in his set, Felder talked about his relationship with his friend, Stevie Ray Vaughan. He told us about how he helped him with the song “Pride and Joy.” A song I’ve long forgotten. I searched for it on Spotify and emailed it to Susan. You’re my pride and joy! And so are our kids!

A special toast to your Pride and Joy!

Have a great weekend…

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO