With shares 36% below last year’s highs, we believe an investment in Intelsat (NYSE: I) represents exceptional value ahead of important catalysts as the regulatory process enters its final stages. The bull thesis as laid out in our original, full-length report and subsequent Seeking Alpha article, All Systems “Go”, remains unchanged: The C band is extremely valuable spectrum and the C-Band Alliance (“CBA”) holds the keys to unlocking it.

Q4 hedge fund letters, conference, scoops etc

We believe international spectrum auctions suggest the C band is worth substantially more than the $0.21/MHz-pop implied in Intelsat’s current share price. In addition, what makes risk/reward particularly attractive are signs the CBA is winning support from key stakeholders, particularly AT&T, while continuing to lay the groundwork for secondary market agreements with interested parties.

Shares should be pricing in greater conviction on the value of the spectrum and the increasing probability of positive catalysts, not retracing levels visited 6 months ago. Our long-term price objective remains $151 per share.

Let’s Make a Deal

After months of negotiations with various parties, we believe the CBA has made material progress in determining the framework for secondary market transactions with one or multiple network providers. We believe general accord has been reached between interested parties on minimum price, the band plan for when and how declared spectrum will be made available, and operational details including exclusion zones and power levels. The level and detail of talks confirm the favored positioning of the CBA’s proposal among regulators and stakeholders, clearing the path to a deal announcement in mere days or weeks after a final Report and Order (“R&O”), or possibly before it.

The CBA’s interest in striking an agreement as soon as practical is anything but idle speculation. The topic of a framework deal, even before a final ruling, has been openly discussed at Intelsat investor presentations and earnings calls since last May.

Goldman Sachs Leverage Finance Conference transcript, May 10, 2018 (emphasis added):

Q – Jason K. Kim, Goldman Sachs Group Inc., Research Division>: Is there – what would prevent you from announcing some sort of a deal with a wireless carrier, supporting the deal sort of set it up and then support a broad framework of how this can work before the FCC gives a final ruling? Or is this even possible? Or would this not be a preferred route?

A – Jacques D. Kerrest, Executive VP & CFO, Intelsat>: I mean, it’s possible that it happens this way. We don’t know. It’s a little bit too early right now, but it’s possible that it happens this way. And because, as I said before, there are only going to be half a dozen parties involved here, and we can all sit down in a room and deal with it. And I mean, the FCC has given hints that something like this could happen. And I mean not in public, I understand, but in private conversations. And so we’d be ready to do that if we need to soon.

Intelsat 2Q 2018 Earnings Transcript (emphasis added):

A – Stephen Spengler, CEO, Intelsat>: Well, of course we are engaged with the interested parties now… In terms of how the process proceeds, you know I think it’s probably too early to speculate how things will transpire. We certainly want to see some clarity from the FCC… So I think we will see how this plays out in the coming months

Intelsat 3Q 2018 Earnings Transcript (emphasis added):

Q – Arun Seshadri, Credit Suisse>: And the second, just wanted to get a sense for, is there anything to preclude a transaction for a portion of the spectrum before the final order comes from the FCC?

A – Stephen Spengler, CEO, Intelsat>: And your last comment about timing. I think it’s still too early to comment about that in the sense that we are following the guidance and the direction of the FCC and the ultimate FCC order. And so how we proceed on that is something that we’re still assessing the best way to do that. Obviously, we want to make sure that we assess demand fully and there’s a transparent process for the market-based transactions. And so that’s important and it has to coincide with what the wishes of the FCC are.

Clearly, the CBA has been laying the groundwork for an eventual deal for some time. The size and complexity of any transaction has warranted engagement of a full array of advisors to build scenarios and negotiate tactics. In the opinion of a sell-side analyst we spoke with, the CBA is “up to its eyeballs” with advisors and the level of activity suggests to him that after many months of talks, the consortium has at least one counterparty and is engaged in a sales process that will not wait for a final R&O to begin.

But after months of negotiations, why are these conversations coming to a head now?

