“In play there are two pleasures for your choosing; The one is winning and the other – losing. – Lord Byron, Don Juan

Q3 2019 hedge fund letters, conferences and more

Endeavors in the financial markets do not fall firmly on, but move fluidly between, extremes on the chance and design spectrum. At times, investment outcomes are a product of chance and design engaging in a competition. And at other times, they are a product of the two working together.

Chance pushes investors to look for predictions. Yet it is exactly the presence of chance that render predicting a futile effort.

Overemphasizing the role of chance

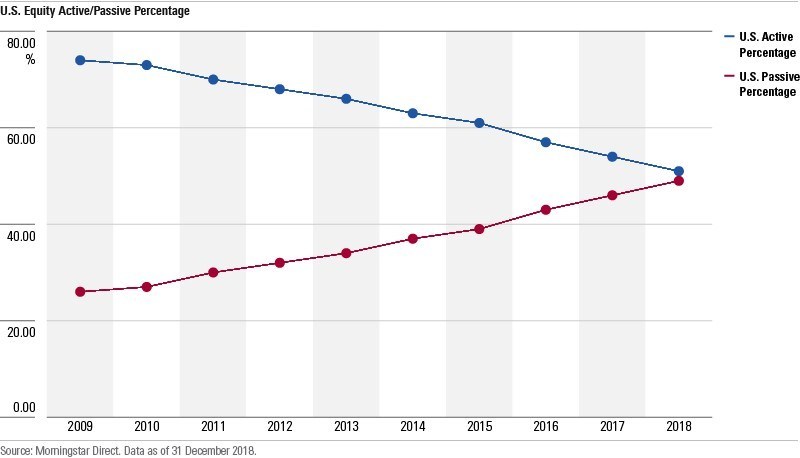

Another important attribute of investing is that it is further characterized by the presence of design. Interestingly though, most participants either completely ignore design or pursue it in a rather haphazard fashion. We are in the middle of an environment where Wall Street has sold the idea that design has no role to play in investment decisions making. Indeed, it has sold the idea rather successfully. As a result, an increasing proportion of investment flows have gone towards funds that focus exclusively on chance as the source of investment returns, i.e., passive funds and ETFs. As the chart below shows, over the past decade passively managed assets as a percentage of total U.S. equity assets has persistently risen at the expense of actively managed assets.

Source: Morningstar

Rational investor’s objective

As we stated earlier, the placement of financial endeavors in the chance and design spectrum is fluid. It is possible to shift the placement of one’s engagement further towards design via a rational decision-making process; that is the primary objective of a rational investor.

There are two primary ways of achieving that objective. Firstly, you may selectively choose your play. Within the financial markets, there are areas that are better suited to one’s skill levels. By sticking to those areas, one can shift the play out towards design. And secondly, by acting only when probabilities within your chosen area are stacked in your favor, one can further skew the system towards design. That process is similar to a poker player choosing which games to sit in on and once on the table, placing bets on only those hands where probabilities are favorable.

When Buffett said that he likes to shoot fish in a barrel and he likes to do it after the water has run out, he was referring to these two factors, i.e., choosing where to fish and when to fish.

Moving towards design – Defining our circle of competence

There are three areas of financial markets that are well suited to our investment process. Each of those areas represents a small fraction of the broader investment universe. Below, we offer a quick description of each of these baskets.

Moats. The first basket comprises of businesses with strong franchises that possess durable competitive advantages. These are businesses that Buffett refers to as moat businesses. In our own analysis, we find this population set to be under 150 businesses globally.

Advantaged asset owners. The second one is a set of businesses that own and/or operate assets that we consider to be of superior quality in terms of their desirability or in terms of cost competitiveness. Interestingly, we find this subset to be even smaller than that of the moat businesses set.

Emerging corporates. Lastly, there is a small group of businesses that are in what is likely to be the initial innings of their lifecycle. These are businesses that operate either in areas that are not addressed effectively, or the business is acting as a disruptor in a space where the customer is willing to switch. The businesses we look for have proven business models and the target market opportunity continues to be significantly larger in relation to the company’s current size. We refer to such businesses as emerging corporates.

Moving towards design – Favorable probabilities

The choice of areas that we operate in has the biggest impact on investment outcomes over extended periods. Limiting our actions only to those times when probabilities are favorable has the potential to enhance investment results as compared to that of the overall basket. There are three primary components to our process of identifying opportunities with superior probabilities.

Valuation. The first component is valuation. As Buffett said, price is what you pay; value is what you get. The idea is to ensure that we get more than what we paid. As opposed to being focused on traditional valuation metrics like price-to-earnings or price-to-book multiples or painting everything with the same brush of DCF, we focus our attention on the source of business value. For example, for earnings-power-based businesses, our preferred value at risk assessment metric is no-growth value and our preferred business valuation metric is DCF. On the other hand, for a business that derives its value from the ownership of assets, our preferred valuation metric is replacement cost of assets.

