Hayden Capital letter to investors for the fourth quarter ended December 31, 2017.

[timeless]

Dear Partners and Friends,

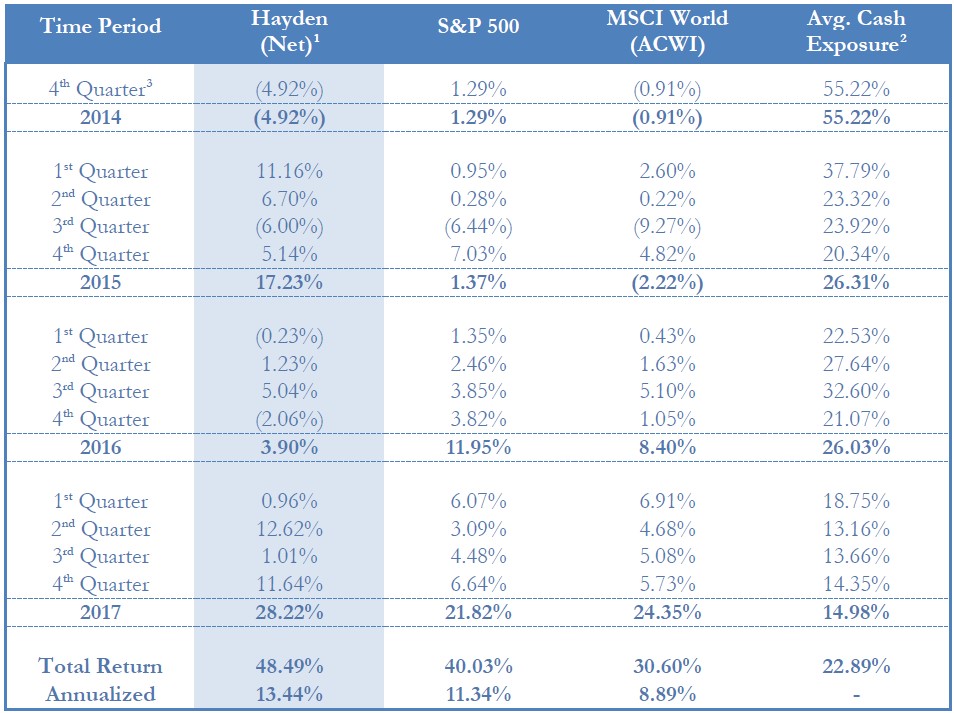

Our portfolio closed out 2017 on a strong note. During the fourth quarter, Hayden Capital’s portfolio gained +11.6% (net of fees), and finished 2017 with a +28.2% return for the full year. Comparatively, the S&P 500 and MSCI World Indices were up +21.8% and +24.4%, respectively.

This brings our compounded annual return to +13.4% (net of fees) since inception, versus +11.3% for the S&P 500 and +8.9% for the MSCI World Index. During this period, our cash balance has averaged ~23% since inception, and ~14% in the most recent quarter.

Learning How To Trust

Recently, I did a presentation for the MOI Global Best Ideas 2018 conference (a few slides from the deck are shown below). In it, I discuss at a high-level our research process for potential investments, and how we see our role as investment managers (LINK).

I think the discussion of the how to analyze companies is an interesting one, and something that I wish more investors talked about. Instead, discussions at conferences or within investors letters usually center around the what (“what are we buying, what happened in the portfolio, etc.”). But personally, I don’t think this is nearly as helpful in understanding a manager’s thought process or portfolio composition (which after all, isn’t that the purpose of these communications with our partners?).

Some in the industry are fearful of publicly talking about their investment process, due to the fear of giving away the “secret sauce”. However, I have a different perspective.

Instead, I see it like the research process in hard sciences (i.e. physics, mathematics, etc.), where one team may take the previous findings of another, build on top of it, with the combined effort eventually resulting in a new breakthrough for the entire field. There’s no reason the investment industry can’t be similarly collaborative and learn from one another… not all investing is a zero-sum game.

It’s with this goal, that I enjoy talking about our investment framework & process – with the hope that those in the community can take these ideas and iterate off them (which our portfolio / process may then benefit from in the future). Similar to most scientific research, these thoughts are always “works in progress” and can only benefit after thorough feedback / peer review. The only way for these frameworks to evolve and become more robust, is after significant poking and prodding. It’s for this selfish reason, that I’m always open to feedback on flaws or aspects of our process that can be improved.

**

So to start the discussion, I’d like to highlight how we approach the age old question (at least it is among investors): “How can we judge management? Can we trust someone enough, to be confident they’ll make the right decisions, years in the future, regarding issues which haven’t even been determined yet?”

It’s a tricky issue, but a very important one for growing and evolving companies, who are entering new markets / initiatives, and especially where the future may look very different than today.

First, the issue is you’re outsourcing very important decisions that can have huge implications on your net worth, to someone else (i.e. management). Many investors aren’t comfortable giving up this much control, and trusting someone else to steer them through the abyss and leave them more profitable on the other side. How do we know management isn’t painting a rosier picture of the future, than reality?

