Almost 90% of Survey Respondents Report a Negative Mental Health Impact

We’ve all said it: these bills are driving me nuts, these prices are making me crazy, and the rent is pushing me off the deep end. Most of us don’t mean it literally (most of the time at least) but we might not be that far from the truth.

Even before the pandemic and the subsequent surge in inflation, significant numbers of Americans endured regular financial stress. The number has only grown greater since.

But how is this stress affecting the mental health of Americans, by their own perceptions? We recently ran a survey on the impact of inflation and asked questions designed to answer that question.

Q3 2022 hedge fund letters, conferences and more

Key Findings

- Roughly 90% of respondents reported negative mental health consequences from financial stress.

- Older and more affluent respondents reported negative consequences at a lower rate but large majorities still reported psychological stress.

- Most respondents reported feeling stressed, anxious, or worried.

- Paying bills was the largest single source of stress, followed by rising interest rates, debt payments, and affording food.

- Roughly 45% of Americans are reducing spending on maintaining both mental and physical health.

Survey: The Impact of Inflation on Mental Health

How do Americans perceive the impact of inflation on their own mental states? We decided to ask, and to keep it simple we focused on just three questions.

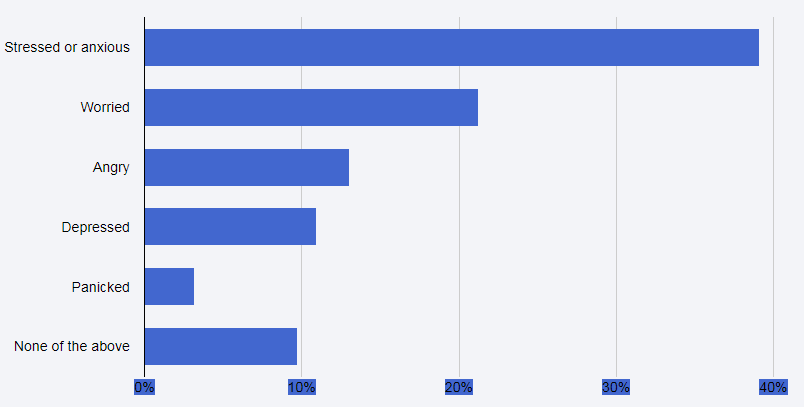

Over the Past Six Months, How Has the Rising Cost of Living Made You Feel?

Only 9.75% of respondents reported no psychological stress. That number was higher among those over 60 years old (22.51%) and those earning over $150,000 (15.69%), but in every case, it was a small minority.

Between 50% and 60% of respondents across all income brackets reported feeling worried, stressed, or anxious over their finances. 10% to 12% of all groups reported depression and between 10% and 20% reported anger.

Almost 5% selected “other”, with the most commonly cited cause being “all of the above”.

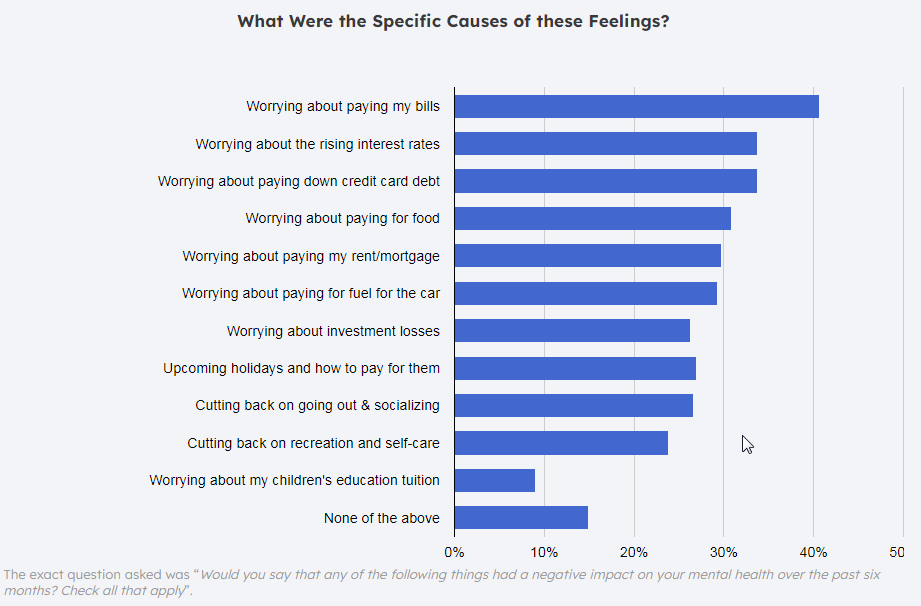

Many respondents selected more than one answer. Most people were directly concerned with basic necessities:

