July 4, 2019: This month’s blog will show the daily thinking process that we go through at MarketCycle Wealth Management and also at our paid membership site: MarketCycle Wealth REPORT (link below).

Q2 hedge fund letters, conference, scoops etc

PORTFOLIO CHANGES:

Gold is likely to gain as late-stage inflation begins to pick up from exceptionally low current levels. Gold also helps during times of increased risk. Despite any near-term and temporary pretend trade deal (that merely ‘kicks the can further down the road’) risk deflecting assets will still be needed, as shown later in this blog. In mid-June, on the day before GOLD (strongly) broke out of its 5 year consolidation pattern, MarketCycle took a 5% position in a relatively unknown gold trust with the stock symbol of “PHYS” and we picked this trust over the popular ETF of “GLD” because:

- Unlike GLD, it holds actual gold bullion in the (very safe) Central Bank of Canada.

- Unlike GLD, if the stuff hits the fan, shares can be redeemed for the actual gold bullion.

- Unlike GLD, it pays interest (and is the only non-option gold bullion asset to do so).

- Unlike GLD, it does not generate a complicated (and always late) K-1 tax form.

- Unlike GLD, it generates half of the amount of capital gains tax than does GLD.

- PHYS will benefit from the Federal Reserve stopping or eventually reversing its interest rate tightening.

- PHYS will act as an anti-risk asset during increased volatility and rising recession probabilities.

- The parent company is very strong and the asset is highly liquid.

MarketCycle also took a 5% position in a relatively unknown, diversified (CEF) Closed-End-Fund (MLP) Master-Limited-Partnership with the stock symbol “FEI” because:

- It leverages the interest rate section of the MLP which allows it to generate 11% in interest on top of capital gains.

- It has a discounted (NAV) net-asset-value which may allow it to gain more than the stock market as we move into the end of this market cycle. It is under-priced.

- Energy stocks and MLPs usually gain after the yield-curve has inverted, like now. FEI contains both.

- The parent company is very strong and the asset is liquid.

- Because this MLP is actually a Closed-End-Fund, it also does not generate a K-1 tax form.

Although this REPORT states that we are still in a bull market, MarketCycle’s global client accounts are currently positioned to profit in a market that could go in any direction and we are holding highly select assets and reaping a lot of dividends and high interest levels. We are allocated the most defensive of any time since late 2007 although we are not currently positioned for an economic recession. At times like this, I hear the old saying somewhere in the back of my brain: “Do not fire until you see the whites of their eyes.”

Although 2019’s late-stage risk is obviously rapidly increasing, technical analysis gives us a near-term S&P-500 target of 3030. And if we do get the typical final euphoric melt-up, perhaps from the Federal Reserve being very aggressive with rate cuts (more below), then it might even temporarily hit 3300 within the next 6-9 months, but it would then likely die a slow and lingering death. In today’s volatile times, these price projections could be wrong and the potential downside is now larger than is the potential upside. And if it heads higher, then it might, unusually, be fairly defensive sectors and factors that will lead higher. Like a boiling pot, the market requires constant watching… even more so than usual.

MarketCycle Wealth Management’s client accounts have been beating the market on most up days and also beating on most down days, and we hold more than 50% less risk than does the S%P-500. As I type this sentence today, the market is up a lot, but we are beating by 2x and with very much less risk. We are also pulling in a lot of dividends and high interest that quietly flow (on a monthly basis) into our accounts. So, all of that makes me happy.

