(28 June 2021) – Economic concerns driving new macro investor enquiries while visible momentum sparks increased investor interest in event-driven funds – HFM Event-driven Composite Index up 11.9% YTD

Q1 2021 hedge fund letters, conferences and more

HFM Insight’s latest strategy reports covers the latest performance vs benchmarks, AUM, investor flows and key trend analysis. This month’s release features the event-driven and macro hedge fund strategies.

Highlights:

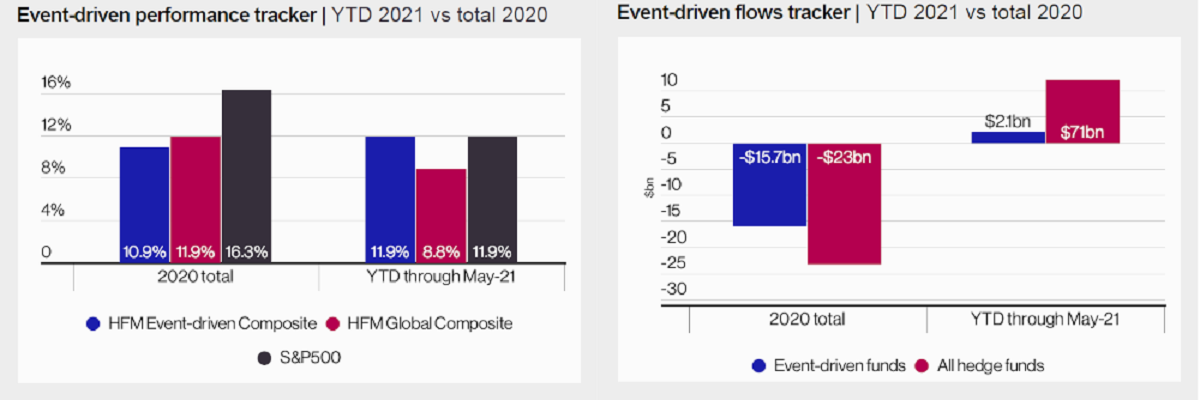

- The HFM Event-driven Composite Index was up 11.9% YTD through May after 1.6% monthly gain

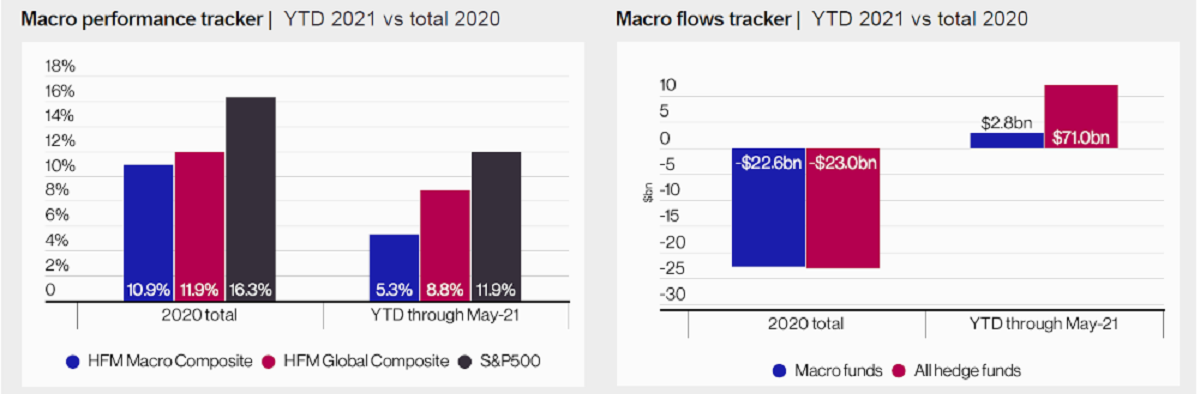

- HFM’s Macro Composite Index up 5.3% YTD at the end of May, trailing most top-level strategies

- Performance gains into event-driven were aided by record levels of M&A activity during the first five months of 2021

- Macro flows set to remain positive in H2 as investors look to navigate inflation concerns

- Investor flows into event-driven were positive in May ($5.6bn), turning YTD flows positive ($2.1bn) as well. For macro, investor flows were also positive in May ($3.7bn), turning YTD flows positive ($2.8bn).

