Tesla attracted such attention with its back to back earnings announcement and the Musk tweet that we wrote a short research paper analyzing the two news releases.

[timeless]

Q2 hedge fund letters, conference, scoops etc

The main takeaway is that analysis of such events should begin with a reverse engineered discounted cash flow model that relates projections of future cash flows to the current stock price. Those projections provide a point of reference for evaluating how stock prices should rationally respond to new information. (The details are explained and illustrated in the paper.) Using this approach, we conclude that the sharp Tesla price increase on the earnings announcement was not justified and that a buyout at $420 was highly unlikely.

Information Release and Stock Price Movements: The Tesla Earnings Announcement and the Musk Tweet

Introduction

On rare occasions individual observations of stock price movements are sufficiently informative that interesting insight can be gained even from single observations. The response of the market to Tesla’s earnings announcement on August 1, 2018 and the Elon Musk tweet on August 7 are prime examples.

After the market closed on August 1, Tesla reported financial results for the second quarter of 2018 followed by a conference call with analysts. Before the announcement, Tesla closed at $300.84. By the end of trading on August 2, Tesla had jumped to $349.54 – an increase of $48.70 or 16.2%. This was the largest daily percentage increase in Tesla’s stock price since December 2013. The market capitalization of the company rose by $8.16 billion dollars. The dramatic price increase raises the obvious question of what information was conveyed to justify the jump.

Next, on August 7 at 12:48 Eastern time, Elon Musk tweeted, Am considering taking Tesla private at $420. Funding secured. Prior to the tweet, the stock had closed at 341.99 August 6. Following the tweet, it rose 11.0% to close at 379.57 on August 7. Due to the chaos caused by the tweet trading was halted in Tesla between 2:08 and 3:45. Before turning to the details of those events, however, it is helpful to provide perspective by starting with a fundamental valuation model that relates the market price to the present value of future cash flows. For this exercise, we rely on the work of Prof. Aswath Damodaran who posts on his website detailed, and fully transparent, discounted cash flow valuation models for a variety of companies including Tesla.