First, we believe the close of the formal comment period on December 11 was an important milestone. The process has now entered a period where all stakeholders must make a final

push to present to the Commission solutions rather than just talking points to influence final rulemaking. Though it is consensus that the CBA proposal enjoys preferred status at the FCC, the public record suggests there is still work to be done to get stakeholders on board.1 We believe the FCC views it as the responsibility of market participants, not regulators, to lead and hasten this effort. As Commissioner O’Rielly strongly warned in his statement last July, “It is of utmost importance that this proceeding is concluded, and spectrum is released into the marketplace quickly. There can be no unnecessary delays or distractions.” The month-long government shutdown certainly did not help. As we outlined in our original report, the Republican majority FCC is staffed by market-oriented reformers who want 5G spectrum repurposed quickly and believe in principles of regulatory humility. Attempts to provide the FCC an industry approved framework in advance of a final order would likely find favor with at least one commissioner, Commissioner O’Rielly, who believes market forces should guide spectrum allocation policy and there is no time to waste.

As a sign of the high priority the Commission has placed on repurposing the C-band, as well as its implicit support for the CBA, Commissioner O’Rielly held his first meeting on the issue with the consortium shortly after the government reopened on January 31. Later that day, Intelsat IR tweeted a link to an ex parte summarizing the meeting with the commissioner, but rather than simply addressing him by name she used the curious reference to meeting with “someone that likes bows.”

We believe this is because according to conversations with multiple individuals present in meetings with Commissioner O’Rielly last summer and fall, the commissioner likened the possibility of reviewing a secondary market transaction that precedes an R&O, to receiving a package with a “bow” on it.

While the support of a commissioner who has spearheaded the effort to repurpose the C band from inception certainly helps, to safeguard against a private auction being labeled as “backroom dealing,” the CBA must ensure market-based transactions are conducted with

fairness and transparency. The CBA has been noticeably stepping up efforts on these fronts since early December.

On December 8, the CBA filed reply comments that enshrine in the public record its intent to move swiftly: “The C-Band Alliance is also willing and able to negotiate the commercial and technical terms of SMAs [Secondary Market Agreements] that could be executed even before this rulemaking is complete – subject, of course to consummation after receipt of all government regulatory approvals…”

On December 20, the CBA filed in the docket a document titled “Early Sale Letter” sent to more than 300 parties identified as potential participants in the US 5G ecosystem. The letter invites interested parties to contact the CBA by January 11 to learn more about its market-based process. To defuse potential concern over competitive fairness, the Alliance made sure recipients included small, regional, and rural wireless carriers. According to Intelsat IR, at the same time the letter was sent, access to a data-room containing “standard asset sale” information was granted to parties that signed an NDA downloadable from the CBA website.

The explicit objective of these actions was to “put everyone on notice” and disarm arguments that adequate transparency, notice, and access regarding a transaction had not been provided by the CBA.

But what about potential counterparties to a deal – why would they wish to engage meaningfully with the CBA now? We believe part of that answer lies in the most significant development of the reply period. After expressing general ambivalence over the details of the process, AT&T introduced a proposal of its own on December 11 – one which underscores the need for a high level of CBA involvement, preserves crucial economic benefits to CBA members, and injects the plan with more FCC oversight.

Under AT&T’s proposal:

- C-band spectrum would be “allocated in an auction run by CBA according to well- established auction rules approved by the FCC.”

- The CBA would act as Transition Facilitator and initial drafter of a proposed Auction Plan, with interested parties able to provide input in a public comment period and the FCC acting as final arbiter.

- Of significant importance to Intelsat shareholders, the CBA will be paid all proceeds net of transition costs, pursuant to a Transition Plan:

Revenues from the auction would have to exceed aggregate transition costs, as reported in the Transition Plan, as well as auction costs, plus a reasonable premium…This establishes effectively a minimum aggregate bid for the CBA, but the premium, plus any proceeds above the aggregate revenue clearing level, would go to the CBA for distribution to its members, in a manner described in the Transition Plan (emphasis added)

A few key differences remain and determining an agreeable level of FCC oversight is not a trivial matter, but in speaking with a consortium member, the proposal represents “great strides”

toward the CBA proposal and the parties remain in “active negotiation.” Striking a compromise with AT&T that gets CBA members paid while addressing perceived weaknesses in the CBA proposal regarding oversight and transparency, would provide a game-changing level of industry buy-in and lobbying support from both a major wireless operator and content distributor.