A summary is included below and the compiled report is available for download. If you require more information on this report, have data queries or interview requests, please do not hesitate to contact me. As a reminder, with Pageant Media’s acquisition of Eurekahedge, you now have insights from both HFM and Eurekahedge when it comes to information and data requests – feel free to check in about data from either brand.

Event-Driven

Visible momentum sparks increased investor interest: Event-driven funds gained 1.6% in May, making their YTD return through May the largest among HFM’s top-level hedge fund indices (11.9%). This came on the back of intense M&A activity in H1, high-profile activist campaigns and innovation within existing strategies. Record levels of M&A activity in the first five months of 2021, including several large deals, like WarnerMedia’s merger with Discovery, presented event-driven hedge fund managers with multifarious opportunities to employ arbitrage strategies.

This month HFM reported that $750m Samson Rock Capital had taken advantage of the environment for event-driven managers to launch a new special situations business, led by industry veteran, Rado Bradistilov. Meanwhile, Dallas-based Saltoro Capital, which has returned 92% over 12 months, hired UBS Securities’ global head of hedge fund sales with a view to securing entry into the hedge fund billion-dollar club. All this marks a contrast to H1 2020 when event-driven funds fared considerably worse than other hedge fund strategies during the onset of Covid-19. Following significant net outflows in 2020, event-driven has built on strong performance towards the end of last year by becoming the top-performing strategy of 2021 YTD. Early signs are that this has sparked investor interest, which will continue into H2.

(Source: HFM Insights)

Macro

Economic concerns driving new macro investor enquiries: The average macro fund reporting to HFM gained 1.6% in May, taking the HFM Macro Index’s YTD return to 5.3%, trailing the HFM Global Composite YTD by over three percentage points (8.8%). Having been wary of macro funds for much of the past 18 months, pulling more than $20bn from the strategy in 2020, investors have seen enough from recent performance numbers and economic indicators to increase and/or create macro exposure.

Investor flows added $3.7bn to macro assets in May, turning YTD flows positive for the first time since January, and look set to remain positive over the coming months. Provisional data from HFM’s latest biannual investor sentiment survey suggests a third of hedge fund allocators are looking to increase their exposure to macro funds in H2 2021 – more than for any other top-level hedge fund strategy. Experienced managers will hope to benefit from increased allocations as investors look to navigate the threat of inflation in the US, a slow economic recovery and the prospect of global price dislocations. Moreover, the likelihood of increased interest rates in the medium term and rapidly rising equity and commodity prices will facilitate greater volatility and potential returns for macro funds during the next 18 months.

(Source: HFM Insights)

| Benchmark | May-21* | Apr-21 | Mar-21 | 2021 YTD* | 2020 | 2019 | 12-month* | 3 yr ann.* |

| HFM Event-Driven Composite Index | 1.6 | 2.9 | 1.1 | 11.9 | 10.9 | 7.5 | 34.6 | 8.7 |

| HFM Macro Composite Index | 1.8 | 1.6 | 0.5 | 5.3 | 10.9 | 10.5 | 17.1 | 8.3 |

| HFM Global Composite Index | 1.4 | 2.1 | 0.9 | 8.8 | 11.9 | 9.6 | 25.1 | 8.7 |

| S&P 500 | 0.6 | 5.2 | 4.2 | 11.9 | 16.3 | 28.9 | 38.1 | 15.8 |

*Analyst note: HFM performance indices represent the mean average return of funds on the HFM platform. Indices are based on reported data at time of publication and are subject to future revision.

Download full report with charts

About HFM

HFM provides hedge fund professionals with an unparalleled blend of business essential data, exclusive industry intel and market-leading events. Combining 22 years of industry heritage with a cutting-edge platform, to create true business intelligence; the intelligence needed to raise assets, allocate funds or source new business opportunities. Insights is the research and analysis service from Pageant Media, sitting within the company’s hedge fund intelligence network, HFM. The division produces research reports and analytical articles on a variety of topics in the global hedge fund industry, including business operations, investor relations, technology and regulation. Leveraging Pageant’s wealth of data and news sources, and with access to the HFM network’s vast membership, Insights is uniquely positioned, offering exclusive surveys and expert commentary. Learn more about HFM.