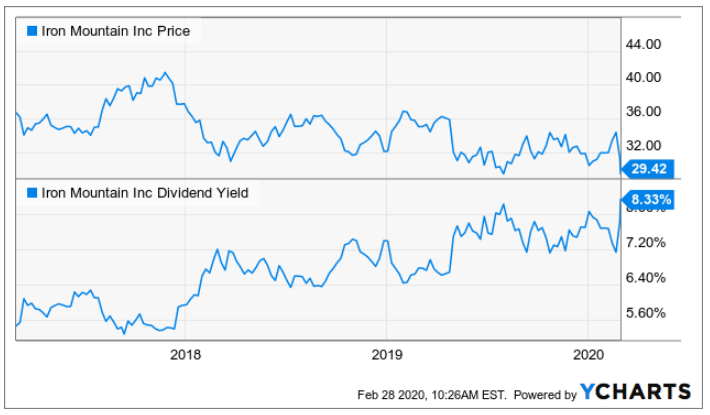

The recent indiscriminate market plunge has driven Iron Mountain’s (IRM) price sharply lower and its dividend yield sharply higher. Despite broad market actions, Iron Mountain has its own unique set of risks, such as the capital intensive nature of its business and management’s efforts to transition the company’s strategy (they’re working to diversify into growth areas). Iron Mountain has also taken on a significant amount of debt to support its transitioning growth strategy. This article reviews the health of the business, valuation, risks, dividend safety, and concludes with our opinion on whether the recent price plunge tips the risk versus reward trade-off in favor of income-focused investors enough to warrant investing at this time.

Q4 2019 hedge fund letters, conferences and more

Overview:

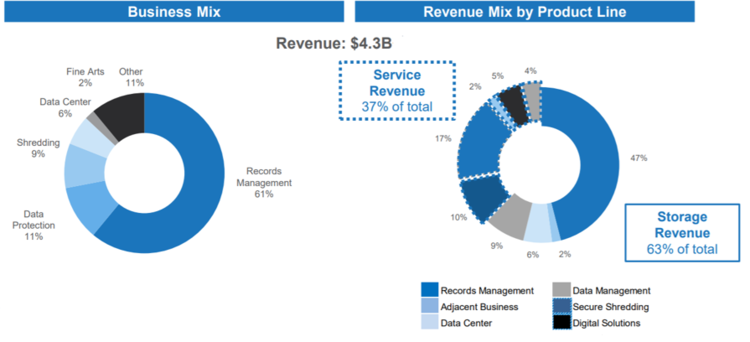

Iron Mountain operates as a REIT, and it is the global market leader in physical storage and document retrieval. It also provides additional services including data protection, data management, digital solutions, shredding and data centers. It operates more than 91 million square feet of storage space in nearly 1,450 facilities located in 50 countries. In total Iron Mountain serves more than 225,000 global customers, including 95% of the Fortune 1000.

The storage business generates the majority of revenue (~63% in 2019) and gross profits. Historically, the storage management business has seen strong customer retention at ~98% and solid physical records retention (>50% of physical records were stored more than 15 years ago). However, with the physical storage business maturing in developed markets and customers transitioning to digital, IRM is also trying to expand into faster growing geographies and verticals.

(source: Company Presentation)

Diversifying into growth areas

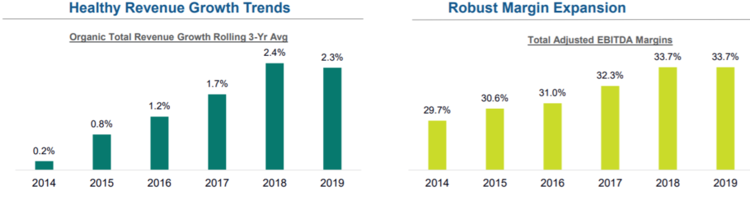

In recent years, Iron Mountain has made significant progress in shifting its revenue mix to faster growing businesses, including emerging markets, data centers, and adjacent business segments (such as entertainment and fine art storage). The shift in business mix has resulted in higher organic growth and continued improvement in adjusted EBITDA margins (as shown in figure below). The faster-growing geographies are expected to be ~20% of the records management business in 2020 (versus ~10% in 2013). Also, 2019 was a record year for the global digital solutions business, with revenue increasing 10% year-over-year.

Potentially, the most important growth driver for Iron Mountain is its data center operations, which currently account for ~8.5% of total EBITDA, and is expected to reach ~10% in 2020. The company has made several data center acquisitions including Fortrust, I/O, Credit Suisse, and EvoSwitch. It currently operates 14 data centers across 13 global markets with a presence in nine of the top 10 US markets and three of the top 10 international markets. Five of the top 10 global cloud providers are IRM’s Data Center customers.

Iron Mountain also plans to invest heavily in the coming years, nearly tripling its overall data center storage capacity organically (~120 MW to 357 MW). Data center development capex was approximately $400 million for the full year 2019. In 2020, it expects development capex of ~$200 million, reflecting the development projects currently under way.

