This research note was originally published by the CFA Institute’s Enterprising Investor blog. Here is the link.

[timeless]

Q2 hedge fund letters, conference, scoops etc

SUMMARY

- Equity crowding models can be applied to factors and sectors

- Crowding leads to more frequent drawdowns

- Tech sector was crowded over the last 12 months

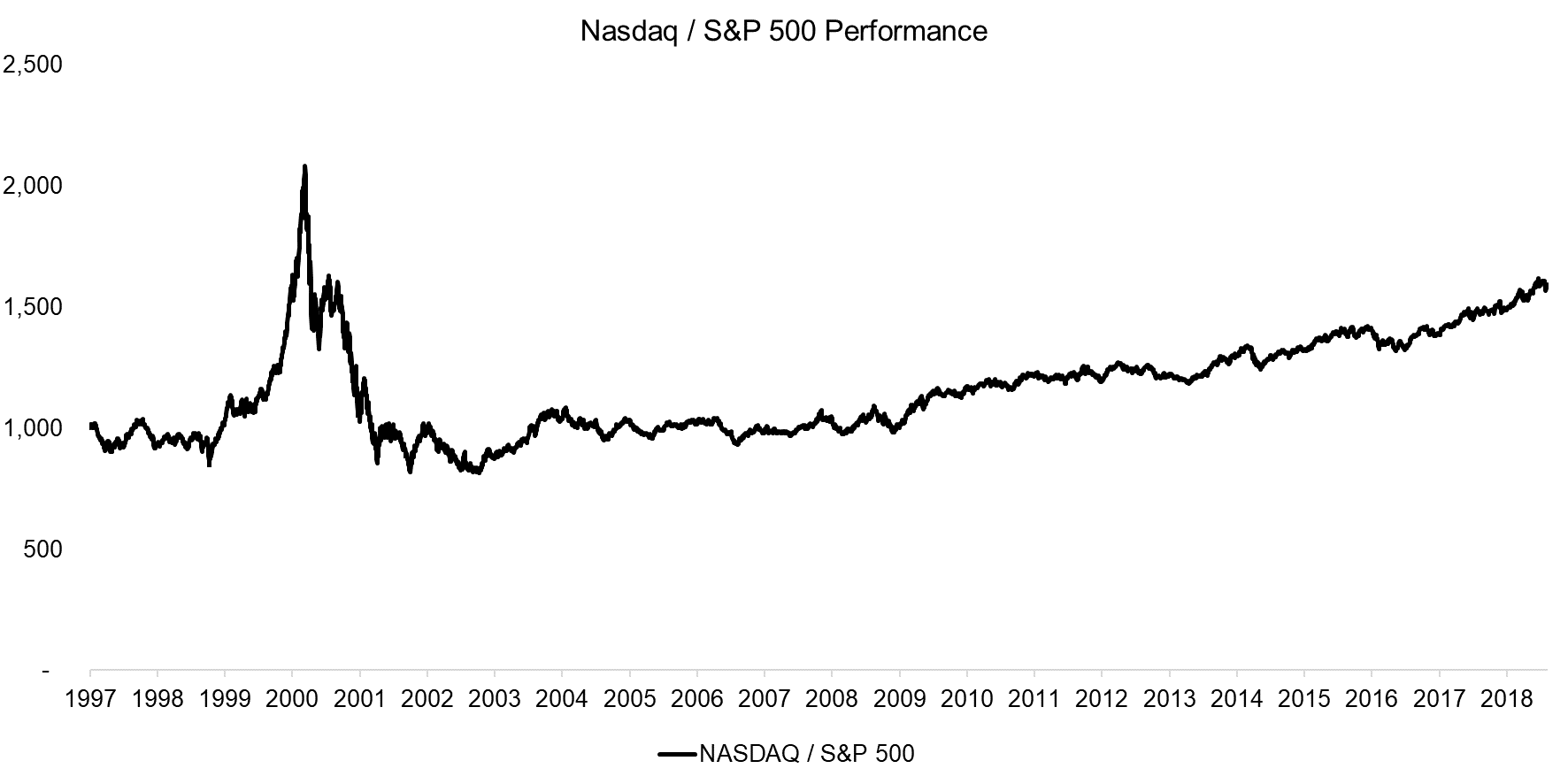

DOT-COM REDUX

Many investors are wary of technology stocks despite their strong performance over the last several years. The implosion of the dot-com bubble back in the early 2000s casts a long shadow.