As with any move by a competitor, we believe the potential for AT&T’s proposal to gain favor as an acceptable middle ground was met warily by Verizon. This is because FCC-like comment periods envisioned under AT&T’s plan would result in an extension of the reallocation timeline, a development which runs directly against Verizon’s interests. Verizon likely sees securing prime 5G spectrum, while competitors are preoccupied with recent and pending mergers and acquisitions, as a golden opportunity. With ambitious 5G deployment plans, limited mid-band spectrum holdings, and explicit interest in the C band, Verizon is a CBA supporter that is motivated to expedite the regulatory process and gain access to C-band spectrum in a way that plays to its temporal advantage.

Others have also picked up on strong signals that talks regarding commercial terms have advanced between the CBA and potential counterparties. No fewer than three brokerage firms – Jefferies, J.P. Morgan, and RBC – have all published notes in recent weeks using unusually strong and specific language in discussing the potential for near-term deal-making:

“We expect the CBA to at any moment decisively influence the FCC with the pre-emptive announcement of secondary market agreements for the spectrum with interested parties. This will be too hard for the FCC to ignore, in our view.”

– Giles Thorne (Jefferies, January 23, 2019)

“We think a potential pre-sale announcement, contingent upon FCC approval, could come in conjunction with earnings or shortly thereafter.”

– Michael Pace (J.P. Morgan, January 17, 2019)

“Obviously concluding the correct deal and the best price is paramount, but with the pace of developments being exceptionally quick, we suspect the CBA may harbor a desire to be able to announce a deal in time for Mobile World Congress (25-28 February).”

– Wilton Fry (RBC Capital Markets, January 14, 2019)

Regardless of whether a deal occurs before an R&O or immediately after, the most important takeaway is the high level of activity and interest that surrounds a CBA-led sales process. As Intelsat CEO Stephen Spengler stated last summer, “we’re engaged with the various parties now to make sure that we’re able to move [as] quickly as possible once we see all the criteria come together for execution.” With repurposing the C Band a key policy objective at the Commission, we believe a final R&O this summer remains a strong possibility and the regulatory process is entering a catalyst-rich final phase.

International Auction Results Support Significant Upside

The most referenced spectrum range for initial 5G deployments globally is the C band and adjacent frequencies (~3.4-3.9 GHz). Recently concluded auctions in Italy and Australia offer constructive read-throughs for the value to be unlocked here in the US. While mapping foreign prices to the US is not an exact science, there is an unmistakable pattern when comparing international prices for the same band: US prices are nearly always substantially higher. We believe C band in the US will be no different.

Italy

In October 2018, MiSE, the Italian equivalent of the FCC auctioned off 200 MHz of spectrum between 3600 and 3800 MHz for a final blended price of $0.41/MHz-pop – over 3x what Street analysts predicted pre-auction and a world record for national spectrum in the band (source: New Street Research). All four major nationwide operators – Telecom Italia, Vodafone, Wind Tre, and Iliad – ended up purchasing spectrum.

- Telecom Italia and Vodafone each paid ~$1.9bn ($0.40/MHz-pop) for an 80 MHz

- Wind Tre and Iliad each paid $554m (an even higher implied $0.46/MHz-pop) for a 20 MHz block.

As with every auction, the format and rules adopted play a significant role in determining price. In Italy, the allocation plan called for an uneven distribution of 2x80MHz blocks and 2x20MHz blocks preventing the possibility of an equitable split for all bidders. 3 bidders – Telecom Italia, Vodafone, and Wind Tre – ended up fighting for the 2 larger 80MHz blocks with each taking turns in the final rounds as end-of-day winners (source: see daily results from MiSE).

While auction structure is important, we would argue that no spectrum auction, no matter how cleverly designed (or poorly from the telco operator’s point of view) can generate high prices unless bidders also see compelling fundamental benefits to ownership of the frequencies. As the president of Italy’s communications regulator, Agcom, colorfully said in response to criticism of the auction, “If someone pays a price, to me it’s never excessive, unless that person has a gun pointed to their head.”