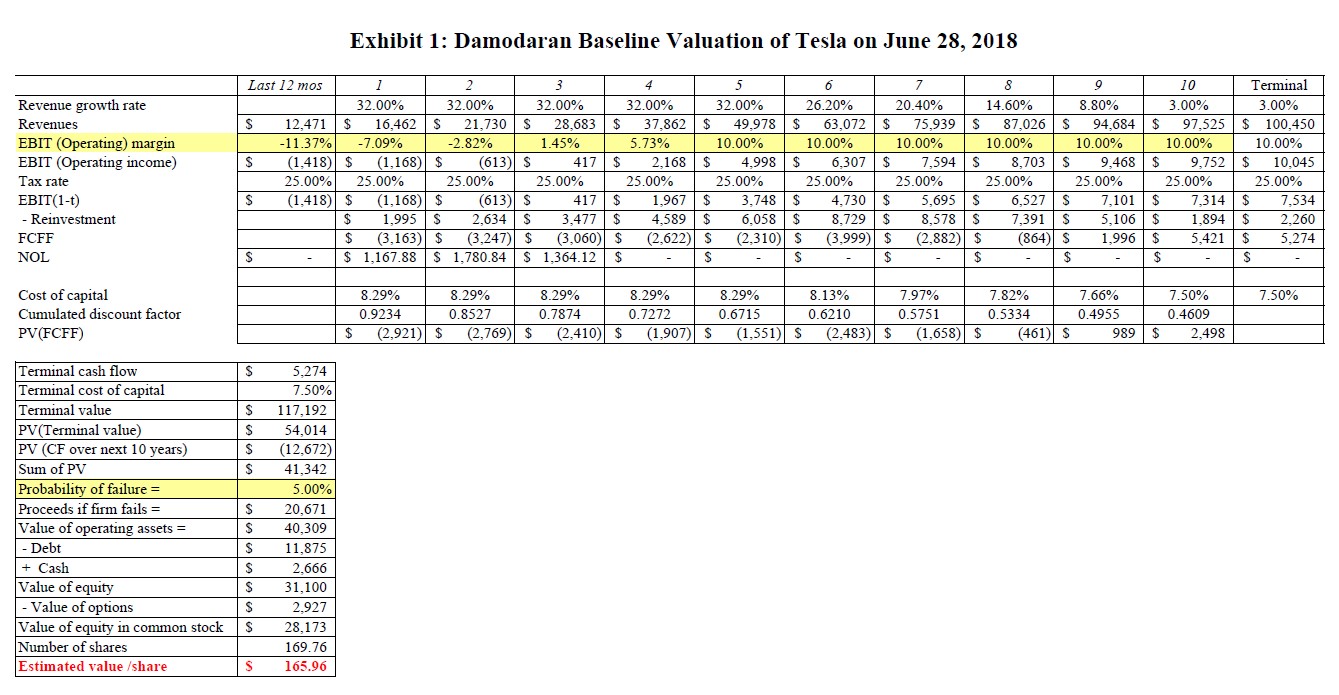

As of August 1, 2018, Prof. Damodaran’s most recent valuation of Tesla was posted on June 28, 2018. Prof. Damodaran is often referred to as a “Tesla bear” because at that time his estimated alue was $165.96 per share, barely half the price of the stock on August 1. However, examination of the model details reproduced in Exhibit 1 reveals that Prof. Damodaran was hardly pessimistic. In his model, Tesla’s revenues grow from $12.47 billion to $97.53 billion over the ten-year forecasting period – a compound growth rate of 22.8%. At the same time, operating margins improve from -11.4% to 10.0%. By comparison, among the ten largest auto manufacturers in the world, none had an operating margin of 10.0%. The highest was BMW at 9.9%. Thus, Prof. Damodaran was projecting both rapid revenue growth and dramatic improvement in margins to industry leading levels, hardly pessimistic assessment of the company.

In addition to his base model, Prof. Damodaran also posted what he called his “royal flush” scenario. This scenario employed what he believed were the most optimistic possible assumptions. His royal flush valuation came to $395.52. By combining the two sets of projections, it is possible to reverse engineer the market price of $300.84 on August 1, 2018. The result of that exercise is shown in Exhibit 2. Exhibit 2 makes three major changes to Exhibit 1. First, the revenue growth rates are increased so that the compound rate is now 25.1%. Second, the operating margins become positive more quickly and rise to 11.6%, well above that of Tesla’s competitors. Third, the probability of failure is reduced from 5% to 0%. With these changes to Damodaran’s baseline assumptions, the estimated share price comes to $300.91, seven cents greater than the market price.

Following Prof. Damodaran, in both Exhibits 1 and 2 the assumption is made that Tesla will maintain a sales-to-capital ratio approximately equal to that of its major competitors. This assumption is important because it determines the amount of reinvestment. It implies, contrary to statements by Mr. Musk, that as sales ramp up while operating cash flow remains meager, additional capital raises will be required.

It is helpful to pause for a minute to digest these projections. Elon Musk has been in an ongoing verbal battle with “Tesla shorts.” Mr. Musk’s comments often imply that he has concluded that the shorts view Tesla as a distressed company. While this may be true of some short sellers, it hardly needs to be the case. Look back, for example, at Damodaran’s baseline projections in Exhibit 1. They reflect a highly successful future for Tesla that is quite remarkable given the competitive and capital-intensive nature of the automobile industry. Damodaran projects a combination of both rapid growth in revenue and pronounced improvements in operating margins to industry leading levels, hardly the earmarks of a failing company. Nonetheless, his valuation of $165.96 implies that a rational investor should short the stock because his projections, optimistic as they may be, are significantly less optimistic than those impounded in the pre-announcement market price of $300.84.

The fundamental point is that the rationality of the market’s response to Tesla’s earnings announcement or Mr. Musk’s tweet cannot be analyzed in the abstract. They can only be assessed properly with reference to the projections already impounded in the market price prior to the announcements. With that in mind, we first turn to the earnings announcement.

Article by Brad Cornell’s Economics Blog