MarketCycle Wealth REPORT

July 4, 2019

Important note about the REPORT signals: The individual asset signals shown below are determined by combining the following 8 criteria…

- The trend direction of the individual asset

- Relative strength of the individual asset

- Where we are in the current market cycle

- Where we are in the longer-term secular cycles

- Global Central Bank activity

- Global currency relative strength and trends

- Accelerated inflation data

- Accelerated economic data

STOCKS…

United States: BULLISH

Developed Markets (ex-U.S.): AVOID

Japan: AVOID

Emerging Markets (commodity producers): AVOID

China: AVOID

India: BULLISH

Global private equity: BULLISH

- SECULAR U.S. stock outlook (effective October 1, 2011): Bull markets will be stronger than usual

- SECULAR Emerging Market stock outlook: Bear markets will be more severe than usual

BONDS…

U.S. Treasury-bond, 30 year: BULLISH

U.S. Treasury-bond, 10 year: BULLISH

U.S. fixed-rate corporate bonds: BULLISH

U.S. floating-rate assets (and TIPS): CAUTION

U.S. high-yield corporate bonds: BULLISH

U.S. preferred shares: CAUTION

Emerging Market high-yield bonds: BULLISH

- SECULAR fixed-rate outlook: Bear markets will be more severe than usual.

COMMODITIES…

Gold: BULLISH

Oil & energy: BULLISH

Industrial metals: CAUTION

Lumber: CAUTION

U.S. home price appreciation: CAUTION

- SECULAR commodity outlook (effective October 1, 2011): Commodity bear markets will be more severe than usual

CURRENCIES…

U.S. Dollar: BULLISH

Euro: BEARISH

Yen: BULLISH

Emerging Market currencies: BULLISH

RISK ASSESSMENT…

- Calculated future U.S. economic-RECESSION probabilities (markets can correct without being in recession): BULLISH

- Global (ex-U.S.) Economic Contraction Risk Indicator: WARNING

- U.S. Federal Reserve’s Survey of Professional Forecasters: BULLISH

- Are energy costs HIGH enough to crush the economy? NO

- Are energy costs LOW enough to stimulate the economy? NO

- Number of Hindenburg Double Omens within past 6 months: NONE

- High-yield to T-bonds – price divergence: WARNING

- High-yield to T-bonds – spread: WARNING

- S&P-500 to T-bonds – spread: WARNING

- Global (ex-U.S.) stocks to T-bonds – spread: WARNING

- Percent of S&P-500 stocks above-to-below the 200 SMA – divergence: WARNING

- Small-cap to large-cap divergence: WARNING

- Dow Theory divergence: WARNING

- Home construction divergence (triggers early): WARNING

- Lumber price divergence (triggers early): WARNING

- Copper price divergence: WARNING

- Direction of 200 Day Moving Average: BULLISH (showing weakness)

- Cyclically Adjusted Price-to-Earnings Valuation Ratio: WARNING

- Warren Buffett Valuation Metric: WARNING

- Q-Ratio Valuation Metric: WARNING

- U.S. 3-month:10-year interest rate yield-curve: WARNING

- Likely future direction of U.S. interest rates: FLAT then DOWN

- 12 month trend of inflation levels: DEFLATIONARY

- Inflation/Deflation Extremes Indicator: DEFLATION

- Volatility trading-range: WARNING

- U.S. Leading Economic Indicators EXPANSION or CONTRACTION: CONTRACTION

- U.S. stock market combined SEASONALS (updated monthly): CAUTION

- ∗∗ Calculated chance of a near-term U.S. stock market CORRECTION (a multi-month 10-30% loss): above AVERAGE

- ∗∗ Calculated chance of a near-term U.S. stock market RECESSION (a year-long 20-50% loss): LOW (U.S. recessions usually lead to global recessions, but not vice versa.)

- ∗∗ Calculated chance of a global DEPRESSION (a multi-year 50%+ loss): NONE (Depressions are always global.)

- Minor OVERSOLD Indicator most recent buy-the-dip date: December 26, 2018

- Major OVERSOLD Indicator most recent buy-the-dip date: December 26, 2018

- U.S. SECULAR THEME… “MY” Ratio (investing demographics) is bullish until 2029

- U.S. very-long-term SECULAR THEME… inflation or deflation: INFLATION

We are still BULLISH, but global economic weakness plus the current risk existing within market internals are both increasing exponentially. This can be visualized by comparing the amount of GREEN to RED above. The above RISK ASSESSMENT area has been totally green or mostly green since early 2009… at least until the period that started 3 months ago. What could prolong the bull market? The Federal Reserve lowering interest rates aggressively.