Examine the consequences bidders were willing to endure as a result of this auction and it’s apparent that rather than a “gun pointed at their head[s]” companies were given every reason to walk away and yet opted to engage in 14 days of intense bidding for fear of missing out. FOMO only works if there is something truly worth missing, which in this case is globally harmonized spectrum ideally suited for 5G. Though the price and absolute Euro amounts were low compared to US auctions, the near-term financial damage willing to be sustained was significant:

- Telecom Italia spent the equivalent of 16% of its market capitalization on its spectrum, all while its strategic direction was being sharply debated by warring shareholders.

- Before being outbid on the final day, Wind Tre, with total net leverage of 4.8x pre- auction, was prepared to spend over $1.7bn on an 80 MHz block, equivalent to almost 2x annual

- Following the auction, earnings estimates and price targets were cut across the board for Vodafone, Telecom Italia, and Iliad – stocks that were down -25-42% on the year before the event began (source: Bloomberg).

- Finally, lest one forget, the industry and macro environment for generating a return on large telecom infrastructure purchases in Italy is abysmal. Italy is one of the most competitively challenged telecom markets in Western Europe and the auction took place amid such gravely deteriorating fiscal conditions that observers were comparing the country’s predicament and systemic risk it posed to the Eurozone, to Greece in 2012.

While there are admittedly few relevant precedents in trying to compare Italian spectrum prices to US ones, in 2017 Italy renewed licenses for 1.8GHz spectrum at a price of ~$0.26/MHz-pop (source: New Street Research). Relatively similar paired AWS-3 spectrum in the US sold for 10x that amount in early 2015. Applying a 10x multiplier to just half the price paid recently in Italy, to conservatively allow for auction design distortions, still returns $2.05/MHz-pop for the implied value of American C band. We do not view $2.05/MHz-pop as a realistic expectation in the US given the sheer dollars involved, but it highlights the potential conservatism embedded in our estimate of $0.50/MHz-pop, which represents a modest 20% premium.

Australia

In December 2018, Australia auctioned off 125 MHz of 3.6 GHz spectrum for $853M (AUD), equivalent to $0.29/MHZ-pop (USD 0.21/MHz-pop). Four companies – Optus Mobile, Telstra, a JV between subsidiaries of TPG Telecom and Vodafone Hutchinson Australia (“Mobile JV”), and Dense Air Australia – purchased licenses. While below the USD 0.38/MHz-pop for similar 5G spectrum in Brisbane last year, (see our original report for more detail) headline results do not tell the full story:

- Pursuant to their August 2018 merger agreement, Vodafone Australia and TPG Telecom, the country’s 3rd and 4th largest mobile operators, participated as a JV, not separate entities.

- Significant restrictions were imposed on the top 2 potential bidders. Under the terms of the auction, the spectrum was broken into different areas, with companies allowed to purchase up to a 60 MHz limit in metropolitan and 80 MHz in regional areas. Optus Mobile, the nation’s #2 player, was barred entirely from bidding in potentially lucrative metro areas because it already exceeded imposed caps in every major city. Telstra, the nation’s largest wireless provider, was at the spectral limit in Sydney and Melbourne and ~50% below the limit in the rest of the metro areas.

- Australia’s National Broadband Network (NBN), a government owned wholesale-only network provider, was above imposed limits in all locations except some parts of Western Australia, and therefore also highly restricted in participating.

In the major metro areas (Sydney, Melbourne, Brisbane, Canberra) where Optus Mobile and Telstra were restricted, Mobile JV saw limited competition and opportunistically scooped up spectrum at the reserve price (USD 0.08/MHz-pop). Outside metro areas, where competition for licenses was more unrestrained, the average jumped to USD 0.53/MHz-pop. Had bidding not been expressly barred in metro areas for the two largest players, it is highly likely the overall price achieved would have been much higher.

AT&T’s Ability to Pay

One of the most frequent topics we encounter when speaking with investors is whether AT&T can afford to be a robust auction participant given balance sheet constraints following the Time Warner acquisition. Indeed, sitting two notches above non-investment grade, holding $180bn in corporate debt and confronting secular challenges across many of its operations, the ability to pay considerable sums for spectrum all at once appears limited for AT&T. But therein lies the misconception.

The CBA has near unlimited flexibility to structure payment terms over however long it wishes. Beyond perhaps an initial down payment, nothing material would likely be paid until 2021 based on a targeted 18-36 month clearing process post final order. Thus, the question regarding ability to pay should not be whether AT&T can spend $12bn in 2019; rather, can it spend $3bn per year from ~2021-2024 while de-levering the balance sheet? The answer to that is unequivocally “yes.”

