Key highlights for August 2018:

[timeless]

Q2 hedge fund letters, conference, scoops etc

- Hedge funds are up 0.45% for the year, their weakest performance on record since 2011 when they declined 0.40% in the eight months through to August. Almost 46% of the managers are in the green for the year with roughly 12% of these managers posting double digit gains as tracked in the Eurekahedge Global Hedge Funds Database.

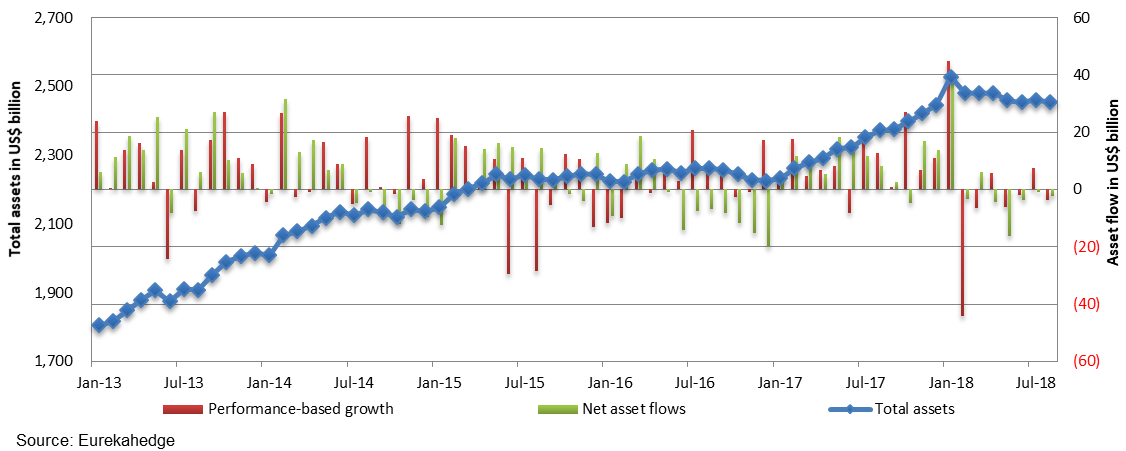

- Total assets under management have increased by US$7.4 billion as of August 2018 year-to-date, down from US$147.4 billion over the same period last year as performance driven losses and subdued allocations from investors cap asset growth. Barring January earlier this year, investors have redeemed US$25.4 billion from hedge funds globally through to August. For detailed asset flow breakdown across regions, strategies and fund size mandates please reply to this email.

- Emerging markets focused mandates are in the red for the year down 3.05% year-to-date, with Asian managers down 2.26% for the year and underlying Eurekahedge Greater China Hedge Fund Index posting losses of 5.94% as of August 2018.

- Across strategies, distressed debt, relative value and event driven hedge funds lead for the year up 7.46%, 3.79% and 1.70% respectively.

- Assets under management for CTAs/managed futures strategies have shrunk by almost 11% in 2018 – corresponding to a decline in AUM of US$29.0 billion in the first eight months of the year. The strategy however posted gains of 1.05% in August, with underlying trend following strategies up 2.64% for the month.

- Across both equities and fixed income assets, North American hedge fund managers remain the bright spot with underlying long/short equity managers up 5.65% whilst fixed income focused mandates have gained 5.35% as of August 2018 YTD. In contrast, emerging markets focused equity long/short managers are down 4.92% while fixed income mandates have lost 3.34% for the year.

- The Eurekahedge Crypto-Currency Hedge Fund Index is down 52.93% for the year. The index has lost more than half of its value over the first eight months of 2018, as fund managers struggled to mitigate the damage caused by the crypto-currency market crash following gains of 1708.5% in 2017.