Fundamental momentum. Secondly, we look at fundamental momentum as a way of gauging whether the underlying business trends are favorable or unfavorable. For businesses that own durable franchises, it is about the relevant competitive metric. For example, we look at market share for a fragrance and flavors business like Givaudan and number of cards and number of transactions per card for a card network like Visa. On the other hand, for a business with low entry barriers, it is about understanding new capacities being setup or capacities being closed and their impact on the overall demand-supply situation.

Price momentum. Lastly, we look at price momentum as a way of gauging the sentiment of market participants around our intended investments.

Rational investor’s choice

In a world where much of the market is shifting towards passive investment products, a rational investor will do well to push further towards the design spectrum. This is where we have positioned ourselves and that’s the play we have chosen.

In the following section, we offer a quick summary of the current investment pricing environment, the impact of investment flows unconcerned with valuations on investment pricing, and our consequent investment positioning.

Investment environment

The increasing allocation to passively managed investment products accentuates investment mispricing. Much of the money flowing into passive investment products ends up in the same group of large-cap names. Investors, while they think that they are appropriately diversified because they have invested in different style products, actually end up with significant over-allocation to those names. As investment flows to such products continue, those same names see more buying interest.

It is not hard to imagine the outcome of such a process – the spread between cheap and expensive will end up in more extreme territory than was seen before. Indeed, that’s exactly the outcome we are currently seeing. As seen in the chart below, value has had the worst decade compared to growth in its entire recorded history.

Source: US Research Returns Data, French/Fama 3 Factors

Equity markets and sectors that are priced for superior long-term returns (e.g., a select group of emerging and non-U.S. equities) have continued to put up relatively poor performance compared to their more expensive counterparts.

Investment allocation in such an environment

As investors focused on moats, our “where to fish zone” is given. In terms of when to fish, there are times when our overall investment basket is priced for high investment returns. The years 2009 and 2012 represented such times when the overall global moats index (GMI) was priced for healthy investment outcomes. Then there are times when the overall basket isn’t priced for a healthy outcome, but a select few businesses are. We are currently in the midst of such an environment.

As valuation-driven investors, we take comfort in the fact that in these times when broader equity markets are priced for poor expected returns, value-insensitive investment allocations are allowing us to construct portfolios that have healthy expected returns over the long-term.

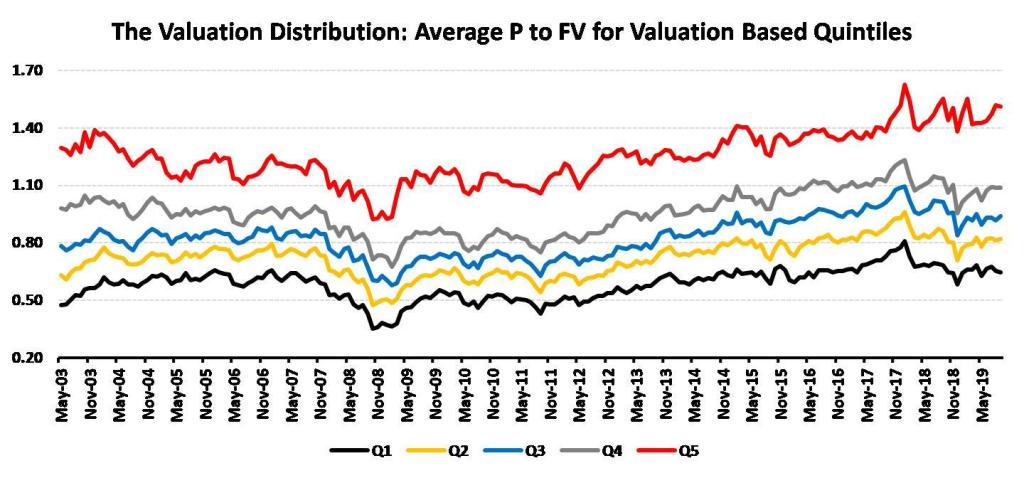

To that point, the chart below shows what we refer to as the valuation distribution[1]. The average price-to-fair value ratios for each of the quintiles has persistently risen over the past decade. Indeed, the average valuation ratio for the most expensive quintile (Q5) has risen to a level well above that before 2008. Valuations of the cheapest quintile (Q1) continues to be well below those levels. There is a rather wide spread between Q1 and Q5 allowing us to construct superior portfolios.

Summary

We are positioned as investors who persistently push themselves to the design side of the chance and design spectrum. Our primary mechanism to achieve that objective is to limit ourselves to a small subset of businesses that generate superior underlying returns on capital, driven either by business franchises or by ownership of advantaged assets. Valuation is the primary factor that helps us improve upon our probability of superior investment outcomes.

A defining characteristic of the markets, over the past decade, has been the big shift in asset flows from active to passive investment strategies. This is fanning extreme pricing. As the valuation distribution has widened, we have been positioning the fund towards investment opportunities where we expect to earn satisfactory investment returns.

[1] To construct the chart, we calculated the price to fair value of each company in the Global Moats Index on a monthly basis. The index was then segmented in quintiles based on the price to fair value ratio. The chart plots the average of price to fair value ratios so calculated for each one of the quintiles.

Article by Baijnath Ramraika, CFA – Symantaka