Portfolio Manager Chuck Royce and Co-CIO Francis Gannon recap 3Q19, discuss September’s reversals, and detail why these market rotations could be sustainable.

Q3 2019 hedge fund letters, conferences and more

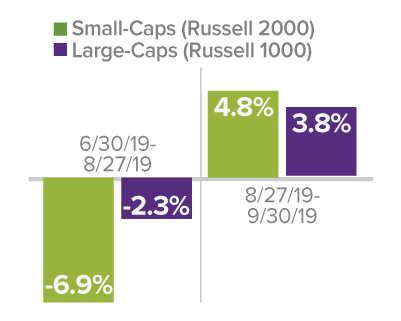

What do you make of the rebound for cyclicals and small-cap value late in 3Q19?

Chuck Royce It was certainly a welcome development, one that we hope is sustainable going forward. The cyclical areas of small-cap in particular have looked very reasonably priced to us for a while. We’d been waiting for some time for a lot of these stocks to turn around and gain recognition for what we saw as very attractive fundamental attributes.

There were a few other elements to the move that made it really interesting to us. First, small-caps, micro-caps, value, and cyclical stocks all made strong upward moves. In light of what we’ve seen over the last few years, we didn’t expect to see this sort of favorable reversal for value and cyclicals during an upward move—though we’re very pleased that we did. The second element that made it remarkable was that these shifts occurred within a couple of days of each other.

If you’re looking for more timely hedge fund insight, ValueWalk’s exclusive newsletter Hidden Value Stocks offers exclusive access to under-the-radar value hedge funds and their ideas. Click here to find out more and signup for a free no-obligation trial today.

Three Reversals Within 3Q19

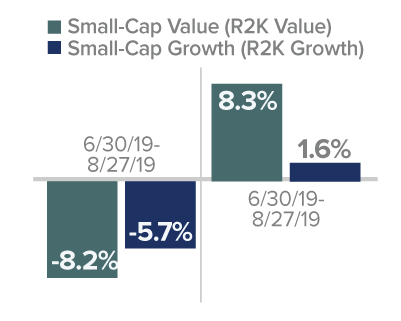

Maybe the most notable aspect, however, was small-cap value’s strength on the upside in September. After trailing its growth sibling from 6/30/19-8/27/19 (-8.2% vs. -5.7%), the Russell 2000 Value Index advanced 8.3% from 8/27/19-9/30/19 compared to 1.6% gain for the Russell 2000 Growth Index. Even allowing for the need to make up ground from the downside, that’s an impressive relative advantage, especially over a short period of time for a style that has typically lagged when the markets have recovered over the last couple of years.

Do you think the September rebound is sustainable?

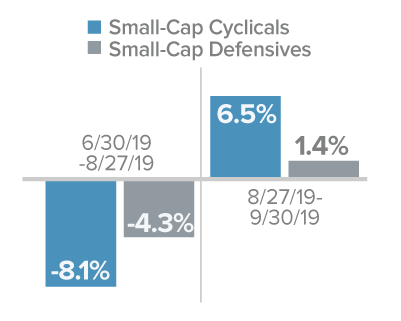

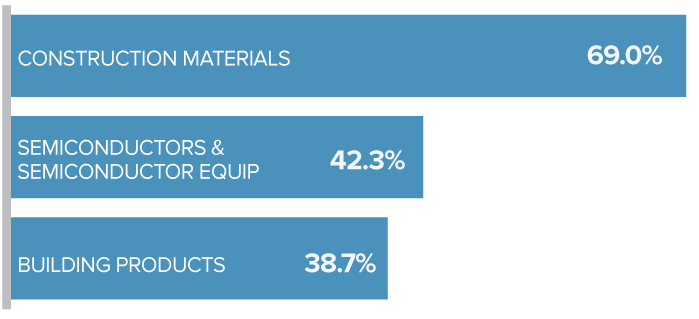

CR One important development that caught our attention was the relative strength of three bellwether industries within the Russell 2000 that are also economically sensitive, cyclical areas so far this year—construction materials, semiconductors & semiconductor equipment, and building products. While the first and the last of these industries are housing-related and as such could be expected to rally when interest rates fall, we think that the strength of these industries may also be related to the absence of bad news about important parts of the U.S. economy. Investors may be beginning to see that slower growth—which we have in certain areas—is very different from a broad-based recession, which still looks remote to us.