2018 Key Trends in Asian Hedge Funds

The Eurekahedge Hedge Fund Index ended the month almost flat, gaining 0.09% with gains posted by North American mandated funds offset by losses suffered by managers focusing on Europe, Asia and Latin America. Roughly 28% of the hedge fund managers tracked by Eurekahedge managed to outperform the underlying global equity markets as represented by the MSCI AC World Index (Local) which gained 1.06% over the month. On a year-to-date basis, the Eurekahedge Hedge Fund Index was up 0.45% as of August 2018, with 10% of the constituent funds generating double-digit returns over the first eight months of the year.

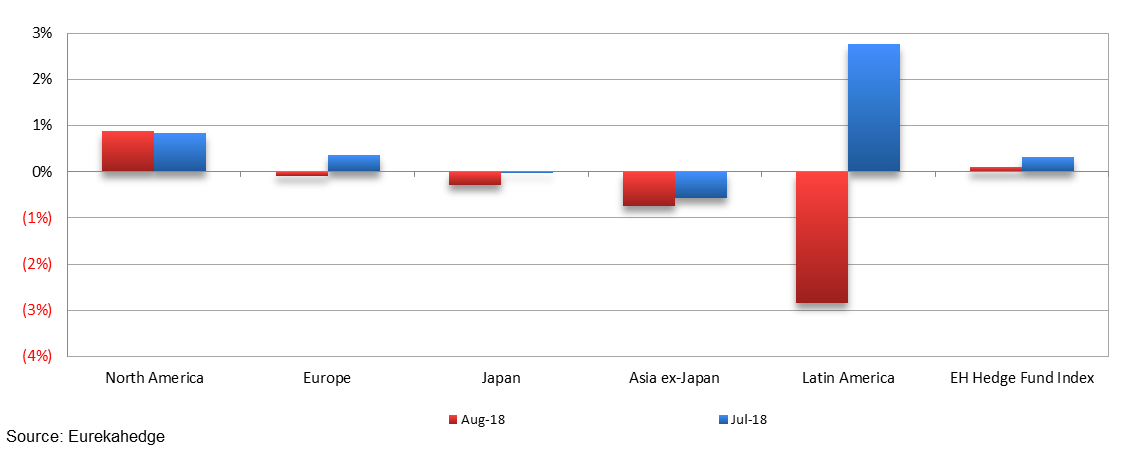

Across geographic mandates, North American hedge fund managers distinguished themselves by gaining 0.88% as the only mandate to end the month in positive territory. Asia ex-Japan and Latin American mandates continued to suffer as the global emerging market rout grew deeper with Turkish lira and Argentine peso plummeting to their lowest points in recent years. The two mandates registered losses of 0.75% and 2.84% respectively in August. Over in Europe, hedge fund managers ended the month dipping into the red, losing 0.09% on average, outperforming the major European equity markets: the FTSE 100, the DAX Index, and the CAC 40 declined 4.08%, 3.45% and 1.90% respectively.