Second, these decisions are going to be made in the future. Even if you trust management today, how do you know they’ll make equally sound decisions 5 – 10 years from now, or won’t suddenly go bonkers?

The most common method investors use, is to see how management has performed in the past, to predict how they’ll perform in the future (i.e. “The company has historically earned 20% ROICs the last 10 years under the current CEO. It’s likely they’ll continue doing so”). The hope is, smart people don’t suddenly make dumb decisions over night, right?

This is a good start, but I personally don’t think it’s enough. Companies and their competitive environments change over time. So even though it’s had great returns in the past, it may not be true in the future. Therefore, how can we predict what the industry’s future will look like, and that the people running our companies will be smart enough to navigate it?

It’s interesting that in the investing field, asset owners / allocators make this decision every day4. They’re the experts in the subject of evaluating people (aka Investment Managers). Instead of having quantitative data to rely upon (i.e. earnings or cash flows), it’s a purely qualitative decision. The only data you have are past returns (but we’ve all know that past returns aren’t indicative of future results…). So how do allocators get comfortable investing in someone’s future decision-making abilities?

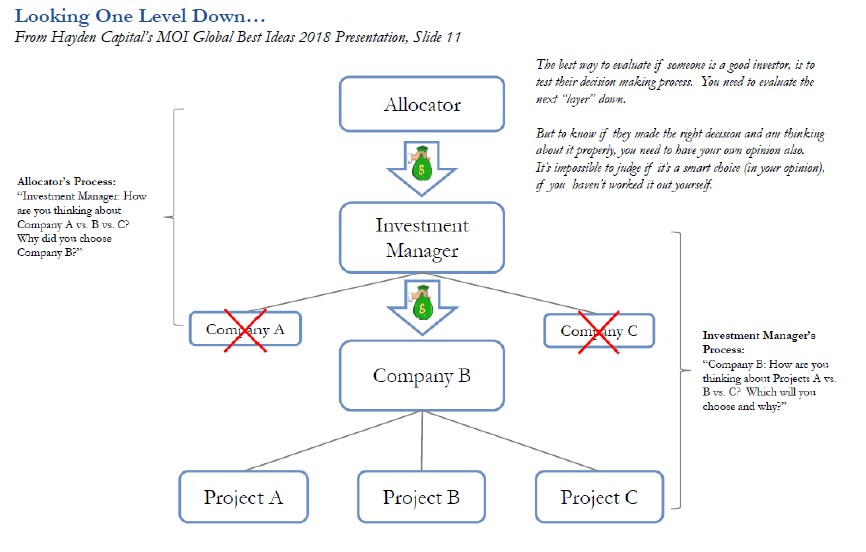

After speaking with many allocators, it seems the consensus is that there’s no better method, than to drill “one layer down” (i.e. conduct an extensive review of the manager’s portfolio). The investor’s portfolio today should be representative of all prior decisions the manager has made, including those which were passed upon and those which were enacted. Simply, there’s no better way to understand how a person thinks.

The idea isn’t just to see what the allocator would be invested in, if they were to write a check. After all, by the time they invest (sometimes several years later), the portfolio holdings are probably going to be different.

Rather, the most important aspect is building trust in the manager’s thought process, and way of looking at the investment world (i.e. “Am I confident the manager will make the right decisions for the portfolio in the future?”). And understanding why past decisions (rather than what decisions) were made, may be one of the best ways to understand how future decisions will be made.

Importantly, the best allocators know that to be good at this, they’ll need to know enough about the target company, to have an informed opinion themselves. Chances are, they’ll never know an investment as well as the manager (I mean, why would you pay the manager, otherwise?). But it’s important to know enough, for how can you objectively judge if someone is smart / trust that the process is sound, if you haven’t done enough work to have an objective opinion on what the “smart answer” is?

**

Along these lines, I’ve been thinking whether we can use a similar process to evaluating companies and their management teams. If the best allocators are looking one layer down at a manager’s portfolio as the best way to judge their future returns and thought process, shouldn’t we do the same as investors?

After all, the end-goal is very similar – to predict which “portfolios” and managers will outperform in the future. Companies have an underlying “portfolio” too – a collection of projects which they’re investing in hoping to get an attractive future return (whether it’s a new factory, an e-commerce initiative, a warehouse, etc.).

Most likely, as an investor you’ll never know the business as well as management (just like allocators won’t know the portfolio as well as the investment manager). But perhaps by evaluating these companies “portfolios” today, and the thought process behind building them, we can have a better judgement on management and confidence in the future “portfolio”. We’ll never be 100% certain or accurate, but we don’t need to be. Getting it roughly right, and more importantly, building trust in the team managing the daily operations is often better than not5.

Note: Heck, often management is does not have a clear picture either… they’re simply trying to make the best decisions possible with the information available. And in today’s data filled world where everything is tracked, and information is easily accessible, it’s gotten much easier to have the same access (or at least a large portion) of the same information management has. Reaching an objective opinion on a company’s strategic decisions via primary research is easier today than ever before.