Bellwether Industries

Select R2K Industries YTD through 9/30/19

Were there any other notable developments?

Francis Gannon There were some related developments that went along with those that Chuck mentioned. For example, stocks with higher earnings yields and free cash flow did very well, and dividend payers outperformed non-dividend payers. Additionally, low momentum stocks outperformed high momentum issues in the third quarter. Finally, there was an interesting dichotomy in defensive sectors. The bond-like defensive sectors—Utilities, Real Estate, and Consumer Staples—had positive returns in the quarter, as they often do when interest rates fall. However, Health Care and Communication Services—also ostensibly defensive sectors—were anything but as they underperformed in the quarter.

What is your take on why small-caps have lagged large caps for an extended period?

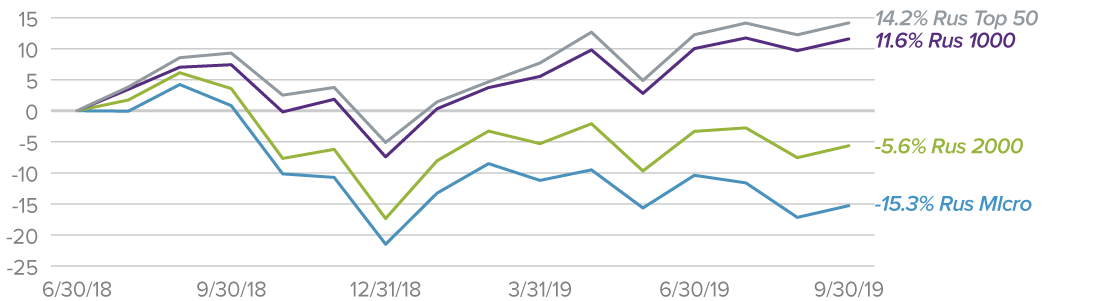

CR I have a few observations that I think a lot of investors may not be aware of. First, if you look at the underperformance for small-caps over the past 10 years, most of the disadvantage has occurred over the past 15 months. From 9/30/2009 to 6/30/2018, the Russell 2000 gained 13.6% on an annualized basis versus 13.8% for the Russell 1000 Index—nearly equal returns over an extended time period. From 6/30/18-9/30/19, however, small-caps really struggled—they were down 5.6% on a cumulative basis versus an increase of 11.6% for large-caps. And mega-cap stocks, as represented by the Russell Top 50, did even better, advancing 14.2% cumulatively over the same period. On the opposite end of the capitalization spectrum, micro-caps fell 15.3% over this same period. The 15-month return spread between mega-caps and micro-caps has been nearly 30%. I don’t have a good explanation as to why that is, but I would say we are in the midst of an extraordinary preference for mega-caps that seems unlikely to last.

Notable Index Performance Spreads

Russell Index Performance—6/30/18-9/30/19

What do you think all of this implies for small-cap stocks?

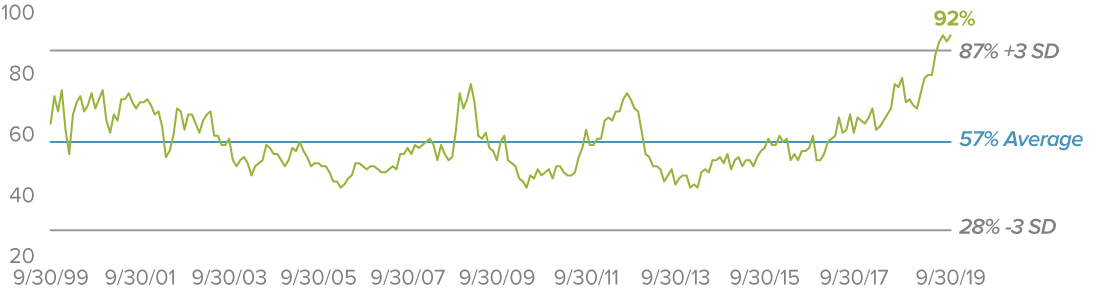

FG Mega-cap stocks currently dominate the market. To get a sense of their strength and size, the two biggest in the U.S.—Microsoft and Apple—had a combined market cap of more than $2.1 trillion at the end of September. The entire Russell 2000 Index, on the other hand, had a combined market cap of $2.2 trillion.