In the context of a company that spends nearly $23bn in annual capex (more than half of which is on a declining wireline business), has forecasted $12bn in FCF after dividends in 2019, and has $500bn in total assets including “a large amount of office buildings and raw land that [they] have identified for potential sale”, coming up with $3bn per year is chump change. All else being equal, layering in $3bn in annual spectrum payments would offset the company’s medium-term net leverage by a mere ~.05x using Street forecasts.

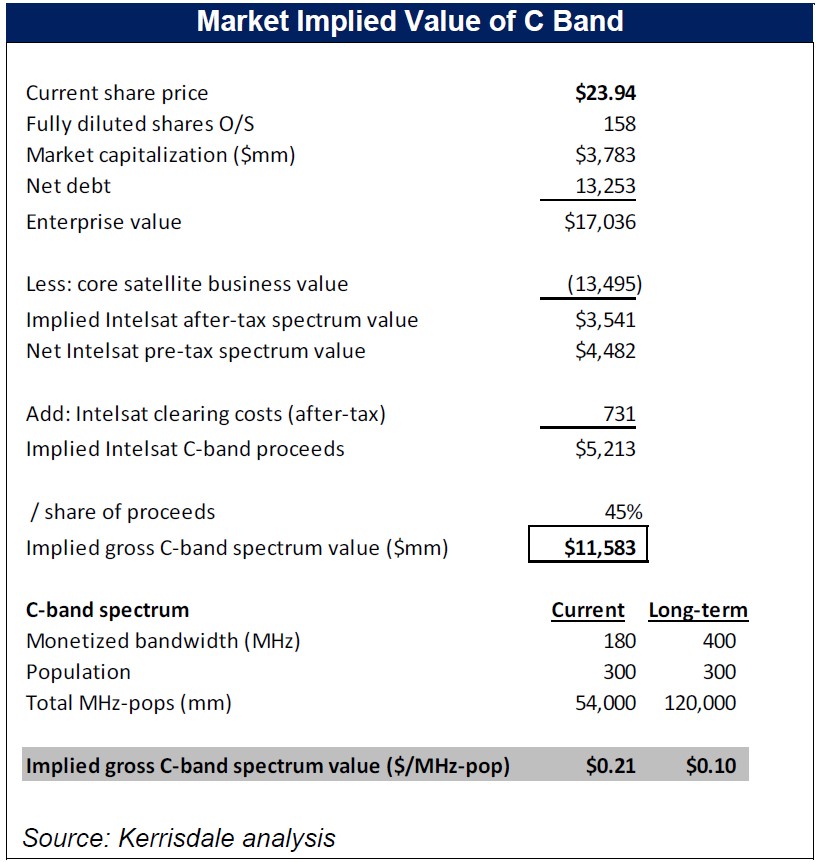

What is Implied in Intelsat Shares?

Despite the tendency of US spectrum to fetch substantial premiums to international prices, we estimate the market implied value of C-band spectrum embedded in Intelsat is roughly

$0.21/MHz-pop or ~$11.6bn in gross proceeds. This is 50% below 3.7 GHz pricing in Italy. The value and underlying assumptions we use for the core satellite business is little changed from our original report, with fractionally lower EBITDA offset by lower cash taxes. We estimate that as recently as mid-October, when shares reached $38, the market implied value for Intelsat’s C band was $0.33/MHz-pop. In our view, there has been no change in the value of the spectrum nor the ability of the operators to monetize it during this time.

While the market remains anchored to the current proposal to clear 200 MHz, we do not believe this will be the long-term end-state for the band. Rational economic principles will prevail: if bids for terrestrial use of additional spectrum beyond the first 200 MHz sufficiently outstrips the cost of clearing it and moving incumbent users elsewhere, then operators will have every reason to agree to a deal, develop innovative solutions to increase capacity or find alternatives as fiber proliferates, and free up more spectrum. Our core assumptions of $0.50/MHz-pop for 400 MHz of cleared spectrum as outlined in our original report remains the basis of our long-term price target of $151.

Article by Kerrisdale Capital Management