Many respondents selected more than one answer. Most people were directly concerned with basic necessities:

- 40.67% were concerned with paying bills,

- 30.86% were worried about being able to buy food,

- 29.24% were stressed over buying fuel for a car,

- 29.76% were troubled over housing costs (paying the rent or mortgage),

- 33.7% cited credit card debt as a source of stress.

There were distinct differences in the specific causes for concern among different income groups.

51.35% of those earning under $50,000 worried about paying bills, while 40.52% of those earning over $150,000 were stressed over investment losses.

Across all income groups, though, 20% to 35% worried about paying for fuel for the car, 25% to 40% worried about credit card debt, and 30% to 35% were affected by rising interest rates.

There was less variation by age group, though respondents over 60 were somewhat less concerned overall (22.51% selected “none of the above”, more than any other group) and most likely to be concerned over investment losses.

Overall, while older respondents and those with higher incomes expressed lower levels of stress, the levels reported were still quite high.

Are Americans Cutting Back on Coping Mechanisms?

Americans are more aware of mental health than ever before, and they have embraced a variety of responses, from therapy and medication to exercise and meditation. Many of these responses require money, adding additional financial stress.

We wondered if inflation was forcing Americans to reduce their spending on maintaining both mental and physical health, so we asked.

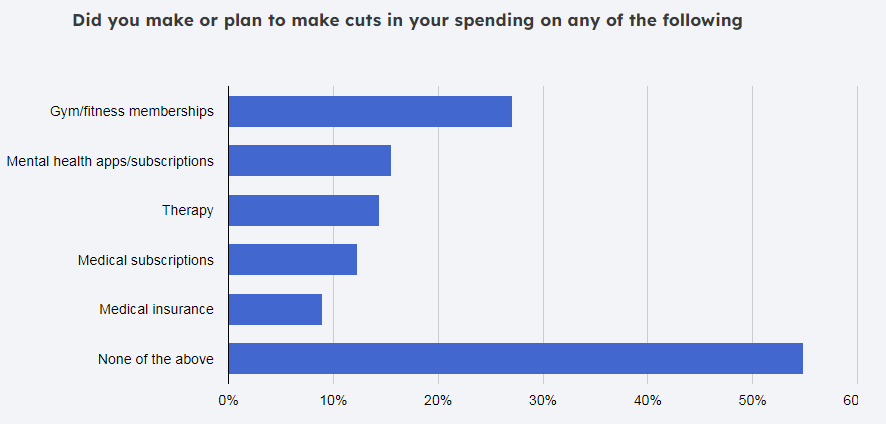

The answers indicate that our respondents place a high priority on this type of spending. 54.87% had no plans to cut back on any of these categories. 27.05% planned to cut back on gym or fitness memberships, 15.56% on mental health apps and subscriptions, and 14% on therapy.

The answers indicate that our respondents place a high priority on this type of spending. 54.87% had no plans to cut back on any of these categories. 27.05% planned to cut back on gym or fitness memberships, 15.56% on mental health apps and subscriptions, and 14% on therapy.

Only 8.97 % planned to reduce health insurance spending and 12.27% planned to reduce spending on medical subscriptions.

It’s important to recognize, of course, that only people who are currently spending on (for example) gym memberships or therapy can consider cutting back on this spending!

There were few differences by income. People earning over $150,000 were most likely to be cutting back on gym memberships (they may also be the ones most likely to have gym memberships) and least likely to cut back on therapy.

Respondents aged 18-45 were most likely to make some cuts in this area. 40% to 45% expected not to reduce spending, compared to 60% for ages 45-60 and 69.63% for those over 60. People over 60 are least likely to cut back on apps and subscription use, possibly because they are less likely to be using these services in the first place.

Article by Steve Rogers, Finmasters.