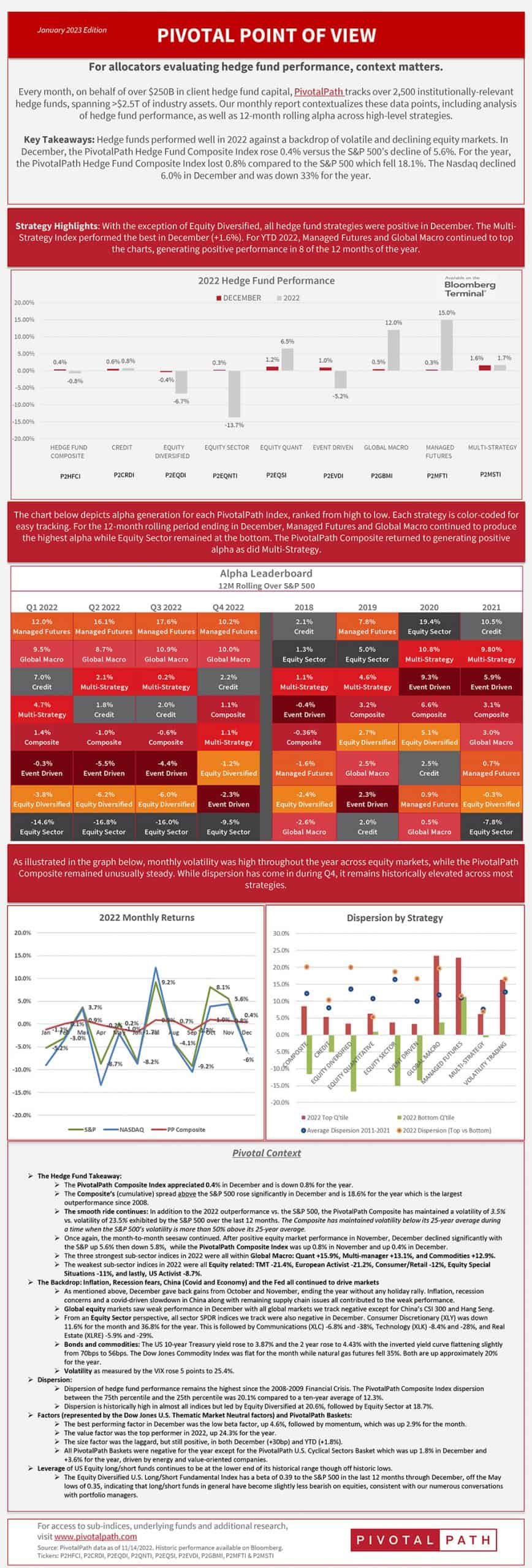

PivotalPath has released their monthly report, the Pivotal Point Of View, which measures performance among more than 2,500 institutionally-relevant hedge funds, as well as 40+ different hedge fund strategies and $2.5T in total industry assets. Our latest report looks at hedge fund performance in December, as well as 2022 as a whole.

Q4 2022 hedge fund letters, conferences and more

Below are a few quick highlights.

- The Composite’s (cumulative) spread above the S&P 500 rose significantly in December and is 18.6% for the year which is the largest outperformance since 2008. Additionally, the PivotalPath Composite has maintained a volatility of 3.5% vs. volatility of 23.5% exhibited by the S&P 500 over the last 12 months.

- December gave back gains from October and November, ending the year without any holiday rally. Inflation, recession concerns and a covid-driven slowdown in China along with remaining supply chain issues all contributed to the weak performance.

- Dispersion of hedge fund performance remains the highest since the 2008-2009 Financial Crisis. The PivotalPath Composite Index dispersion between the 75th percentile and the 25th percentile was 20.1% compared to a ten-year average of 12.3%.