August 2018 and July 2018 returns across regions

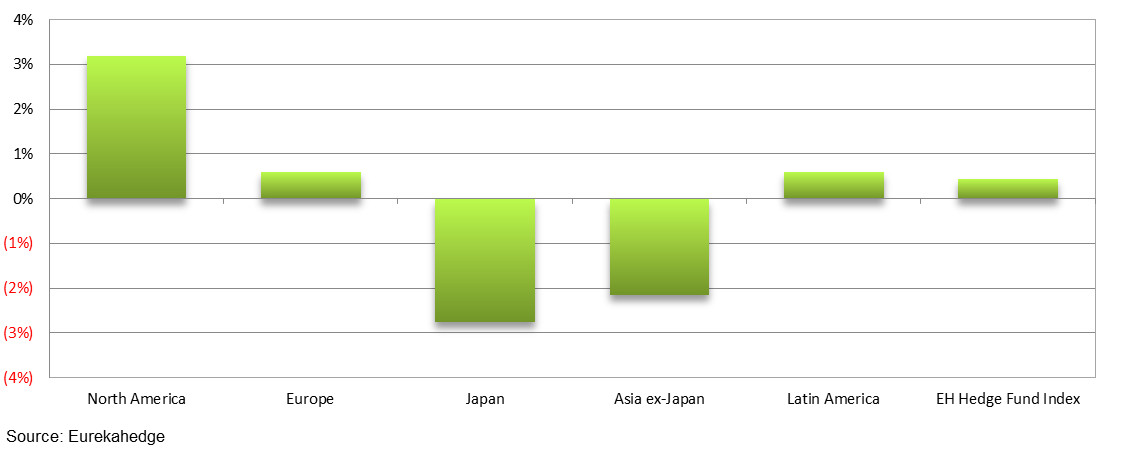

On a year-to-date basis, North American fund managers were up 3.19%, followed by European and Latin American fund managers, both of which gained 0.60% over the first eight months of 2018. Meanwhile, the Eurekahedge Japan Hedge Fund Index which tracks hedge fund managers investing exclusively in Japan was down 2.75% as of August 2018 year-to-date, consecutive months of losses compounded and pushed them to the last place among the regional mandates.

2018 year-to-date returns across regions

Mizuho-Eurekahedge Asset Weighted Index

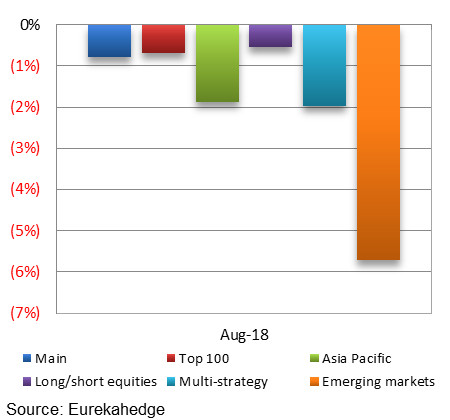

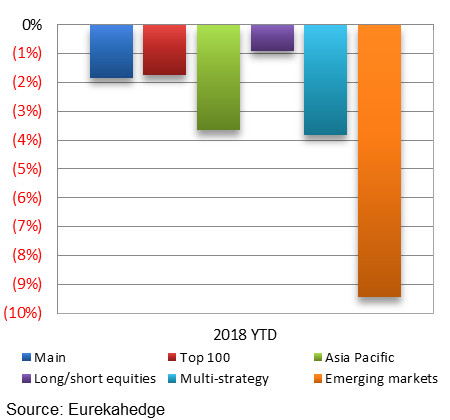

The asset-weighted Mizuho-Eurekahedge Index – USD ended August down 0.79%, bringing their 2018 year-to-date return to -1.85%. It should also be noted that the Mizuho-Eurekahedge Index is US dollar denominated, and during months of strong US dollar gains, the index results include the currency conversion loss for funds that are denominated in other currencies. The US Dollar Index edged slightly higher during the month, gaining 0.62% as the US dollar strengthened against major currencies. Apart from the currency conversion, the noticeable discrepancy between the asset-weighted Mizuho-Eurekahedge Index – USD and the equal-weighted Eurekahedge Hedge Fund Index which returned 0.09% in August were reinforced by losses suffered by multi-billion dollar fund managers. Almost 60% of the fund managers managing in excess of US$1 billion were in the red over the month.

The entire suite of Mizuho-Eurekahedge Indices were down during the month, with the Mizuho-Eurekahedge Emerging Markets Index declining 5.72% in August, securing their position at the bottom of the chart. On a year-to-date basis, all indices were in the red, with emerging markets focused fund managers posting the sharpest decline as they ended the first eight months of 2018 down 4.21%, weighed by the weak currencies and global trade friction which has seen investors fleeing emerging markets since February.