Business Mix Accelerating Growth

(source: Company Presentation)

Limited financial flexibility impacts dividend safety

The company has limited financial flexibility given its already high debt. The leverage at the end of 2019 was 5.7x and is expected to remain flat to slightly down in 2020. This is well above its long-term target of 4.5x-5.5x. The company’s leverage profile is riskier than the average REIT’s leading to a junk credit rating of BB- from Standard & Poor’s. This leads to higher cost of capital and difficulty in raising capital. Importantly, a lack of access to capital can significantly impact IRM’s ability to sustain and grow its dividend.

The firm’s AFFO was $856 million in 2019 and payout ratio was 82%, a reasonably safe level in most cases. This left ~$150 million in retained cash flow to fund the REIT’s growth plans in 2019, which totaled $693 million largely due to data center investments and acquisitions. This meant that majority of growth had to be financed via debt which is common for a REIT, but somewhat concerning for IRM considering its already high debt level and high cost of capital.

And into 2020, the situation remains largely the same. IRM is guiding for AFFO in the range of $930-$960 million. Assuming zero dividend increase would still mean just over ~$240 million in cash flows to fund its growth plans for 2020 which are around $650 million as guided by management. This large shortfall will again have to funded via the capital markets. And given the already high leverage, we see it will be challenging for IRM.

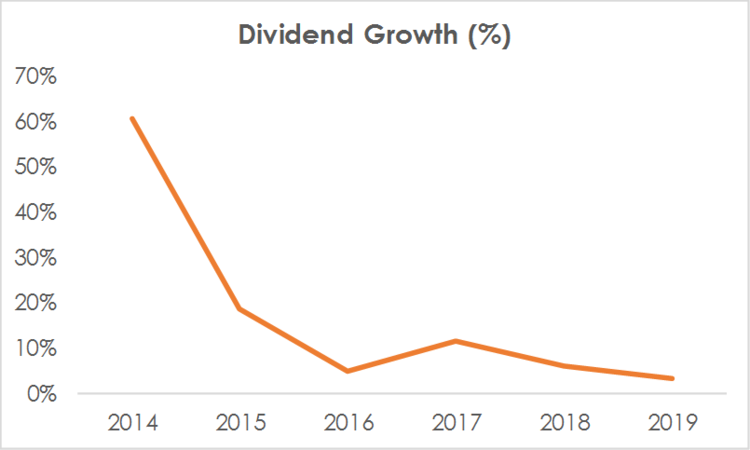

Further growth has been slowing in recent years. IRM raised its annual dividend by 11.6% in 2017, 6.1% in 2018, and only 3.2% in 2019. Management has already guided for reducing its AFFO payout ratio to mid-60s to low-70s range. While IRM has a solid core storage business that produces steady cash flow, limited growth prospects and the capital intensive nature of the business leaves little room for error. This could eventually put pressure on management to reduce the dividend if growth investments fall short of expectations. Essentially, management is betting big on its transition plans, and will face significant challenges if they fall short.

Dividend growth slowing

(source: Company Data)

Valuation:

On a Price to Adjusted Funds from Operations (“AFFO”) basis, IRM is trading at ~10.5x its 2020E AFFO. Since the company has no direct peers, we compare it to data center and industrial REITs. The data center REITs (such as Digital Realty Trust (DLR) and Equinix (EQIX)) are trading in the range of 17x-25x, while industrial REITs (Duke Realty (DRE), Eastgroup Properties (EGP), Prologis (PLD)) trade in the range of 27x-29x. Based on this, IRM appears inexpensive, but that view must be tempered by the unique and significant risks as described above (which are reflected in the valuation). The high dividend yield, as compared to other REITs, is also an indication of higher risk.

Risks:

High debt: The company’s debt remains high, which increases risk, given the inherent capital intensive nature of the business. It also increases interest expense putting pressure on earnings and cash flow. While deleveraging remains a priority for management, we see limited options to achieve this goal other than successfully executing on its growth strategy.

Lack of organic growth: The physical storage business (more than 60% of IRM’s revenue) is low growth, as clients transition to digital. While the company is working to transition to more digital businesses (including data centers) the fact remains that these growth initiatives are still relatively small in size. Also, these growth businesses require significant capex. If the company fails to achieve the scale and competitive advantages it seeks in data centers, it will create further challenges for the business.

Conclusion:

Iron Mountain’s 8.3% dividend yield is compelling, but it comes with risks. For example the company is hampered by a low growth physical storage business and an already stretched balance sheet. However, the company is making significant progress in transitioning a growing portion of its business into higher organic growth areas, such as data centers. Further, the recent share price plunge provides an increasingly compelling entry point (in terms of price and dividend yield) to compensate investors for the risks. If you are looking to opportunistically take advantage of the recent market wide sell off, IRM is worth considering for a spot in your prudently-diversified, goal-focused, income-oriented investment portfolio.

Article by Blue Harbinger