In rare circumstances & if you do it right, you may even reach a conclusion the management team hasn’t thought of yet, and you can influence / add-value to your investment by sharing it with the company6. You’re proactively skewing your risk-reward and chance of success. The best activism is constructive to the growing the overall pie and good for all stakeholders (vs. the financial engineering we often see disguised as “activism” – where activists are simply re-cutting the pie into larger pieces for themselves).

This process requires putting ourselves in management’s shoes, and asking “what we do in the same situation?” And being able to reach that answer requires doing a lot of work to obtain the same information the company has, to reach an independent informed opinion.

It’s like when you meet a new person at a party. They may start talking about (just picking a random topic here) Bitcoin. They might sound very smart and confident, and seem to know what they’re talking about. But how can you know for sure, that they’re actually smart and not just faking it? Well it’s hard, unless you’ve done extensive research on the subject yourself, and after hours of questioning them as to why and how they formed their beliefs, conclude they have done extensive thinking on the subject. Note, it doesn’t necessarily mean they’ll be right. But at least they’ve come to their beliefs in a rational and thoughtful manner (which is already better than 90% of the people I’ve come across…).

For us, this involves analyzing a projects’ Incremental Returns on Capital 7. I’ve discussed our framework / data-point method in-depth in prior letters + our “Calculating Incremental ROIC’s” presentation, so I won’t repeat it here (LINK). However, if we do it right, we think we can gain confidence in what the company’s returns will look like in the short-term (let’s say the next 2 years). This is like that phase, where you’re grilling that new Bitcoin friend, to see if they know what they’re talking about.

What about after 2 years though, or after the company’s current projects are finished? How can we underwrite what the business’ returns look like in Years 3 to infinity?

This is where it gets “squishy”, since you’re essentially betting that the people running the company will make the right decisions, on issues that haven’t been determined yet. It requires trust… and hopefully after thorough “grilling” (evaluating their past decisions, the current “portfolio”, incentives, and the corporate culture they’ve created) you have a good amount of confidence in the decision-making process.

But this doesn’t mean we have to surrender our control completely, and blindly trust them going forward. As investors, we can’t be completely passive either & close our eyes for the next 20 years, letting management “do their thing”. Sometimes the world changes, and requires a new skillset the company doesn’t possess in order to be successful. Sometimes smart people do stupid things8. As investors, we need to be on the lookout for these instances. We need to “trust, but verify”.

Throughout the life of an investment, we should continually evaluate the decisions the company made, and confirm if they were the right ones every step of the way. For instance, for each round of new projects, we should do the same type of analysis as a new investment and constantly ask ourselves if the next two years (or the life of the project) have more attractive, same, or less attractive returns than the previous projects.

In this way, it’s similar being on the Board of Directors. You’re not running the day-to-day operations, but you’re double-checking the decisions they make (even if it’s just to yourself). And perhaps if we see enough of these positive “data-points”, it’s enough for us to give management benefit of the doubt that they will continue allocating capital intelligently in the future.

**

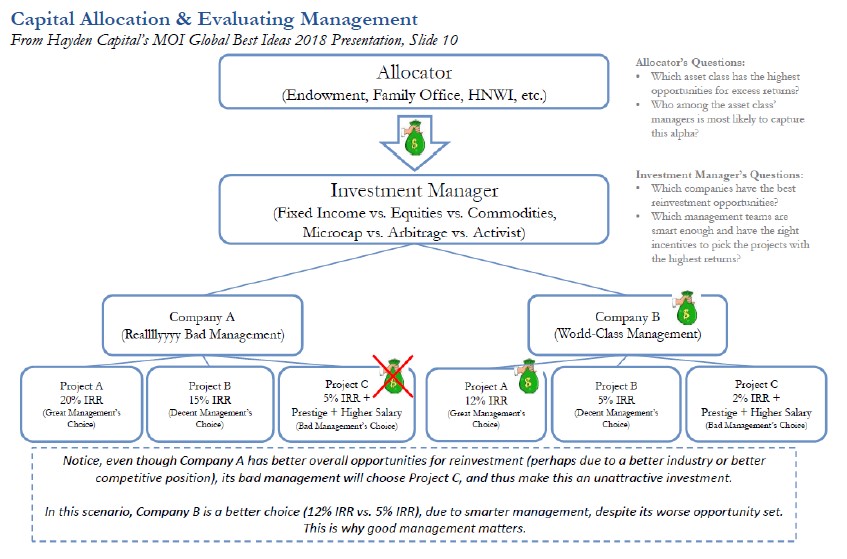

So what are we looking for in our vetting? At a high-level, what we want is management that has consistently shown a history of choosing Project A (see below exhibit). For example, even though Company A is in a more attractive industry with better return opportunities (20% / 15% / 5%), poor management choices & the wrong incentives may lead them to choose the less attractive investment (Project C). On the other hand, even though Company B has a worse opportunity set, great management will result in a better return for investors (12% IRR) vs. their counter-part.