| Mizuho-Eurekahedge Indices August 2018 returns

|

Mizuho-Eurekahedge Indices 2018 year-to-date returns

|

CBOE Eurekahedge Volatility Indexes

The CBOE Eurekahedge Volatility Indexes comprise four equally-weighted volatility indices – long volatility, short volatility, relative value and tail risk. The CBOE Eurekahedge Long Volatility Index is designed to track the performance of underlying hedge fund managers who take a net long view on implied volatility with a goal of positive absolute return. In contrast, the CBOE Eurekahedge Short Volatility Index tracks the performance of underlying hedge fund managers who take a net short view on implied volatility with a goal of positive absolute return. This strategy often involves the selling of options to take advantage of the discrepancies in current implied volatility versus expectations of subsequent implied or realised volatility. The CBOE Eurekahedge Relative Value Volatility Index on the other hand measures the performance of underlying hedge fund managers that trade relative value or opportunistic volatility strategies. Managers utilising this strategy can pursue long, short or neutral views on volatility with a goal of positive absolute return. Meanwhile, the CBOE Eurekahedge Tail Risk Index tracks the performance of underlying hedge fund managers that specifically seek to achieve capital appreciation during periods of extreme market stress.

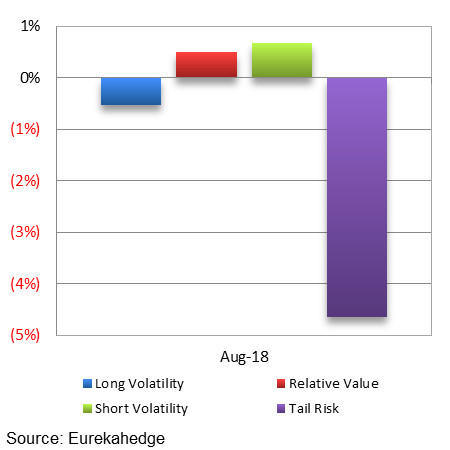

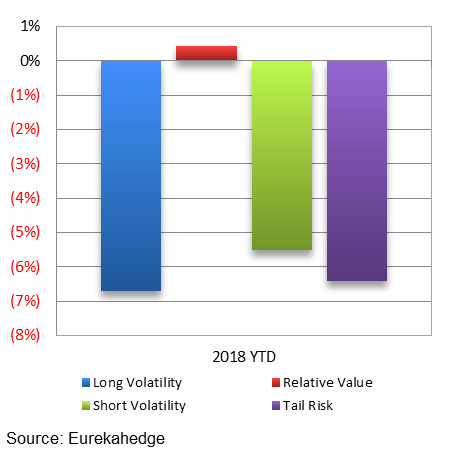

The CBOE Eurekahedge Short Volatility Hedge Fund Index and the CBOE Eurekahedge Relative Value Volatility Hedge Fund Index ended August on a positive note, returning 0.69% and 0.51% respectively. On the other end of the spectrum, long volatility fund managers were down 0.52% this month, and tail risk fund managers dipped 4.64%, dragged down by small funds which posted double-digit losses over the month. On a year-to-date basis, three of the four volatility strategies remained in the red, with long volatility fund managers posting the steepest losses of 6.69%. The CBOE Eurekahedge Relative Value Volatility Hedge Fund Index was the only index within this index suite to post a positive gain (0.43%) as of August 2018 year-to-date.

|

CBOE Eurekahedge Volatility Indexes August 2018 returns

|

CBOE Eurekahedge Volatility Indexes 2018 year-to-date returns

|

Summary monthly asset flow data since January 2013

Eurekahedge

Eurekahedge

Launched in 2001, Eurekahedge has a proven track record spanning over 16 years as the world’s largest independent data provider and alternative research firm specialising in global hedge fund databases and research. Headquartered in Singapore with offices in New York and Philippines, the global expertise of our research team constantly adapts to industry changes and needs, allowing Eurekahedge to develop and offer a wide array of products and services coveted by institutional investors, family offices, accredited investors, qualified purchasers, financial institutions and media sources. In addition to market-leading hedge fund databases, Eurekahedge’s other business functions include hedge fund research publications, due diligence services, investor services, analytical platforms and risk management tools.

Article by Eurekahedge