Historically, the two biggest names in the U.S. market averaged roughly 57% of the total market cap of small-cap stocks. At the end of September, however, they were equal to 92% of small-cap’s total market cap—more than three standard deviations greater than their long-term historical average. What would happen if this strong preference for mega-caps unwound, even modestly? From our perspective as small-cap specialists, it strikes us as a great redistribution opportunity for the small-cap asset class. Any profit taking among, say, the largest 50 companies equates to a quite sizable potential investment in small-cap stocks. And that would be the case even if these mega-caps stocks were to stay relatively flat.

Mega-Cap Market Cap Dominance

Largest Two U.S. Companies as Percentage of Russell 2000’s Total Market Cap from 8/31/99 through 9/30/19

Were you pleased with the recent earnings and guidance from your holdings?

FG Absolutely. Earnings were solid and generally in line with expectations for the majority of our holdings. There were exceptions on both sides, of course. Certain companies did better than expected, and, to be fair, expectations in many cases had been set lower as the economy continues to grow at a slower pace. A handful of others disappointed, mostly because they had significant exposure to China.

But this is the important point—it felt like a pretty ordinary earnings season. The mix of the expected and unexpected that we saw in 3Q19 is fairly typical because earnings season always carries its share of surprises as well as more likely developments. What was notable to us was the disconnect between August’s headlines, which were dominated by uncertainty about ongoing economic prospects—and companies reporting mostly positive results while also not lowering guidance for the rest of the year. That’s a very positive signal to us.

Are you concerned that the Russell 2000 remained 11.1% off its all-time high from August 2018?

CR I wouldn’t say we’re concerned as much as we were impatient for a turnaround prior to September. Of course we are guardedly optimistic that the rebound will last. But it’s certainly been a difficult twelve months for small-cap stocks relative to their larger siblings, which tends to be forgotten in light of how strong the first quarter was for equities as a whole this year.

FG The challenges for small-caps over the one-year period were particularly tough relative to large-caps. Our own research shows how rare it’s been for large-caps to be positive while small-caps are negative over 12-month periods. It’s happened only 8% of the time over the last 20 years—that’s only 16 out of the last 229 periods from 9/30/99 through 9/30/19. Moreover, there have been 14 periods where we have data following the 12-month periods after this kind of large-cap/small-cap divergence. In 13 of the 14—more than 90% of the time—small-caps outpaced large-caps, and the average return differential was more than 300 basis points. We think that makes a powerful case for small-cap.

Rare Divergence Historically Followed by Frequent Small-Cap Rebound

Trailing 1-Yr Periods from 9/30/99 through 9/30/19

What have you been hearing from company management teams?

CR In light of all the headlines warning us about recession signals and constant talk about tariffs and trade, almost all of our companies are constructive. Most have been preparing as well as they can for the negative impacts of tariffs for more than a year at this point, so while tariffs and trade present genuine challenges, they’re not new ones. In fact, the biggest challenge common to many of the companies we hold, particularly those in more specialized technical fields, is finding people. The labor market is awfully tight, and companies are looking longer and harder for qualified workers. That’s not the kind of problem we see when the economy is in poor shape.

FG I think what’s also interesting is what management teams are not saying. Some companies we hold have experienced slowdowns while others are facing challenges because of exposure to China. Yet almost no one we’ve talked to is worried about a recession. It’s simply doesn’t come up until we ask. And when we do ask, we’re hearing that it’s not a major near-term concern. As Chuck said, we’re hearing a lot more about the efforts to hire and retain talented people.

What is your take on the prospects for small-cap cyclicals?

FG When we analyze economically sensitive companies, we often gravitate to those that are innovators and/or beneficiaries of innovation—and we feel very confident about their prospects. These companies are in the business of boosting the productivity of their customers and helping them execute more efficiently. They can be found not just in the technology space, but also in several different industrial areas—they’re most prevalent in machinery—and even in chemical companies. The uses may sound pedestrian, but the benefits to the business are anything but. And with ample pressure on companies to innovate and execute more effectively, we see solid demand for companies that offer productivity-boosting products and services regardless of the near-term pace of economic growth.

Can you discuss a name in your high-quality strategy that’s has done well so far this year?