Historically, 1995 was very similar to today. Back then as now, the catalyst for trouble was high stock market valuations combined with increased risk and unusual late-stage falling inflation levels. The Federal Reserve then embarked on a series of three rapid interest rate cuts (total of 75 basis points) and the stock market pulled out of its risk period (after 7 months) and moved forward for another five years (before suffering major losses from 2000-2003). So, if the Federal Reserve were to cut 75 basis points before the end of 2019, they might pull off the same thing and create another soft-landing for the economy, just as they did in 1995. The market itself may already see this and it may explain why MarketCycle is seeing high risk at the same time as low recession probabilities. Today the market is pricing in the chance of a late July rate cut at 100% and if it doesn’t happen, and it may not, then the market will not like it.

WHY IS THE Federal Reserve hinting about lowering rates? The Federal Reserve would lower interest rates in response to the falling inflation of the past 15 months, and that they just recently noticed. MarketCycle’s proprietary accelerated inflation indicators suggest that the past 15 months of falling inflation might soon be over. If so, the Fed would not see the new inflationary trend until January of 2020. We will know whether the change is confirmed & valid by the end of this month. What is still pulling on the other end of the rope is the fact that the job market remains strong. The Fed has a dual mandate to avoid deflation and to promote job numbers. So, would the Federal Reserve be correct if they actually do lower interest rates rather than just sitting on their hands and doing nothing right now? Well, as Winnie The Pooh taught us: “Doing nothing leads to the very best of some things.”

SUMMARY: We are still in a bull market for U.S. stocks. Stocks could have another 10% upside if the Fed does 3 rapid rate cuts before year-end. Regardless, the Federal Reserve is likely done with raising interest rates because of the exceedingly low and falling inflation of the past 15 months. Defensive factors and sectors still lead in relative strength. Risk has increased in the near term and MarketCycle’s client accounts are in safety mode. However, economic-recession probabilities within the next 3 months remain below 4% which is still quite low. So, conditions must be monitored daily and portfolio protection is now a must regardless of any remaining upside.

Chart posted on July 4, 2019. You can clearly see how difficult and volatile the past two years have been:

Cornerstone Macro Analysis came out in mid-June promoting exactly what MarketCycle has been saying for the past half year. They are suggesting the defensive “TRUMP” trade. We would now add Master Limited Partnerships to the list since the Fed is becoming more accommodative… and we also like using a barbell approach to any corporate bonds in one’s portfolio (basically, an equal mix of high-yield and high-quality).

- T reasury-bonds

- R EITS

- U tility stocks

- M omentum defensive stocks

- P recious Metals (gold)

July 1, 2019 CNBC headline that warns about upcoming corporate earnings (this strongly affects stocks):

For the past year I’ve been repeating that home prices would start to follow home construction DOWN. (CNBC headline image from July 2, 2019):

Where does market danger exist? Corporate debt, particularly in China & Hong Kong and in the central & northern parts of Europe presents the problem. Low interest rates have encouraged excessive and dangerous corporate debt levels (as %-of-GDP) even in the normally fiscally responsible countries of Canada, Norway, Netherlands and Switzerland. This easy access to cheap money allows for the temporary survival of zombie corporations (that would normally already be dead and buried) and for the artificial propping up of the entire stock market via continual stock buy-backs. EVEN MORE IMPORTANT: The truly gigantic global government debt bubble and the $1-Quadrillion(!) derivatives market will likely not start to implode for another 15 years (yes, there is even a way to protect investors from that disaster!).