Such fears may be overblown. The gains of the technology-heavy Nasdaq and the S&P 500 in recent years are more moderate than the rapid jumps seen at the turn of the millennium. That gives some reassurance that the situations are not quite analogous.

Source: FactorResearch

But if history doesn’t repeat, it still may rhyme. So just how crowded are technology stocks today, especially the powerful FAANG quintet of Facebook, Amazon, Apple, Netflix, and Google? After all, among its other lessons, the dot-com bubble illustrates the risks of crowded stocks. A sudden change in market sentiment can lead many investors to try and unload the same equities simultaneously. With few natural buyers left in the market, the losses can become amplified.

CROWDING METRICS

To measure crowding across the entire technology sector, we borrow a model that gauges the crowding of equity factors. Given the strong performance of technology stocks in recent years, many are currently included in the long momentum factor portfolio, which buys the winning and shorts the losing stocks. At certain times, the present among them, the momentum factor exhibits significant exposure to the technology sector and provides a useful means of comparison. The crowding model aims to identify when the technology sector or momentum factor is crowded, which is characterized by exhibiting more subsequent drawdowns than an uncrowded sector or factor.

Various methodologies measure crowding. Our approach focuses on market-derived metrics that are available daily or even intra-day. We combine five measures that indirectly reflect changes in the sector or factor and often indicate when significant inflows or outflows are occurring. They are:

- Residual Volatility

- Residual Correlation

- Residual Dispersion

- Valuation Difference to the Market

- Performance

All of these metrics correlate positively to crowding. That is, the higher the residual volatility or the larger the valuation difference to the market, the greater the likelihood that crowding is taking place.

We standardize the five metrics and combine them into one score. According to the model below, the technology sector was crowded in 2000 and in 2018. The momentum factor was also crowded in 2000, when it exhibited a significant exposure to the technology sector. It was crowded as well during the financial crisis in 2008 and in 2016.

Source: FactorResearch

We can investigate the effectiveness of this approach by analyzing the drawdowns of the momentum factor after measuring the crowding score. The analysis below demonstrates that a crowded factor is associated with higher subsequent drawdowns.

Source: FactorResearch

Applying the same methodology to the technology sector works too: A crowded sector exhibits more frequent subsequent drawdowns than an uncrowded one. These drawdowns are measured on a relative basis to the market.

Source: FactorResearch

CURRENT CROWDING SNAPSHOT

The score dashboard below provides a recent snapshot of all the summarized metrics and shows that both the technology sector and momentum factor were crowded, with positive scores on all metrics except for the correlation of technology stocks. The sector and factor appeared especially crowded on valuations, which may not be too surprising, while technology stocks were more volatile than usual. Momentum factor stocks also displayed higher dispersion than the norm.

Source: FactorResearch

Crowding is not negative for the performance of a factor or sector per se. After all, every investment needs some interest to generate performance. An uncrowded sector or factor demonstrates a lack of investor interest and thus is not especially attractive. The optimal state is between crowded and uncrowded, not too hot and not too cold.

FURTHER THOUGHTS

The recent sell-off in technology, especially among FAANG stocks, led to renewed comparisons of the tech sector today versus 2000. But the sector has matured and contains many highly profitable, stable businesses, so it is far less risky than two decades ago.

Current relative valuations are high but gauging sector risk with valuations is not a perfect science. Valuations can be elevated for long time periods, often much longer than most investors’ time horizons.

Investors are better off listening to multiple signals to measure portfolio risks.

INTERESTED IN FACTOR CROWDING?

Please see additional research on crowding of common equity factors like Value: Factor Crowding.

ABOUT THE AUTHOR

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Article by Factor Research