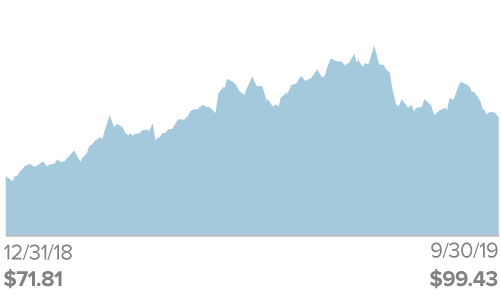

CR One of the first names that comes to mind is John Bean Technologies (JBT). This is a company that is definitely an innovator, but it does so in an area that most people probably wouldn’t associate with innovation by providing technology in food processing machinery and airport equipment. While that may not scream ‘cutting edge,’ the company is a forward-thinking market leader in specialized products and services for food storage and transport. John Bean has also been building its presence in Asia, where a growing middle class is eager for travel.

John Bean Technologies (JBT)

YTD as of 9/30/19

In May, the firm announced strong quarterly results while also raising its full-year 2019 guidance. Its shares have since corrected a bit, mostly due to a narrow earnings miss in the second quarter, but it’s still been a strong performer so far in 2019. Its long-term prospects also continue to look very promising to us. We’re happy to be in for the long run.

Can you discuss another in the same strategy that hasn’t yet taken off?

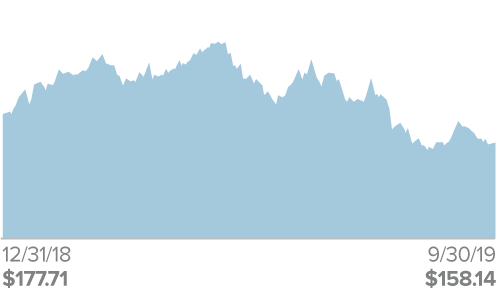

CR Quaker Chemical (KWR), which does business as Quaker Houghton, develops and produces a range of formulated chemical products for various heavy industrial and manufacturing uses. Although it’s relatively new to our quality strategy, our experience with it goes back four decades. Its shares have been down so far in 2019, partly the result of lower sales volumes, caused by slower automotive and other industrial production outside the U.S., and steel production declines in June by a number of global customers in order to correct inventory issues. Throughout this period, Quaker maintained solid margins and expanded market share, two highly positive signs in our view.

Quaker Chemical (KWR)

YTD as of 9/30/19

Quaker closed out a major combination with Houghton International in July—which gave it a larger foothold in metalworking fluids—and announced in August that it was buying the operating divisions of Norman Hay plc, a private U.K. company in a similar business. These moves are part of Quaker’s ongoing efforts to boost shareholder value through acquisitions that effectively complement its existing business.

The firm announced later in August that it doesn’t expect any dramatic changes in sales volumes over the next quarter. Management did say, however, that year-over-year comparisons should improve because its markets weakened appreciably in the second half of 2018. As a result, Quaker doesn’t anticipate the same level of negative impacts that it faced in the first half of 2019 through the rest of this year and into early 2020.

What is your outlook for small-cap performance?

CR As the pace of growth continues to slacken, multiple expansion will be harder to come by, so I’m not expecting high returns. But I do think that small-caps will outperform large-caps. The valuation discrepancies are just too wide right now, especially based on our preferred valuation metric, EV/EBIT (enterprise value divided by earnings before interest & taxes). The median EV/EBIT for the Russell 2000 was 17.74 at the end of September and 19.26 for the Russell 1000, excluding non-earners. What makes this even more compelling to us is that historically small-caps have traded at a modest premium to large-caps on average. So we’re feeling confident in the prospects for our asset class within the context of what we suspect will be a moderate return environment for equities.

“We’re feeling confident in the prospects for our asset class within the context of what we suspect will be a moderate return environment for equities.” — Chuck Royce

Over the last four quarters, small-caps went straight down (4Q18) and then straight up (1Q19), before they basically ran in place over the last six months. Of course, stocks don’t move sideways indefinitely—they either break down or break out at some point. When we’re thinking about the subsequent direction for stocks, we ask two key questions: Can small-cap earnings growth improve from here? If the answer is ‘yes,’ then we see a breakout; if the answer is ‘no,’ a breakdown. What might drive small-cap earnings growth? Three currently weak areas may be bottoming soon: year over year small-cap EPS growth, the ISM Manufacturing Index, and Western European and Chinese economies—and China actually enjoyed a better September than most observers were expecting, which should help Germany and other European economies.

So while we continue to get mixed signals from the U.S. economy, we also see attractive valuations and enough fundamental strength among our small-cap holdings to suggest the possibility of a sustainable shift to small-cap leadership driven by cyclical stocks.

Article by Royce Funds