War with Iran? President Trump’s closest military adviser, John Bolton, never saw military service, but has been chomping at the bit to bomb Iran for several decades now. That seems to be his main focus in life. But Iran is not Iraq. It is the 14th most powerful military in the world and it is armed to the teeth, as evidenced by its ability to take out a U.S. un-manned $150-Million drone with one missile. It has a million person military. Iran is allied with Russia and China. China recently said that it would side with Iran in any war. Naturally, Russia would do the same. Israel and Saudi (ruled) Arabia would side with the United States. There is an outside chance that war could quickly escalate. Economically, oil disruption would likely cause a 30% leap in oil prices, completely crippling the global economy.

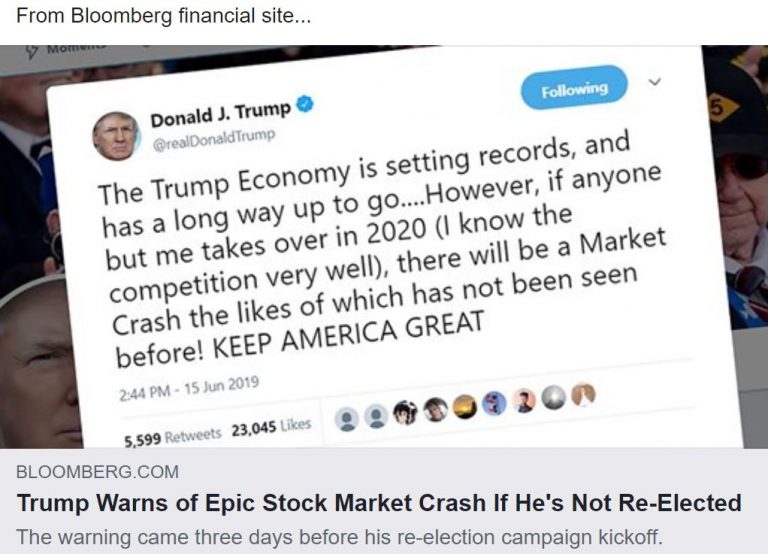

Currency war? President Trump’s Trade War might progress to currencies, especially if he is voted in for a second 4-year term. In my opinion, temporarily owning some gold in one’s investment account may offer protection against protectionist shenanigans and also money-printing.

Bloomberg financial site reports that India is imposing retaliatory trade tariffs on the United States effective on June 16, 2019… the Trade War is spreading:

On Wednesday, June 26th in a Fox interview, President Trump was told that many manufacturers are now moving production to Vietnam because of his trade war with China. His response was that he will likely now put trade tariffs on Vietnam:

JOKES & more added down BELOW…

We do not advertise. If you like what you see, please share and tell others.

MarketCycle Wealth Management is in the business of safely navigating your investment account through rough waters. The entire process of setting up with MarketCycle is easy and the first 3 months are at no charge.

You can SUBSCRIBE to this free, no-spam MONTHLY blog via the website… first click on the “HOME” tab and then find the signup on the right or bottom.

The LINK for the REPORT website: https://MarketCycleWealthREPORT.com/

Graham & Dodd: “The essence of investment management is the management of risks, not the management of returns.”

Ralph Wagoner: “The market is like an excitable dog on a very long leash in New York City, darting randomly in every direction. The dog’s owner, who ultimately determines the primary direction (trend), is walking from Columbus Circle, through Central Park, to the Metropolitan Museum. At any one moment there is no predicting which way the pooch will lurch. But in the long run, you know he’s heading northeast at an average speed of three miles per hour. What is astonishing is that almost all of the market players, big and small, seem to have their eye on the dog and not the owner.”

On June 27th, President Trump announced that he wants to slash the taxes on capital gains for investments held in investment accounts for over one year. He plans to use an Executive Order in order to bypass Congress. This would create a nice boost to our client’s non-IRA investment accounts!

From The Onion satire site:

MARKET CYCLE – WEALTH MONEY MANAGEMENT – TREND FOLLOWING – GLOBAL MACRO – HEDGE FUND

Thanks for reading… Steph Aust

Article by Marketcycle Wealth Management